As a young adult, navigating the world of student loans can be overwhelming. Private student loans are a vital option for many students, filling the gap between federal aid and the actual cost of attending college. For instance, if you're pursuing a degree in a field with high tuition fees, private student loans can help cover the expenses that federal loans may not.

Private student loans are offered by banks, credit unions, and other lenders, providing an alternative to federal student loans. These loans often have varying interest rates and repayment terms, making it essential to carefully review and compare options before making a decision. It's crucial to consider factors like interest rates, fees, and repayment flexibility when choosing a private student loan.

When exploring private student loan options, consider the following key factors:

- Interest rates: fixed or variable, and how they may impact your monthly payments

- Repayment terms: flexible repayment plans, deferment, or forbearance options

- Fees: origination fees, late payment fees, or other charges associated with the loan

Understanding these factors can help you make an informed decision about which private student loan is right for you. By doing your research and carefully evaluating your options, you can find a private student loan that meets your needs and helps you achieve your educational goals.

Understanding Private Student Loans

When it comes to financing your education, you have two primary options: federal student loans and private student loans. Private student loans are offered by banks, credit unions, and other lenders, and they differ significantly from federal loans in terms of interest rates and repayment terms. For instance, federal loans have fixed interest rates, while private loans often have variable rates that can fluctuate over time.

Private student loans can be a good option for students who have exhausted their federal loan options or need additional funding. The benefits of private student loans include flexibility in repayment, as some lenders offer income-driven repayment plans or temporary hardship forbearance. Additionally, private loans may offer potentially lower interest rates, especially for borrowers with excellent credit scores.

To be eligible for a private student loan, you'll typically need a good credit score, as lenders use this to determine your creditworthiness. Your credit score can also impact the interest rate you're offered, with higher scores resulting in lower rates. For example, a borrower with a credit score of 750 may qualify for a 4.5% interest rate, while a borrower with a score of 650 may be offered a 7% rate.

Here are some key factors to consider when evaluating private student loan options:

- Interest rates: Look for lenders offering competitive, fixed or variable rates

- Repayment terms: Consider lenders with flexible repayment plans, such as income-driven repayment or graduated repayment

- Fees: Check for origination fees, late payment fees, or other charges that can add to your overall cost

Before applying for a private student loan, it's essential to review your credit report and work on improving your credit score if necessary. You can do this by paying bills on time, reducing debt, and avoiding new credit inquiries. By taking these steps, you can increase your chances of qualifying for a private student loan with a favorable interest rate and repayment terms.

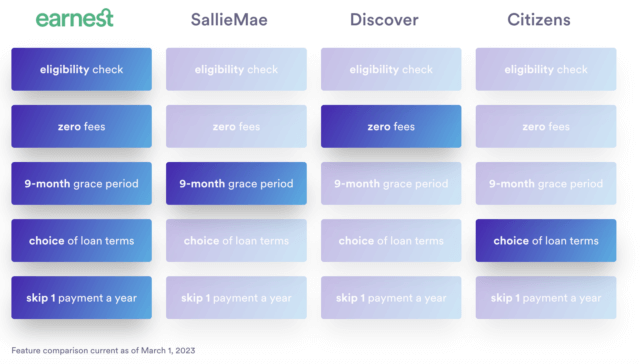

Top Private Student Loan Lenders for 2025

When it comes to funding your education, private student loans can be a viable option. Top lenders offer competitive interest rates and flexible repayment terms, making it easier to manage your debt. For instance, lenders like Sallie Mae and Discover offer variable interest rates ranging from 2.50% to 12.99%, depending on your credit score and other factors.

Some private student loan lenders stand out for their unique features, such as flexible repayment options or forbearance policies. These features can be a lifesaver if you're facing financial difficulties. For example, College Ave offers a 4-month forbearance period, allowing you to temporarily suspend payments if you're experiencing hardship.

Here are some top private student loan lenders to consider:

- Sallie Mae: offers variable interest rates from 2.50% to 12.99% and a 0.25% interest rate reduction for automatic payments

- Discover: provides variable interest rates from 3.49% to 12.99% and a 1% cash reward for good grades

- College Ave: offers variable interest rates from 2.99% to 12.99% and a range of repayment terms, including 5- to 15-year options

These lenders often have similar application processes, requiring documentation such as proof of enrollment, income verification, and a credit check.

The application process typically involves submitting an online application, providing required documents, and reviewing the loan terms before accepting the offer. It's essential to carefully review the loan agreement and ask questions if you're unsure about any aspect of the loan. For example, you may want to ask about the lender's policy on co-signers or how to apply for a forbearance period.

Repayment terms vary among lenders, but most offer options such as deferred payments, interest-only payments, or full payments. Some lenders, like SoFi, offer unemployment protection, which can pause payments if you lose your job. It's crucial to understand the repayment terms and choose a lender that aligns with your financial situation and goals.

How to Choose the Best Private Student Loan

When it comes to choosing a private student loan, there are several key factors to consider. Interest rates, fees, and repayment terms are all crucial elements that can impact the overall cost of the loan. For example, a loan with a lower interest rate may save you thousands of dollars in interest payments over the life of the loan.

To compare loan offers, it's essential to review the terms and conditions carefully. This includes looking at the interest rate, origination fees, and repayment terms. You can use online tools to compare loan offers from different lenders, such as a loan comparison calculator, to determine which loan is the best fit for your needs.

Here are some key factors to consider when choosing a private student loan:

- Interest rates: fixed or variable, and how they may change over time

- Fees: origination fees, late payment fees, and other charges

- Repayment terms: length of the repayment period, and options for deferment or forbearance

By considering these factors, you can make an informed decision about which loan is right for you.

Negotiating with lenders is also an option, and it's worth asking about potential discounts or flexible repayment terms. Some lenders may offer discounts for automatic payments or good grades, so it's worth inquiring about these options. Additionally, you can ask about the possibility of releasing a co-signer from the loan after a certain number of payments.

It's also essential to read and understand the loan terms and conditions before signing any agreements. This includes reviewing the fine print and asking questions about any terms you don't understand. By taking the time to carefully review the loan terms, you can avoid any surprises or unexpected charges down the line.

In addition to reviewing the loan terms, it's a good idea to ask questions and seek guidance from a financial advisor if needed. This can help you make a more informed decision and ensure that you're getting the best possible loan for your needs. By doing your research and carefully comparing loan offers, you can find a private student loan that works for you and helps you achieve your educational goals.

Managing Private Student Loan Debt

When dealing with private student loan debt, it's essential to understand the various management options available. Income-driven repayment plans can help lower monthly payments, although they may not be as widely available for private loans as they are for federal loans. For example, some lenders may offer income-sensitive repayment plans that can help borrowers manage their debt.

To tackle private student loan debt, borrowers can consider consolidation options, which involve combining multiple loans into one loan with a single interest rate and monthly payment. This can simplify the repayment process and potentially lower monthly payments. However, consolidation may not always be the best option, so it's crucial to weigh the pros and cons before making a decision.

Some key considerations for managing private student loan debt include:

- Communicating with lenders to discuss possible repayment options

- Exploring income-driven repayment plans or consolidation

- Seeking assistance from credit counseling services if needed

Refinancing private student loans can also be a viable option, but it's essential to understand the pros and cons, such as potentially lower interest rates but also the loss of certain borrower benefits.

Refinancing can be beneficial for borrowers who have improved their credit score since taking out the original loan, as they may qualify for a lower interest rate. On the other hand, refinancing may not be the best option for borrowers who are struggling to make payments, as it may not address the underlying issue. Borrowers should carefully evaluate their financial situation before making a decision.

For borrowers struggling with private student loan debt, there are resources available, such as credit counseling services that can provide personalized advice and guidance. The National Foundation for Credit Counseling (NFCC) is a non-profit organization that offers credit counseling and education to help borrowers manage their debt. Additionally, many lenders offer assistance programs or hardship options that can help borrowers temporarily suspend or reduce payments.

Alternatives to Private Student Loans

When it comes to funding your education, private student loans are not the only option. Exploring alternative funding options can help you avoid debt and make your educational journey more affordable. Consider looking into scholarships, grants, and work-study programs, which can provide significant financial assistance without the burden of loans.

One of the most effective ways to fund your education is through scholarships and grants. These can be merit-based or need-based, and there are numerous organizations and institutions that offer them. For example, you can search for scholarships on websites like Fastweb or Scholarships.com, which provide a wide range of opportunities for students.

In addition to external funding, you can also consider using personal savings or assistance from family and friends. This can be a good option if you have a supportive network or have been able to save up over time. However, it's essential to discuss the benefits and drawbacks of this approach, such as the potential impact on your relationships or the risk of depleting your savings.

Some of the benefits of using personal savings or assistance from family and friends include:

- Avoiding debt and interest payments

- Maintaining control over your finances

- Building a support network of loved ones

On the other hand, some drawbacks to consider are:

- Depleting your savings or emergency fund

- Potentially straining relationships

- Limited financial assistance

Another innovative way to fund your education is by starting a side hustle or exploring entrepreneurship. This can be a great way to earn money while pursuing your studies, and can even lead to long-term career opportunities. Consider freelancing, tutoring, or starting a small business to help cover your educational expenses and gain valuable work experience.

Frequently Asked Questions (FAQ)

What are the eligibility requirements for private student loans?

When considering private student loans, it's essential to understand the eligibility requirements. Eligibility typically depends on credit score, income, and enrollment status, which can vary between lenders. A good credit score can significantly improve your chances of getting approved for a private student loan.

To qualify for a private student loan, you'll usually need to meet specific credit score requirements, which can range from 600 to 700 or higher. For example, if you have a limited credit history, you may need to apply with a co-signer who has a good credit score. This can help you qualify for a loan with a more favorable interest rate.

Here are some key factors that lenders consider when evaluating your eligibility:

- Credit score: A good credit score can help you qualify for better interest rates and terms

- Income: You or your co-signer may need to meet minimum income requirements to demonstrate repayment ability

- Enrollment status: You'll typically need to be enrolled at least half-time in a degree-granting program to qualify for a private student loan

It's crucial to review the eligibility requirements for each lender and compare them to your individual circumstances. By doing so, you can increase your chances of getting approved for a private student loan that meets your needs.

If you're struggling to meet the eligibility requirements, consider working on your credit score or finding a co-signer with a good credit history. You can also explore other financing options, such as federal student loans or scholarships, which may have more lenient eligibility requirements. By taking the time to understand the eligibility requirements and exploring your options, you can make informed decisions about funding your education.

Can I consolidate or refinance private student loans?

Consolidating or refinancing private student loans can be a viable option for managing debt. This process involves combining multiple loans into one loan with a single interest rate and payment, which can simplify your finances. For instance, if you have multiple private loans with high interest rates, consolidating them into a single loan with a lower rate can save you money on interest.

To consolidate or refinance private student loans, you typically need to meet certain eligibility criteria, such as having a good credit score and a stable income. Lenders may also consider factors like your debt-to-income ratio and credit history when determining your eligibility. It's essential to review the terms and conditions of any consolidation or refinancing offer carefully to ensure it's the right choice for your financial situation.

Some benefits of consolidating or refinancing private student loans include:

- Lower monthly payments: By extending the repayment period or lowering the interest rate, you may be able to reduce your monthly payments.

- Simplified finances: Combining multiple loans into one can make it easier to keep track of your debt and make payments on time.

- Potential interest savings: If you can secure a lower interest rate, you may save money on interest over the life of the loan.

However, there are also potential drawbacks to consider, such as losing certain benefits or protections associated with your original loans.

When exploring consolidation or refinancing options, it's crucial to weigh the pros and cons carefully and consider your individual circumstances. You may want to consult with a financial advisor or credit counselor to determine the best course of action for your specific situation. Additionally, be sure to research and compare offers from multiple lenders to find the most favorable terms.

How do private student loans affect my credit score?

When it comes to private student loans, understanding their impact on your credit score is essential for maintaining good financial health. Your payment history and debt-to-income ratio are two key factors that can influence your credit score. For instance, missing a payment or defaulting on a loan can significantly lower your credit score, making it harder to secure loans or credit in the future.

To minimize the negative impact of private student loans on your credit score, it's crucial to make timely payments and keep your debt-to-income ratio in check. You can do this by creating a budget and prioritizing your loan payments. Additionally, consider setting up automatic payments to ensure you never miss a payment.

Here are some ways to manage your private student loans and protect your credit score:

- Make all payments on time to demonstrate responsible credit behavior

- Keep your debt-to-income ratio below 30% to show lenders you can manage your debt

- Monitor your credit report regularly to catch any errors or discrepancies

By following these tips and being mindful of your payment history and debt-to-income ratio, you can minimize the negative impact of private student loans on your credit score and maintain a healthy financial profile. Regularly reviewing your credit report can also help you identify areas for improvement and make informed decisions about your financial future.