As a new academic year begins, students and recent graduates are likely to be concerned about the latest developments in student loan rates. In September 2025, the interest rates on federal student loans have undergone significant changes, affecting both new and existing borrowers. For instance, undergraduate students can expect to pay an interest rate of around 5.5% on their loans, which can add up over time.

The impact of these rate changes will be felt by borrowers in various ways, including increased monthly payments and a longer repayment period. To put this into perspective, a student with a $30,000 loan at 5.5% interest will pay around $300 per month over 10 years, compared to $280 per month at 4.5% interest. This highlights the importance of understanding the latest student loan rates and their implications.

Here are some key points to consider when it comes to the latest student loan rates:

- Interest rates on federal student loans are determined by the government and can change annually

- Borrowers can choose from various repayment plans, including income-driven plans that can help lower monthly payments

- Consolidating loans or refinancing with a private lender may be an option for some borrowers to reduce their interest rates

It is essential for borrowers to review their loan terms and explore available options to manage their debt effectively. By staying informed about the latest student loan rates and developments, borrowers can make informed decisions about their financial situation and plan for a more stable financial future.

Understanding the New Rates

As a borrower, it's essential to stay up-to-date with the current federal student loan interest rates. The rates for the 2022-2023 academic year have been set, and they have increased compared to the previous year. This change can significantly impact your monthly payments, so it's crucial to understand how these rates work.

The federal student loan interest rates are divided into two main categories: subsidized and unsubsidized loans. Subsidized loans are available to undergraduate students who demonstrate financial need, and the government pays the interest on these loans while the student is in school. Unsubsidized loans, on the other hand, are available to both undergraduate and graduate students, and the borrower is responsible for paying the interest on these loans.

Here are the current interest rates for federal student loans:

- Subsidized loans: 4.99% for undergraduate students

- Unsubsidized loans: 4.99% for undergraduate students and 6.54% for graduate students

These rates are subject to change, and it's essential to check the official government website for the most up-to-date information.

The difference between subsidized and unsubsidized loans can significantly impact your monthly payments. For example, if you borrow $10,000 in subsidized loans at 4.99% interest, your monthly payment could be around $50. However, if you borrow $10,000 in unsubsidized loans at 6.54% interest, your monthly payment could be around $70. This difference can add up over time, so it's crucial to consider the type of loan and interest rate when borrowing.

To give you a better idea of how these rate changes can affect your monthly payments, let's consider an example. Suppose you have a $30,000 loan at 4.99% interest, and your monthly payment is $150. If the interest rate increases to 6.54%, your monthly payment could increase to $200. This is a significant difference, and it's essential to factor in these changes when creating your budget and repayment plan.

By understanding the current federal student loan interest rates and how they have changed, you can make informed decisions about your borrowing and repayment strategy. It's essential to review your loan options carefully and consider factors like interest rates, repayment terms, and loan forgiveness programs to ensure you're making the best choice for your financial situation.

.png?1589760253409)

Managing Your Student Loan Debt

When it comes to managing student loan debt, it's essential to understand your repayment options. Income-driven repayment plans are a great way to make your monthly payments more affordable, as they're based on your income and family size. For example, the Income-Based Repayment (IBR) plan can help lower your monthly payments to 10% or 15% of your discretionary income.

To get started with an income-driven repayment plan, you'll need to contact your loan servicer and provide financial information, such as your income and family size. You can also use the Federal Student Aid website to estimate your monthly payments under different plans. This can help you choose the plan that works best for you and your budget.

Refinancing student loans with private lenders can be another option for managing debt, but it's crucial to weigh the benefits and drawbacks. The benefits of refinancing include potentially lower interest rates and lower monthly payments. However, refinancing with a private lender may require you to give up federal benefits, such as income-driven repayment plans and loan forgiveness programs.

Some things to consider when deciding whether to refinance with a private lender include:

- Interest rates: Will you qualify for a lower interest rate with a private lender?

- Fees: Are there any origination fees or other charges associated with refinancing?

- Repayment terms: Will you have more flexible repayment terms with a private lender?

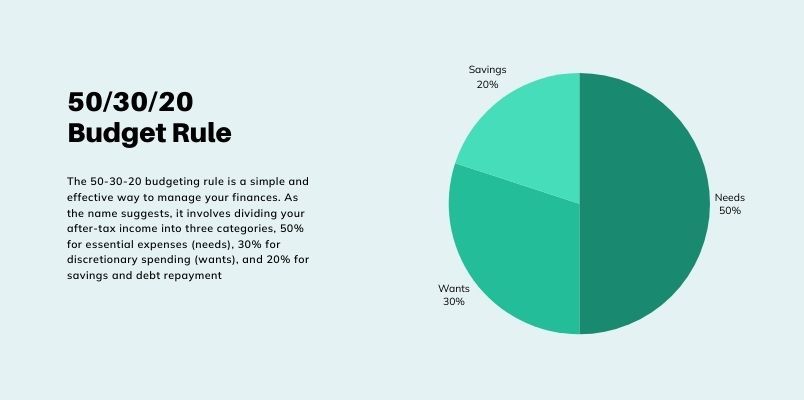

Creating a budget that accounts for student loan payments is also vital for managing debt. Start by tracking your income and expenses to see where your money is going. You can then use the 50/30/20 rule as a guideline to allocate your income towards necessities, discretionary spending, and saving and debt repayment.

When creating your budget, be sure to prioritize your student loan payments and make them a fixed expense. You can also consider setting up automatic payments to ensure you never miss a payment. Additionally, consider using a budgeting app or spreadsheet to track your expenses and stay on top of your finances. By following these tips, you can take control of your student loan debt and make progress towards becoming debt-free.

Impact on Financial Health

Having a significant amount of student loan debt can have a lasting impact on your financial health. It can affect your credit scores, making it harder to get approved for other loans or credit cards in the future. For instance, missing a payment or defaulting on a loan can lower your credit score by as much as 100 points.

Making timely payments is crucial to maintaining a good credit score and overall financial health. By paying your loans on time, you demonstrate to lenders that you are responsible and capable of managing your debt. This can also help you avoid late fees and interest charges that can add up over time.

To avoid default, it's essential to stay on top of your payments and communicate with your lender if you're having trouble making payments. You can also consider income-driven repayment plans or loan forgiveness programs that can help make your payments more manageable.

Some ways to pay off your loans faster include:

- Starting a side hustle, such as freelancing or tutoring, to increase your income

- Taking on a part-time job to supplement your income

- Selling items you no longer need or use to put the proceeds towards your loans

By exploring these options, you can pay off your loans faster and improve your financial health.

Paying off your student loans can seem daunting, but with a solid plan and commitment, you can achieve financial freedom. By making timely payments, avoiding default, and exploring ways to increase your income, you can take control of your financial health and build a brighter future. It's also important to monitor your credit report regularly to ensure it's accurate and up-to-date, as this can help you identify any potential issues early on.

Future Outlook and Planning

As a borrower, it's essential to stay informed about potential future changes to student loan rates. Speculation suggests that rates may rise in the coming years, which could increase monthly payments for variable-rate loans. For instance, a 1% rate hike on a $30,000 loan could add $10 to $20 to monthly payments.

To plan for potential rate hikes, borrowers should review their loan terms and consider consolidating or refinancing their debt. This can help simplify payments and potentially secure a lower fixed interest rate. Borrowers can also take advantage of income-driven repayment plans, which can cap monthly payments at a percentage of their income.

When it comes to planning for the future, borrowers should prioritize investing and saving alongside their debt repayment. Investing in a retirement account, such as a 401(k) or IRA, can provide long-term benefits and help borrowers achieve financial stability. Some key investing strategies for borrowers include:

- Starting small, with automatic transfers to a savings or investment account

- Taking advantage of employer-matched retirement accounts

- Diversifying investments to minimize risk and maximize returns

In addition to investing, borrowers should focus on building an emergency fund to cover 3-6 months of living expenses. This can provide a safety net in case of unexpected expenses or financial setbacks. By prioritizing saving and investing, borrowers can make progress towards long-term financial goals, such as buying a home or starting a business, despite their student loan debt.

Borrowers can also use tax-advantaged accounts, such as a Roth IRA, to save for specific goals, like retirement or a down payment on a home. By automating savings and investments, borrowers can make steady progress towards their goals and reduce the impact of potential rate hikes or changes in loan terms. By staying informed and proactive, borrowers can navigate the complexities of student loan debt and achieve long-term financial success.

Frequently Asked Questions (FAQ)

How do I check my current student loan interest rate?

Checking your current student loan interest rate is a crucial step in managing your debt. By knowing your interest rate, you can make informed decisions about your repayment strategy and potentially save money on interest payments. To get started, you can log into your loan servicer's website, where you'll typically find a dashboard with details about your loan, including the current interest rate.

If you're not sure how to access your loan information online, you can contact your loan servicer directly for assistance. They can provide you with the information you need and guide you through the process of checking your interest rate. You can usually find the contact information for your loan servicer on their website or on your loan documents.

Here are some steps you can take to check your current interest rate:

- Log into your loan servicer's website using your username and password

- Look for a section on your dashboard that displays your loan details, such as the interest rate and balance

- Contact your loan servicer's customer service department if you have any questions or need help accessing your information

It's a good idea to check your interest rate regularly, as it may change over time due to market fluctuations or other factors. By staying on top of your interest rate, you can stay in control of your debt and make progress towards becoming debt-free. For example, if you notice that your interest rate has increased, you may want to consider consolidating your loans or refinancing to a lower rate.

Can I refinance my student loans to a lower interest rate?

Refinancing your student loans can be a great way to save money on interest and simplify your payments. By working with a private lender, you may be able to secure a lower interest rate, which can help you pay off your debt faster. However, it's essential to understand the potential trade-offs involved in refinancing.

When you refinance your student loans, you're essentially taking out a new loan with a private lender to pay off your existing loans. This can be a good option if you have a good credit score and can qualify for a lower interest rate. For example, if you have a federal loan with an interest rate of 6% and you can refinance it to a private loan with an interest rate of 4%, you could save a significant amount of money on interest over the life of the loan.

Here are some things to consider when deciding whether to refinance your student loans:

- Loss of federal loan benefits, such as income-driven repayment plans and loan forgiveness programs

- Potential loss of protections, such as deferment and forbearance options

- Interest rates and fees associated with the new loan

It's crucial to weigh these factors carefully and consider your individual circumstances before making a decision.

If you do decide to refinance your student loans, be sure to shop around and compare rates from multiple lenders to find the best deal. You can also use online tools and calculators to determine how much you could save by refinancing and whether it's the right choice for you. By doing your research and understanding the pros and cons, you can make an informed decision that helps you manage your debt and achieve your financial goals.

How can I pay off my student loans faster?

Paying off student loans can be a daunting task, but there are several strategies that can help borrowers tackle their debt more efficiently. One approach is to make extra payments, which can be as simple as paying a little more each month or making a lump sum payment when possible. For example, paying an extra $50 per month on a $30,000 loan can save around $1,000 in interest over the life of the loan.

Another popular method is the snowball approach, where borrowers focus on paying off their smallest loan balances first while making minimum payments on larger loans. This strategy can provide a sense of accomplishment and motivation as smaller loans are paid off quickly. It's essential to note that this method may not always be the most cost-effective, as it doesn't necessarily prioritize loans with the highest interest rates.

To increase their income and put more money towards their loans, borrowers can explore side hustles, such as freelancing, tutoring, or part-time jobs. Some popular side hustles include:

- Selling products online through platforms like eBay or Amazon

- Ride-sharing or food delivery services

- Participating in online surveys or focus groups

These side hustles can provide a significant boost to one's income, allowing borrowers to make extra payments and pay off their loans faster.

By combining these strategies, borrowers can create a personalized plan to tackle their student loans and become debt-free sooner. It's crucial to review and adjust this plan regularly to ensure it remains effective and aligned with one's financial goals. With discipline, patience, and the right approach, paying off student loans can become a manageable and achievable task.