As a student with poor credit, finding the right loan options for your education can be a daunting task. Many lenders tend to favor borrowers with good credit, leaving those with poor credit feeling left behind. However, there are still several options available for students who need financial assistance to pursue their academic goals.

Paying for education can be expensive, and loans are often a necessary evil for many students. For those with poor credit, it's essential to explore all available options and understand the terms and conditions of each loan. By doing so, students can make informed decisions about their financial aid and avoid further damaging their credit score.

Some loan options for students with poor credit include:

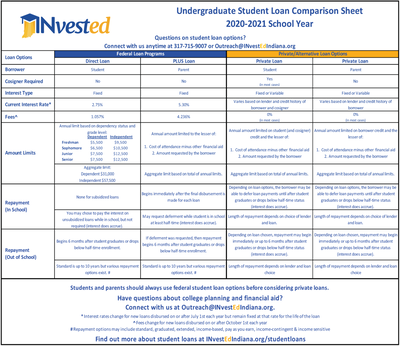

- Federal student loans, which do not require a credit check

- Private student loans with a co-signer, which can help reduce interest rates

- Income-driven repayment plans, which can make monthly payments more manageable

These options can provide students with the financial support they need to complete their education and improve their future career prospects.

When searching for loan options, it's crucial to consider factors such as interest rates, repayment terms, and fees. Students should also be cautious of lenders that charge exorbitant interest rates or have inflexible repayment plans. By being aware of these factors, students can make smart financial decisions and avoid traps that can lead to further debt.

In this article, we will delve into the world of student loans and explore the best options for students with poor credit. We will provide practical tips and examples to help students navigate the complex process of finding and securing a suitable loan.

Understanding Poor Credit Student Loans

When it comes to student loans, having poor credit can significantly impact your eligibility and options. Poor credit can lead to higher interest rates, less favorable repayment terms, and even loan denials. For instance, a student with poor credit may be required to have a co-signer with good credit to secure a loan.

Credit scores play a crucial role in determining loan interest rates, with lower scores resulting in higher interest rates. This means that students with poor credit will likely end up paying more over the life of the loan. For example, a student with a credit score of 620 may qualify for a loan with an interest rate of 8%, while a student with a credit score of 750 may qualify for a loan with an interest rate of 4%.

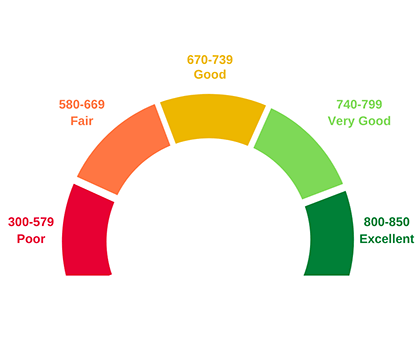

To understand what constitutes poor credit for student loan purposes, it's essential to know the credit score ranges. The following credit scores are generally considered poor:

- 300-579: Bad credit, may struggle to qualify for loans

- 580-619: Poor credit, may qualify for loans with high interest rates

- 620-679: Fair credit, may qualify for loans with moderate interest rates

These credit score ranges can vary depending on the lender and loan type, but they provide a general guideline for students to understand their credit standing.

Students with poor credit can still explore alternative loan options, such as federal student loans, which do not require credit checks. However, these loans often have borrowing limits and may not cover the full cost of attendance. Private lenders may also offer loans to students with poor credit, but these loans often come with higher interest rates and less favorable terms.

To improve their credit scores and increase their loan options, students can focus on making timely payments, reducing debt, and monitoring their credit reports. By taking these steps, students can work towards establishing a positive credit history and becoming more attractive to lenders. This, in turn, can lead to better loan terms, lower interest rates, and a more manageable repayment plan.

Top 5 Student Loans for Bad Credit

As a student with bad credit, finding a suitable loan can be challenging. The Federal Perkins Loan is a great option, offering a low interest rate of 5% and flexible repayment terms. This loan is specifically designed for undergraduate and graduate students who demonstrate exceptional financial need.

The Federal Direct Loan is another viable option, with eligibility criteria based on the student's enrollment status and financial need. To apply, students must complete the Free Application for Federal Student Aid (FAFSA) and meet the general eligibility requirements. The application process typically begins with submitting the FAFSA, which can be done online or through the student's school.

For students who do not qualify for federal loans or need additional funding, private lenders like Sallie Mae or Discover offer student loans to borrowers with poor credit. These lenders often require a co-signer with good credit, which can help reduce the interest rate and increase approval chances. Some popular private lenders include:

- Sallie Mae: offers a range of loan options with competitive interest rates and flexible repayment terms

- Discover: provides loans with no origination fees and a rewards program for good grades

- Wells Fargo: offers loans with competitive interest rates and a variety of repayment options

- Citibank: provides loans with flexible repayment terms and a range of interest rate options

- Ascent: offers loans with no co-signer required and a range of repayment options

When applying for private loans, it's essential to compare rates and terms from multiple lenders to find the best option. Students should also consider factors like repayment flexibility, customer service, and any additional benefits or rewards offered by the lender. By doing their research and exploring all available options, students with bad credit can find a suitable loan to help fund their education.

How to Improve Your Credit for Better Loan Options

Paying bills on time is essential to improving your credit scores. By setting up payment reminders or automating your payments, you can ensure that you never miss a payment. For instance, you can set up automatic transfers from your checking account to your credit card or loan accounts to make timely payments.

Keeping credit utilization ratios low is also crucial in maintaining a healthy credit score. This means that you should keep your credit card balances well below the credit limit. As a general rule, it's a good idea to keep your credit utilization ratio below 30%, which means that if you have a credit limit of $1,000, you should try to keep your balance below $300.

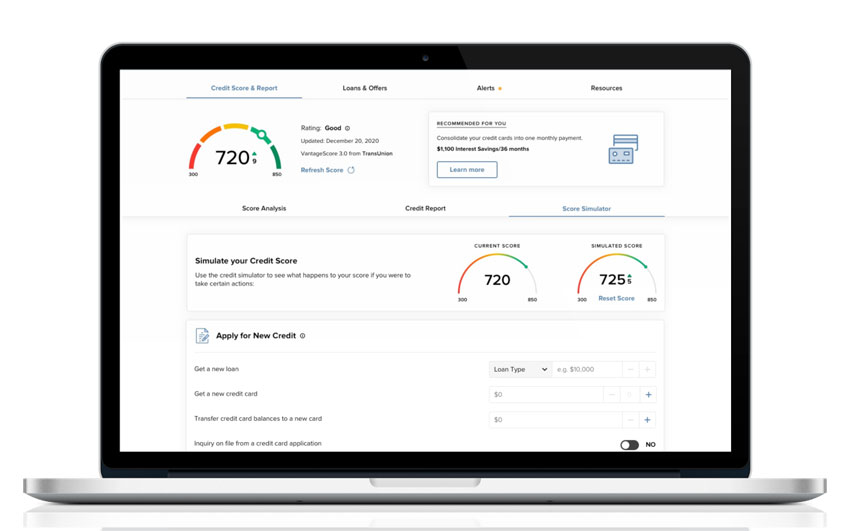

To track and improve your credit scores, you can use credit monitoring services. These services provide you with regular updates on your credit report and score, helping you identify areas for improvement. Some popular credit monitoring services include free options like Credit Karma and paid options like Experian.

Here are some tips to help you improve your credit scores:

- Check your credit report regularly to ensure it's accurate and up-to-date

- Avoid applying for too many credit cards or loans in a short period

- Consider working with a credit counselor if you're struggling to manage your debt

By following these tips and maintaining good credit habits, you can improve your credit scores over time and qualify for better loan options. It's also important to be patient and consistent, as improving your credit score takes time and effort. With persistence and the right strategies, you can achieve a better credit score and enjoy more financial flexibility.

Alternatives to Student Loans for Bad Credit

As a student with bad credit, it can be challenging to secure financial aid for education. However, there are alternatives to student loans that can help. One option is to explore scholarship and grant opportunities, which are often awarded based on merit, need, or other criteria rather than credit score.

Scholarships and grants can be a great way to fund your education without taking on debt. For example, the Pell Grant is a federal grant that awards up to $6,495 to eligible students, and the Federal Supplemental Educational Opportunity Grant (FSEOG) provides additional funding to students with exceptional financial need. You can search for scholarships and grants on websites like Fastweb or Scholarships.com.

Income-driven repayment plans are another option for students with bad credit who have already taken out loans. These plans can help lower your monthly payments by capping them at a percentage of your income.

- The Income-Based Repayment (IBR) plan, for instance, caps payments at 10% or 15% of your discretionary income.

- The Pay As You Earn (PAYE) plan also caps payments at 10% of your discretionary income.

- The Revised Pay As You Earn (REPAYE) plan offers more flexible payment terms, but may not be available to all borrowers.

While income-driven repayment plans can provide relief, they may also increase the total amount you pay over the life of the loan due to interest accrual.

Negotiating with lenders can also be an effective way to secure better loan terms. This can involve contacting your lender to discuss possible alternatives, such as a temporary reduction in payments or a interest rate reduction. For example, you can ask your lender about available hardship programs or forbearance options, which may allow you to temporarily suspend or reduce payments. Be sure to carefully review any new terms before agreeing to them.

It's essential to approach negotiations with a clear understanding of your financial situation and goals. Make a list of your income, expenses, and debts, and be prepared to explain your circumstances to the lender. By being proactive and exploring these alternatives, you can find a solution that works for you and helps you achieve your educational goals.

Conclusion and Next Steps

As we wrap up our discussion on managing student loans, it's essential to remember that taking control of your finances is a journey, not a destination. By understanding your loan options and creating a repayment plan, you can set yourself up for long-term financial success. For instance, considering income-driven repayment plans or loan forgiveness programs can make a significant difference in your monthly payments.

To further explore your student loan options, we recommend checking out the following resources:

- Department of Education's website for information on federal loan programs

- Financial aid offices at your university for guidance on private loan options

- Online forums and communities where you can connect with other students and graduates who have navigated similar situations

These resources can provide valuable insights and help you make informed decisions about your financial aid.

Improving your credit score is also crucial, as it can impact your ability to secure better loan terms or lower interest rates in the future. To get started, you can request a free credit report from the three major credit bureaus and review it for any errors or discrepancies. By taking small steps, such as making on-time payments and keeping credit utilization low, you can begin to build a positive credit history and set yourself up for long-term financial stability.

Now that you've taken the first step by learning more about student loan management, it's time to take action. Start by assessing your current financial situation, creating a budget, and exploring ways to improve your credit score. By doing so, you'll be well on your way to achieving financial freedom and making the most of your investment in higher education.

Frequently Asked Questions (FAQ)

Can I get a student loan with very bad credit?

When it comes to getting a student loan with very bad credit, it's not impossible, but it can be tough. Some lenders offer student loans to borrowers with poor credit, often with less favorable terms, such as higher interest rates or fees. This means you'll need to carefully review and compare the terms of different loans to find the best option for your situation.

To increase your chances of getting approved for a student loan with bad credit, consider having a co-signer with good credit. This can help you qualify for better loan terms and lower interest rates. Having a co-signer can be a great way to get the funding you need, but make sure you both understand the responsibilities and risks involved.

Here are some tips to keep in mind when looking for a student loan with bad credit:

- Research and compare different lenders to find the best rates and terms

- Consider federal student loans, which may have more flexible credit requirements

- Look into credit unions or non-profit lenders that offer more favorable terms

By doing your research and exploring different options, you can find a student loan that works for you, even with very bad credit.

It's also important to note that some lenders specialize in working with borrowers who have poor credit. These lenders may offer more flexible credit requirements, but be sure to carefully review the terms and conditions of the loan. Additionally, be wary of lenders that charge extremely high interest rates or fees, as these can add up quickly and make it difficult to repay the loan.

How can I improve my credit score quickly to get a better student loan?

Establishing a good credit score is essential for students looking to secure better loan options. Paying bills on time is a crucial step in improving credit scores, as it demonstrates responsibility and reliability to lenders. For instance, setting up automatic payments for monthly bills can help ensure that payments are never missed.

Reducing debt is another key factor in improving credit scores, as it shows lenders that you can manage your finances effectively. This can be achieved by creating a budget and prioritizing debt repayment, such as focusing on high-interest loans first. By doing so, you can significantly improve your credit utilization ratio, which is a major contributor to your overall credit score.

To monitor your credit reports, you can request a free copy from the three major credit reporting agencies - Experian, TransUnion, and Equifax - once a year. Here are some ways to improve your credit score:

- Check your credit report for errors and dispute any inaccuracies

- Keep credit utilization below 30% to demonstrate responsible borrowing habits

- Avoid applying for multiple credit cards or loans in a short period, as this can negatively impact your credit score

By following these tips and maintaining good credit habits, you can improve your credit score over time and increase your chances of securing a better student loan.

Are there any student loans that don't require a credit check?

When it comes to financing your education, student loans can be a viable option. Some federal student loans, such as the Federal Direct Loan, don't require a credit check, making them more accessible to students who may not have an established credit history. This is because these loans are backed by the federal government, which assumes the risk of lending to students.

Private lenders, on the other hand, often require a credit check as part of their application process. This is because they want to assess the borrower's creditworthiness and determine the level of risk involved in lending to them. For students who don't have a credit history or have a poor credit score, this can make it more difficult to secure a private student loan.

There are some options available for students who don't have a credit history or prefer not to undergo a credit check. For example, students can consider the following:

- Federal Direct Subsidized Loans, which are available to undergraduate students who demonstrate financial need

- Federal Direct Unsubsidized Loans, which are available to undergraduate and graduate students regardless of financial need

- Federal Perkins Loans, which are available to undergraduate and graduate students who demonstrate exceptional financial need

These loans can provide students with the funding they need to pursue their education without requiring a credit check.

It's worth noting that while some student loans don't require a credit check, they may still have other eligibility requirements, such as being enrolled at least half-time in a degree program or meeting certain income thresholds. Students should carefully review the terms and conditions of any loan before applying to ensure they understand the requirements and any potential risks involved. By doing their research and exploring their options, students can make informed decisions about how to finance their education.