As a young adult, managing debt can be overwhelming, especially when it comes to student loans. Understanding student loan interest rates is a critical step in taking control of your financial future. By grasping the basics of interest rates, you can make informed decisions about your loans and develop a plan to pay them off efficiently.

When it comes to student loans, interest rates can significantly impact the total amount you owe over time. For instance, a loan with a 6% interest rate will accrue more interest than one with a 4% rate, resulting in a larger total payoff amount. This is why it's essential to consider interest rates when choosing a loan or repayment plan.

To get started, it's helpful to understand the different types of interest rates, including:

- Fixed interest rates, which remain the same over the life of the loan

- Variable interest rates, which can change over time

- Subsidized interest rates, which are partially paid by the government

By familiarizing yourself with these concepts, you can begin to build a solid foundation for managing your student loan debt and securing a brighter financial future.

In the following sections, we'll dive deeper into the world of student loan interest rates, exploring topics such as how to calculate interest, strategies for reducing interest rates, and tips for choosing the best repayment plan for your needs. Whether you're a current student or a recent graduate, this guide will provide you with the knowledge and tools necessary to navigate the complex landscape of student loan interest rates and make informed decisions about your financial future.

Understanding Federal Student Loan Interest Rates

For the 2025 academic year, federal student loan interest rates have been set to help students and families plan for the cost of higher education. Undergraduate students can expect to pay an interest rate of 4.53% on their Direct Subsidized and Unsubsidized Loans, while graduate students will pay 6.54% on their Unsubsidized Loans. These rates apply to loans disbursed between July 1, 2024, and June 30, 2025.

The interest rates on federal student loans are determined by Congress and are typically based on the 10-year Treasury note rate, with an added margin to account for administrative costs and other factors. This means that federal student loan interest rates can fluctuate from year to year, depending on market conditions. For example, if the 10-year Treasury note rate increases, federal student loan interest rates may also rise.

Here are the current federal student loan interest rates for comparison:

- Undergraduate Direct Subsidized and Unsubsidized Loans: 4.53%

- Graduate Direct Unsubsidized Loans: 6.54%

- Direct PLUS Loans: 7.54%

It's worth noting that these rates are relatively low compared to previous years, making it a good time for students to borrow if necessary. To put this into perspective, the interest rate on undergraduate loans was 5.05% in 2020, and 4.53% in 2022, so rates have been trending downward in recent years.

To understand the impact of federal student loan interest rates on your own borrowing, consider the total amount you plan to borrow and the repayment term. For instance, a lower interest rate can save you hundreds or even thousands of dollars in interest over the life of the loan. By staying informed about federal student loan interest rates and trends, you can make more informed decisions about your own student loan borrowing and repayment strategy.

.png?1589760253409)

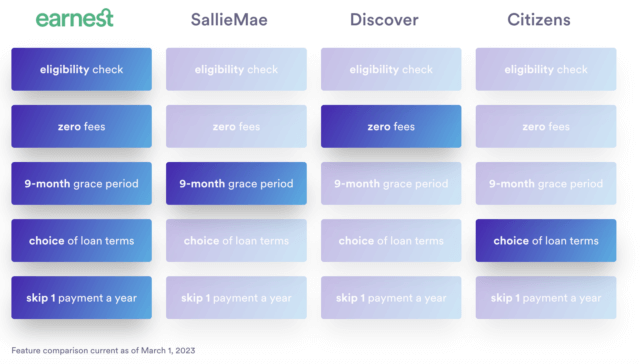

Exploring Private Student Loan Options and Rates

When it comes to financing your education, you have two primary options: federal and private student loans. Federal student loans are provided by the government, while private student loans are offered by banks, credit unions, and other lenders. Generally, federal loans have more favorable terms and lower interest rates, but they may not cover the full cost of your education.

To be eligible for federal student loans, you typically need to be a US citizen, enrolled in a degree-granting program, and making satisfactory academic progress. Private student loans, on the other hand, often require a credit check and may necessitate a cosigner. Interest rates for private loans can vary significantly depending on the lender and your creditworthiness, ranging from around 4% to over 12% APR.

Some key factors to consider when comparing private student loan interest rates include:

- Interest rate type: fixed or variable

- Cosigner requirements: do you need a creditworthy cosigner to qualify

- Loan terms: what are the repayment periods and conditions

- Fees: are there any origination or late payment fees

For example, you may find a lender offering a competitive interest rate, but with a shorter repayment term or higher fees.

Private student loans can be a good option if you've exhausted your federal loan eligibility or need additional funding. However, they often lack the flexible repayment options and forgiveness programs available with federal loans. It's essential to weigh the potential risks and benefits, considering factors like the total cost of the loan and your ability to repay it after graduation.

To get the best deal on a private student loan, it's crucial to shop around and compare rates from multiple lenders. You can use online tools and resources to research and compare loan options, or consult with a financial aid advisor for personalized guidance. By doing your research and carefully evaluating your options, you can make an informed decision that works best for your financial situation and educational goals.

Strategies for Managing Student Loan Debt

When it comes to managing student loan debt, there are several strategies that can help make repayment more manageable. One option to consider is debt consolidation, which involves combining multiple loans into a single loan with a lower interest rate and a single monthly payment. This can simplify the repayment process and potentially save money on interest over time.

Debt refinancing is another strategy that can help with high-interest student loans, involving replacing an existing loan with a new loan that has a lower interest rate and better repayment terms. However, it's essential to weigh the pros and cons of each option, as refinancing may require a good credit score and a stable income. For example, refinancing a federal loan may result in losing certain borrower benefits, such as income-driven repayment plans.

Income-driven repayment plans can be a lifeline for federal student loan borrowers, as they can help lower monthly payments based on income and family size. These plans include options like Income-Based Repayment (IBR) and Pay As You Earn (PAYE), which can cap monthly payments at a certain percentage of discretionary income. To take advantage of these plans, borrowers should review the eligibility requirements and application process.

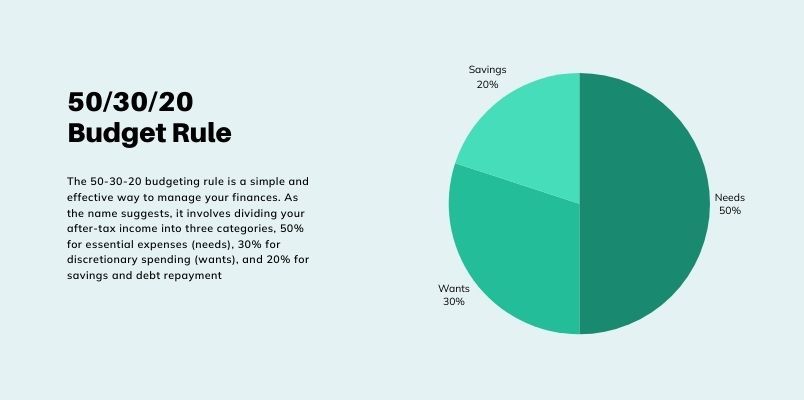

To create a budget that prioritizes student loan repayment, it's crucial to track income and expenses and allocate a sufficient amount for loan payments. Some tips for creating a budget include:

- using the 50/30/20 rule to allocate 50% of income towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment

- utilizing budgeting apps like Mint or You Need a Budget (YNAB) to track expenses and stay on top of finances

- exploring side hustles, such as freelancing or part-time jobs, to increase income and put more towards loan payments

By prioritizing student loan repayment and exploring strategies like debt consolidation, refinancing, and income-driven repayment plans, borrowers can take control of their debt and work towards a more stable financial future. Additionally, creating a budget and using budgeting apps can help borrowers stay organized and motivated, making it easier to stick to a repayment plan and achieve financial freedom. With the right approach and tools, managing student loan debt can become a manageable and achievable goal.

Impact of Interest Rates on Financial Health

High-interest student loans can have a significant impact on your long-term financial goals, such as buying a home or retirement savings. For instance, a student loan with an interest rate of 6% can add thousands of dollars to the total amount you owe over the life of the loan. This can make it challenging to save for other financial goals, like a down payment on a house or contributing to a retirement account.

Credit scores play a crucial role in determining interest rates for private student loans and other financial products. A good credit score can help you qualify for lower interest rates, which can save you money in the long run. For example, a credit score of 750 or higher may qualify you for an interest rate of 4% on a private student loan, while a credit score of 600 or lower may result in an interest rate of 8% or higher.

To prioritize financial health while paying off student loans, it's essential to build an emergency fund and start investing. This can help you avoid going further into debt when unexpected expenses arise and make progress towards your long-term financial goals. Here are some tips to get you started:

- Allocate 10% to 20% of your income towards saving and investing

- Take advantage of tax-advantaged retirement accounts, such as a Roth IRA or 401(k)

- Consider using the 50/30/20 rule to allocate your income towards necessities, discretionary spending, and saving and debt repayment

Paying off high-interest student loans requires a solid plan and discipline, but it's not impossible. By prioritizing your financial health and making smart financial decisions, you can overcome the challenges of high-interest debt and achieve your long-term financial goals. For example, you can consider consolidating your student loans or refinancing them to a lower interest rate, which can help you save money and pay off your debt faster.

In addition to paying off student loans, it's also important to monitor your credit report and score regularly to ensure there are no errors or negative marks that can affect your creditworthiness. You can request a free credit report from each of the three major credit reporting agencies (Experian, TransUnion, and Equifax) once a year and dispute any errors you find. By taking control of your credit and debt, you can improve your financial health and achieve your long-term goals, such as buying a home, retiring comfortably, or starting your own business.

Conclusion and Next Steps

As we wrap up our discussion on student loan interest rates for 2025, it's essential to summarize the key takeaways. Student loan interest rates can significantly impact financial planning, and understanding the current rates is crucial for making informed decisions. For instance, a 1% difference in interest rate can save hundreds of dollars over the life of the loan.

To further manage student loan debt, it's a good idea to explore additional resources, such as financial counseling services. These services can provide personalized advice and help create a tailored plan to tackle debt. Some examples of resources include the National Foundation for Credit Counseling and the Financial Counseling Association of America.

For those looking to take control of their student loans, consider the following steps:

- Review your current loan terms and interest rates to identify areas for optimization

- Research income-driven repayment plans and forgiveness options

- Explore refinancing or consolidation options to potentially lower interest rates

By taking these steps, readers can make informed decisions about their student loans and create a plan to achieve financial stability.

Ultimately, managing student loan debt requires a proactive approach, and there are many resources available to help. By reviewing their own student loans and considering options for optimization, readers can save money and reduce financial stress. Start by reviewing your loan statements and exploring online resources, such as the Department of Education's website, to learn more about your options.

Frequently Asked Questions (FAQ)

How do federal student loan interest rates compare to private loan rates?

When it comes to financing your education, understanding the difference between federal and private student loan interest rates is crucial. Federal student loan interest rates are generally fixed, which means they remain the same throughout the life of the loan. This can provide borrowers with a sense of stability and predictability when it comes to their monthly payments.

In contrast, private loan rates can be variable, which means they can fluctuate over time based on market conditions. Additionally, private loan rates often depend on your credit score, so borrowers with lower credit scores may be charged higher interest rates. For example, a borrower with a good credit score may qualify for a private loan with an interest rate of 6%, while a borrower with a poor credit score may be offered a rate of 12%.

Here are some key factors to consider when comparing federal and private student loan interest rates:

- Federal loan rates are often lower, with rates ranging from 4.53% to 7.54% for the 2022-2023 academic year

- Private loan rates can range from 3.5% to 14.5% or more, depending on the lender and your credit score

- Variable interest rates on private loans can increase over time, making your monthly payments more expensive

To make an informed decision, it's essential to shop around and compare rates from different lenders. You can also consider working to improve your credit score before applying for a private loan, as this can help you qualify for a lower interest rate. By understanding the differences between federal and private student loan interest rates, you can make a more informed decision about how to finance your education and minimize your debt burden.

Can I refinance my federal student loans to a lower interest rate?

Refinancing federal student loans to private loans can be a viable option for those looking to reduce their interest rates. This process involves replacing your existing federal loans with a new private loan, which may offer a lower interest rate and potentially lower monthly payments. For instance, if you have a federal loan with an interest rate of 6% and you refinance it to a private loan with an interest rate of 4%, you could save a significant amount of money over the life of the loan.

To refinance your federal student loans, you will typically need to have a good credit score, as lenders use this to determine the risk of lending to you. A good credit score can help you qualify for a lower interest rate, which can save you money in the long run. For example, a credit score of 750 or higher may qualify you for the best interest rates, while a score below 700 may result in a higher interest rate.

When considering refinancing your federal student loans, it's essential to weigh the pros and cons. Here are some key points to consider:

- Lower interest rates: Refinancing to a private loan may offer a lower interest rate, which can save you money over time.

- Loss of federal benefits: Refinancing federal loans to private loans means giving up federal benefits like income-driven repayment and forgiveness programs.

- Credit score requirements: You will typically need a good credit score to qualify for a private loan with a lower interest rate.

Before making a decision, it's crucial to evaluate your individual circumstances and consider whether refinancing is right for you. If you have a stable income and a good credit score, refinancing your federal student loans to a private loan may be a good option. However, if you're unsure about your financial situation or rely on federal benefits like income-driven repayment, it may be best to stick with your existing federal loans.

How can I pay off my student loans quickly and save on interest?

Paying off student loans can be a daunting task, but with the right strategy, you can save on interest and become debt-free sooner. One effective way to do this is by paying more than the minimum payment each month. For example, if your minimum payment is $100, consider paying $150 or $200 to make a bigger dent in your loan balance.

Using tax deductions for student loan interest is another way to reduce your overall debt burden. The government offers tax deductions for student loan interest, which can help lower your taxable income and put more money in your pocket. You can deduct up to $2,500 of student loan interest paid each year, which can result in significant savings.

Here are some additional tips to help you pay off your student loans quickly and save on interest:

- Consider consolidating or refinancing your loans to lower your interest rate or monthly payment

- Take advantage of income-driven repayment plans, which can lower your monthly payment based on your income and family size

- Use the snowball method, where you pay off loans with the smallest balances first to build momentum and confidence

Consolidating or refinancing your student loans can be a great way to simplify your payments and save on interest. By combining multiple loans into one, you can lower your monthly payment and reduce the amount of interest you pay over time. For instance, if you have multiple loans with high interest rates, you may be able to refinance them into a single loan with a lower interest rate, resulting in significant savings over the life of the loan.

By following these tips and staying committed to your debt repayment plan, you can pay off your student loans quickly and save on interest. Remember to review your budget regularly and make adjustments as needed to ensure you're on track to becoming debt-free. With patience, discipline, and the right strategy, you can overcome your student loan debt and achieve financial freedom.