As an international student, pursuing higher education abroad can be a costly affair, and finding the right financial aid is crucial. With numerous loan options available, it can be overwhelming to choose the best one for your needs. To get started, it's essential to assess your financial situation and determine how much you need to borrow.

When exploring loan options, consider factors such as interest rates, repayment terms, and eligibility criteria. For instance, some loans may offer flexible repayment plans or lower interest rates for students with good credit scores. It's also important to research and compare different lenders to find the most suitable option for your study abroad plans.

Here are some key considerations to keep in mind when searching for a loan:

- Interest rates and fees associated with the loan

- Repayment terms and flexibility

- Eligibility criteria, including credit score and income requirements

- Loan amount and disbursement options

By carefully evaluating these factors, you can make an informed decision and find a loan that aligns with your financial goals and study abroad aspirations.

Understanding International Student Loans

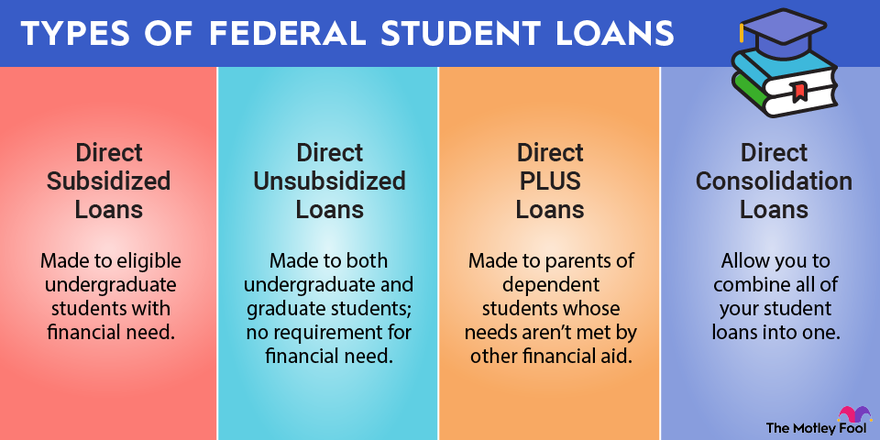

As an international student, navigating the world of student loans can be overwhelming. Federal and private loans are two primary options available, each with its own set of benefits and drawbacks. Federal loans, for instance, often offer more flexible repayment terms and lower interest rates, making them a popular choice among students.

Private loans, on the other hand, may offer more funding options, but they typically come with higher interest rates and less forgiving repayment terms. It's essential to weigh these factors when deciding between federal and private loans. For example, a student from the UK may find that a private loan from a UK-based lender offers more favorable terms than a federal loan from their host country.

Understanding loan terms is crucial for international students, as it can significantly impact their financial situation. Loan terms include interest rates, repayment periods, and associated fees, which can vary greatly between lenders. Students should carefully review these terms to avoid any surprises down the line, such as unexpected fees or repayment deadlines.

Some key loan terms to consider include:

- Interest rates: fixed or variable, and how they may change over time

- Repayment periods: the length of time you have to repay the loan, and any potential penalties for early or late repayment

- Fees: origination fees, late payment fees, and any other charges associated with the loan

Loan options can vary significantly depending on the country and institution. For instance, a student attending a university in the US may have access to federal loans, while a student in Canada may need to rely on private lenders or government-backed loans. Researching these options thoroughly is vital to finding the best fit for your individual circumstances.

Students should research and compare loan options from different lenders and countries to find the most suitable one. For example, a student from Australia may find that a loan from a US-based lender offers more favorable terms than a loan from an Australian lender. By doing their homework, international students can make informed decisions about their student loans and set themselves up for long-term financial success.

In conclusion, international students should prioritize understanding the intricacies of student loans to make the most of their educational experience. By carefully evaluating federal and private loans, loan terms, and options available, students can navigate the complex world of international student loans with confidence.

Top Loan Providers for International Students

As an international student, navigating the complex world of student loans can be overwhelming. Fortunately, several top loan providers cater specifically to international students, offering competitive rates and flexible terms. MPOWER Financing, Prodigy Finance, and Discover Student Loans are among the most popular options.

When it comes to eligibility criteria, each provider has its own set of requirements. For instance, MPOWER Financing offers loans to students from over 200 countries, while Prodigy Finance focuses on providing loans to international students attending top universities worldwide. Discover Student Loans, on the other hand, requires a cosigner for international students.

Here are some key features of each provider:

- MPOWER Financing: offers scholarships and career support services to help students succeed

- Prodigy Finance: provides loans with competitive interest rates and no cosigner required for some students

- Discover Student Loans: offers rewards for good grades and a range of repayment options

These unique features can make a big difference in the overall borrowing experience, so it's essential to research and compare them carefully.

In terms of application processes, each provider has its own online platform. For example, MPOWER Financing offers a simple and straightforward application process, with the option to apply for a loan in just a few minutes. Prodigy Finance, on the other hand, requires students to submit additional documentation, such as proof of admission and financial documents.

International students should also be aware of any specific requirements or restrictions, such as cosigner needs or credit history. For instance, some providers may require a cosigner with a good credit history, while others may not require a cosigner at all. It's crucial to review the terms and conditions carefully before applying for a loan.

Some practical tips for international students include researching multiple providers, reading reviews from other students, and reaching out to customer support teams with any questions or concerns. By doing your homework and comparing your options, you can find the best loan provider to suit your needs and achieve your academic goals.

Applying for International Student Loans

When considering international student loans, it's essential to understand the application process. The first step involves gathering necessary documents, such as proof of admission, passport, and financial statements. This documentation will vary depending on the lender and the country where you plan to study.

To increase your chances of approval, it's crucial to meet deadlines and submit your application well in advance. Missing a deadline can result in delayed funding, which may impact your ability to start classes on time. For example, some lenders may require applications to be submitted 3-6 months before the start of the semester.

Credit checks play a significant role in the application process, as lenders use this information to assess your creditworthiness. International students can build or improve their credit scores by making timely payments on existing debts, keeping credit utilization low, and monitoring their credit reports for errors. By maintaining a good credit score, you can qualify for better interest rates and terms on your loan.

Here are some tips to help you complete the application process efficiently:

- Use online resources, such as loan comparison tools and financial aid websites, to research and find the best loan options for your needs.

- Seek advice from financial aid offices at your university, as they often have experience with international student loans and can provide guidance on the application process.

- Keep track of deadlines and submission requirements using a planner or calendar to ensure you stay on top of the application process.

In addition to these tips, it's also important to carefully review the terms and conditions of your loan before submitting your application. This includes understanding the interest rate, repayment terms, and any fees associated with the loan. By doing your research and seeking advice from financial aid experts, you can make an informed decision and find the best international student loan for your needs.

Finally, don't be discouraged if you encounter obstacles during the application process. Many lenders and financial aid offices offer support and resources specifically for international students, so don't hesitate to reach out for help. With persistence and the right guidance, you can successfully navigate the application process and secure the funding you need to achieve your academic goals.

Managing and Repaying International Student Loans

As an international student, managing loan debt can be overwhelming, especially when navigating a new country and education system. Creating a budget is essential to keeping track of expenses and loan payments. By allocating a fixed amount each month towards loan repayment, you can ensure timely payments and avoid late fees.

When it comes to repayment, income-driven plans can be a lifesaver, as they tie monthly payments to your income level. For example, the Income-Based Repayment (IBR) plan can cap your monthly payments at 10% to 15% of your discretionary income. This can be a huge relief, especially during periods of financial hardship.

Loan forgiveness options are also available, such as Public Service Loan Forgiveness (PSLF), which can forgive remaining balances after 10 years of qualifying payments. To be eligible, you must work full-time for a qualifying employer, such as a government agency or non-profit organization. Additionally, some employers offer loan repayment assistance as a benefit, so it's worth exploring these options.

Navigating repayment terms can be complex, but understanding the differences between deferment, forbearance, and consolidation is crucial.

- Deferment allows you to temporarily postpone payments due to financial hardship or enrollment in school.

- Forbearance is a temporary suspension of payments, usually due to financial difficulties.

- Consolidation combines multiple loans into a single loan with a fixed interest rate and repayment term.

Each option has its pros and cons, so it's essential to weigh the benefits and potential drawbacks before making a decision.

If you're struggling to manage your loan debt, don't hesitate to seek help. Financial counseling services, such as the National Foundation for Credit Counseling (NFCC), offer free or low-cost advice and guidance. Online forums, like Reddit's r/StudentLoans, can also connect you with others who are facing similar challenges, providing a sense of community and support. By taking proactive steps and seeking help when needed, you can successfully manage and repay your international student loans.

Alternatives to International Student Loans

As an international student, exploring alternative funding options can help reduce your reliance on loans. Scholarships and grants are excellent alternatives, offering free money that doesn't need to be repaid. For instance, the Fulbright Scholarship and the Rotary International Scholarship are popular options for international students.

When considering personal savings, it's essential to start planning early, as this can be a significant source of funding. Setting aside a portion of your income each month or using tax-advantaged savings accounts can help you build a sizable fund. Additionally, exploring tax benefits and incentives for education savings can also be beneficial.

Side hustles and part-time jobs can also play a significant role in reducing your reliance on loans. By working part-time, you can earn money to cover living expenses, tuition fees, or other education-related costs. Some popular side hustles for international students include:

- Tutoring or teaching languages online

- Freelance writing or graphic design

- Part-time jobs on campus, such as research assistants or library staff

These side hustles can help you earn a steady income while pursuing your studies.

Crowdfunding and community-based funding initiatives are innovative solutions that can help international students raise funds for their education. Platforms like GoFundMe and Kickstarter allow you to create campaigns and share them with your network, while community-based initiatives like church or community organization sponsorships can also provide significant funding. By exploring these alternatives, you can reduce your reliance on loans and create a more sustainable financial plan for your education.

It's also worth noting that some universities and colleges offer emergency loans or grants to international students, which can be a useful safety net in times of financial need. Be sure to research these options and reach out to your university's financial aid office to learn more. By being proactive and exploring alternative funding options, you can take control of your finances and achieve your academic goals.

Frequently Asked Questions (FAQ)

What are the eligibility criteria for international student loans?

As an international student, securing a loan can be a crucial step in funding your education abroad. Eligibility criteria for these loans vary by lender, but often include factors like citizenship, credit history, and enrollment status. Understanding these criteria is essential to determine which loans you may be eligible for.

Citizenship is a key factor, as lenders typically have specific requirements for borrowers from certain countries. For example, some lenders may only offer loans to students from countries with a strong credit history or economic stability. It's essential to check with lenders to see if they offer loans to students from your country of origin.

Credit history also plays a significant role in determining eligibility, as lenders want to assess your ability to repay the loan. If you have a limited or no credit history, you may need to apply with a co-signer who has a good credit score. Lenders may also consider other factors, such as:

- Enrollment status, including full-time or part-time attendance

- Field of study, with some lenders offering loans for specific programs

- Income level, with some lenders requiring a minimum income threshold

These factors can vary depending on the lender and the specific loan program, so it's crucial to review the eligibility criteria carefully.

To increase your chances of getting approved for an international student loan, it's essential to maintain a good credit history, enroll in an eligible program, and meet the lender's income requirements. You can also consider applying with a co-signer or exploring loan options that don't require a co-signer. By understanding the eligibility criteria and taking steps to meet them, you can secure the funding you need to achieve your educational goals.

Can international students get loans without a cosigner?

As an international student, navigating the world of student loans can be overwhelming. Many lenders require a cosigner, typically a US citizen or permanent resident, to guarantee the loan. However, some lenders offer no-cosigner loans, providing an alternative for students who do not have a cosigner.

These no-cosigner loans often come with stricter eligibility criteria, such as a higher GPA or enrollment in a specific program. Additionally, interest rates may be higher compared to traditional loans with a cosigner. For example, a student with a good academic record may qualify for a no-cosigner loan, but the interest rate might be 1-2% higher than a similar loan with a cosigner.

To increase their chances of getting approved for a no-cosigner loan, international students can:

- Research lenders that specialize in no-cosigner loans, such as MPOWER Financing or Prodigy Finance

- Review and understand the loan terms, including interest rates and repayment conditions

- Prepare a solid application, including proof of admission, academic transcripts, and financial documents

By carefully evaluating their options and choosing a lender that aligns with their needs, international students can find a no-cosigner loan that helps them achieve their educational goals.

It's essential for international students to consider the long-term implications of a no-cosigner loan, including the potential for higher interest rates and stricter repayment terms. By weighing the pros and cons and exploring different lenders, students can make an informed decision that works best for their financial situation. With the right loan and a solid understanding of the terms, international students can focus on their studies and build a successful future.

How do international student loans affect credit scores?

As an international student, managing your finances effectively is crucial, especially when it comes to student loans. Making timely payments on international student loans can help build credit, which is essential for future financial endeavors. By doing so, you can establish a positive credit history, making it easier to secure loans, credit cards, or even an apartment in the future.

One of the most significant factors that affect credit scores is payment history, which accounts for about 35% of your credit score. If you miss payments or make late payments on your international student loans, it can negatively impact your credit score. For instance, a single missed payment can drop your credit score by as much as 100 points, making it challenging to recover.

To maintain a good credit score, it's essential to make timely payments on your international student loans. Here are some tips to help you stay on track:

- Set up automatic payments to ensure you never miss a payment

- Keep track of your payment due dates and amounts

- Communicate with your lender if you're facing financial difficulties

By following these tips, you can avoid missed payments and build a positive credit history, which will benefit you in the long run.

In addition to making timely payments, it's also important to monitor your credit report regularly to ensure there are no errors or inaccuracies. You can request a free credit report from the three major credit bureaus once a year, which will help you stay on top of your credit score. By being proactive and responsible with your international student loans, you can build a strong credit foundation and achieve financial stability.