As a student or parent, navigating the world of financial aid can be overwhelming, especially when it comes to understanding the various forms and requirements. One crucial aspect of this process is completing the Free Application for Federal Student Aid (FAFSA), which helps determine eligibility for student aid. By understanding the income limits associated with FAFSA, individuals can better assess their potential for receiving financial assistance.

The FAFSA income limits are not necessarily cut-and-dry, as they take into account a range of factors, including family size, income, and assets. For instance, a family of four with a combined income of $50,000 may be eligible for more aid than a family of two with the same income. To get a better sense of how these limits work, it's essential to review the FAFSA guidelines and use online tools to estimate your expected family contribution (EFC).

Some key factors to consider when evaluating FAFSA income limits include:

- Household income: This includes the income of both parents, as well as any additional income earned by the student

- Family size: The number of people in the household can significantly impact the EFC and subsequent aid eligibility

- Assets: Certain assets, such as savings accounts and investments, may be considered when determining the EFC

By carefully evaluating these factors and understanding how they impact FAFSA income limits, students and parents can make more informed decisions about their financial aid options and develop a plan to fund their education.

What are FAFSA Income Limits?

When it comes to determining student aid eligibility, FAFSA income limits play a significant role. The Free Application for Federal Student Aid (FAFSA) takes into account an individual's income to calculate their Expected Family Contribution (EFC), which in turn affects the amount of aid they can receive. This is why understanding FAFSA income limits is crucial for students and families seeking financial assistance.

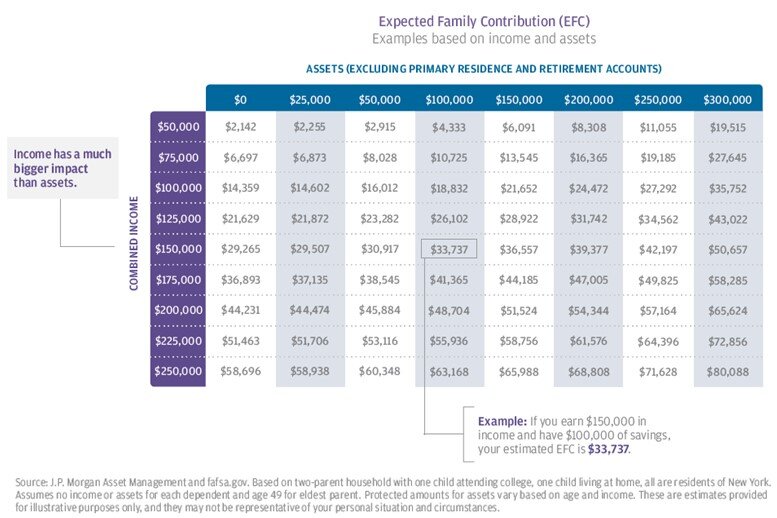

The concept of FAFSA income limits is not about cutting off eligibility at a specific income level, but rather about assessing a family's financial situation to determine their ability to contribute to educational expenses. For instance, a family with a higher income may be expected to contribute more towards their child's education, while a family with a lower income may be eligible for more aid. This is reflected in the EFC calculation, which considers factors such as income, assets, and family size.

Here are some key factors that are considered when calculating FAFSA income limits:

- Gross income from the previous tax year

- Number of family members in college

- Family size and dependency status

- Assets, such as savings and investments

These factors help determine the EFC, which can significantly impact the amount of aid a student receives. For example, a student from a low-income family may be eligible for a full Pell Grant, while a student from a higher-income family may only be eligible for a partial grant or no grant at all.

Accurately reporting income on the FAFSA application is essential to ensure that students receive the aid they are eligible for. Even small discrepancies in reported income can affect the EFC and ultimately the amount of aid received. To avoid errors, it's a good idea to gather all necessary financial documents, including tax returns and W-2 forms, before filling out the FAFSA application. This will help ensure that income is reported accurately and that students receive the financial assistance they need to pursue their educational goals.

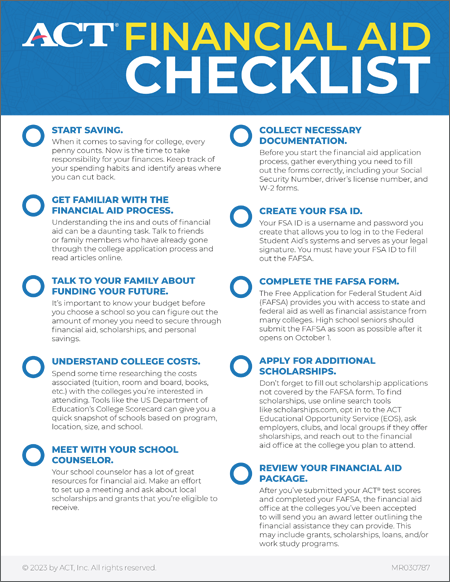

How to Determine Your Eligibility

To determine your eligibility for student aid, start by gathering all the required documents, including your social security number, driver's license, and tax returns. This will help you fill out the Free Application for Federal Student Aid (FAFSA) form, which is the first step in applying for financial aid. Make sure to check the official FAFSA website for the most up-to-date list of required documents.

The next step is to understand whether you are a dependent or independent student, as this affects your eligibility for aid. Generally, dependent students are those who are under 24 years old and are unmarried, while independent students are those who are married, have dependents, or are veterans. For example, if you are a dependent student, your parents' income will be taken into account when determining your eligibility for aid.

The Expected Family Contribution (EFC) plays a significant role in determining aid eligibility, as it represents the amount that you and your family are expected to contribute towards your education. The EFC is calculated based on your FAFSA application and takes into account factors such as income, assets, and family size. Here are some factors that affect your EFC:

- Income: Your income, as well as your parents' income if you are a dependent student

- Assets: Your savings, investments, and other assets, such as property or businesses

- Family size: The number of people in your household, including dependents

To get an estimate of your EFC, you can use the FAFSA4caster tool on the official FAFSA website. This tool will ask you for some basic information, such as your income and family size, and provide you with an estimated EFC. For instance, if your EFC is low, you may be eligible for more need-based aid, such as grants and subsidized loans.

It's essential to note that the EFC is not the same as the amount you will actually pay for college. Rather, it's a measure of your family's financial strength and is used to determine your eligibility for federal, state, and institutional aid. By understanding how the EFC is calculated and how it affects your aid eligibility, you can make informed decisions about your financial aid options and create a plan to fund your education.

Tips for Maximizing Your Aid Eligibility

To maximize your aid eligibility, it's essential to minimize your income. One effective strategy is to contribute to tax-advantaged retirement accounts, such as a 401(k) or an IRA, as these contributions are tax-deductible and can reduce your taxable income. By doing so, you can lower your income level, which can lead to a higher aid eligibility.

When it comes to assets, such as savings and investments, it's crucial to understand their impact on aid eligibility. Generally, assets held in a student's name have a more significant impact on aid eligibility than those held in a parent's name. For example, if a student has a savings account in their name, it may be considered an asset and could reduce their aid eligibility.

Here are some tips to minimize the impact of assets on aid eligibility:

- Consider holding assets in a parent's name, such as a 529 college savings plan, to reduce the impact on aid eligibility

- Use assets to pay for education expenses, such as tuition or room and board, to reduce the amount of aid needed

- Keep in mind that some assets, such as retirement accounts, are not considered when calculating aid eligibility

Negotiating with the financial aid office can also be an effective way to secure additional assistance. If you've experienced a change in financial circumstances, such as a job loss or medical emergency, be sure to reach out to the financial aid office to discuss your options. They may be able to offer additional aid or adjust your aid package to reflect your new financial situation.

It's also essential to be prepared when negotiating with the financial aid office. Make sure to gather all relevant financial documents, such as tax returns and proof of income, to support your request for additional aid. By being proactive and prepared, you can increase your chances of securing the aid you need to fund your education.

Common Mistakes to Avoid

When it comes to completing the FAFSA application, timing is everything. Missing deadlines can significantly reduce or even eliminate aid eligibility, so it's crucial to mark those important dates on your calendar. For instance, submitting your application as early as possible can increase your chances of receiving more aid, as some types of aid are awarded on a first-come, first-served basis.

Misreporting income or assets on the FAFSA application can have serious consequences, including reduced or denied aid, and even repayment of previously awarded aid. It's essential to accurately report your financial information to avoid any potential issues. For example, forgetting to include a parent's income or assets can lead to a significant reduction in aid eligibility.

To avoid common mistakes, it's vital to verify all the information before submitting the application. Here are some key things to double-check:

- Make sure to report all income and assets accurately, including investments and savings accounts

- Verify your social security number and date of birth to ensure they match the information on file with the Social Security Administration

- Check that you have included all required documents and signatures

By taking the time to review and verify your application, you can help ensure that you receive the aid you're eligible for and avoid any potential problems down the line.

Another common mistake to avoid is assuming you won't qualify for aid, so you don't bother applying. However, many students who think they won't qualify are often surprised to find that they do, in fact, qualify for some type of aid. By completing the FAFSA application, you can determine your eligibility for various types of aid, including grants, loans, and work-study programs.

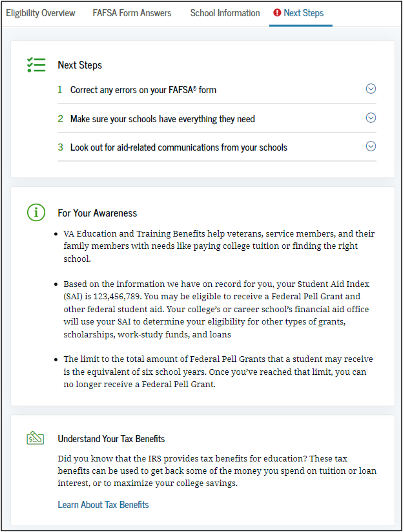

Next Steps After Submitting the FAFSA

After submitting the FAFSA, it's essential to review the Student Aid Report (SAR) carefully. The SAR is a summary of the information you provided on the FAFSA, and it will help you understand your eligibility for federal, state, and institutional financial aid. Check the SAR for any errors or discrepancies, and make corrections as needed.

Once you receive the SAR, you'll start getting financial aid award letters from the schools you've applied to. To compare aid packages, make a list of the types and amounts of aid offered by each school, including grants, loans, and work-study programs. Consider the total cost of attendance, as well as any additional fees or expenses, when evaluating each package.

Here are some key factors to consider when comparing aid packages:

- Cost of attendance, including tuition, fees, room, and board

- Total amount of aid offered, including grants, loans, and work-study programs

- Types of loans offered, such as subsidized or unsubsidized federal loans

- Any additional requirements, such as verification or counseling

Some schools may offer more generous aid packages, but it's crucial to consider the overall cost and value of each institution. For example, a school with a higher sticker price may offer more aid, but the net cost could still be higher than a school with a lower sticker price and less aid.

Completing any additional requirements is vital to securing your financial aid. This may include verification, which involves providing documentation to confirm the information on your FAFSA, or counseling, which helps you understand your loan options and responsibilities. Be sure to check with each school to determine what additional requirements you need to complete and by when.

By carefully reviewing your SAR, comparing aid packages, and completing any additional requirements, you'll be well on your way to making an informed decision about which school to attend and how to finance your education. Remember to stay organized, ask questions if you're unsure, and seek help if you need it – and you'll be navigating the financial aid process like a pro.

Frequently Asked Questions (FAQ)

What is the income limit for FAFSA 2025?

When it comes to determining the income limit for FAFSA 2025, it's essential to understand that there is no one-size-fits-all answer. The income limit varies depending on family size and other factors, such as the number of family members in college and the family's assets. This means that families with similar incomes may have different eligibility for financial aid.

To give you a better idea, the FAFSA considers several factors, including:

- Family size and the number of family members in college

- Gross income from the previous tax year

- Assets, such as savings and investments

- Benefits, like Social Security or veterans' benefits

These factors help determine the Expected Family Contribution (EFC), which is used to calculate the amount of financial aid a student is eligible to receive.

For example, a family of four with two children in college may have a higher income limit than a family of two with one child in college. Additionally, families with lower incomes or more family members in college may be eligible for more financial aid. It's crucial to fill out the FAFSA form accurately and thoroughly to ensure you receive the most financial aid possible.

How does the FAFSA determine income limits?

To determine income limits, the FAFSA uses a formula to calculate the Expected Family Contribution (EFC) based on income, assets, and other factors. This calculation takes into account the family's income, benefits, and assets, as well as the number of family members in college. The goal is to provide a fair and accurate assessment of a family's ability to pay for college expenses.

The formula considers various income sources, including wages, salaries, and tips, as well as benefits like Social Security and veterans' benefits. It also looks at assets such as savings, investments, and real estate, excluding the family's primary home. By evaluating these factors, the FAFSA can determine the EFC, which is the amount the family is expected to contribute towards college costs.

Here are some key factors that influence the EFC calculation:

- Parent income and benefits

- Student income and benefits

- Assets, such as savings and investments

- Family size and number of family members in college

- State and federal tax paid

For example, a family with two working parents, two children, and significant savings will likely have a higher EFC than a family with one working parent, three children, and limited savings. By understanding how the FAFSA calculates the EFC, families can better estimate their eligibility for federal, state, and institutional financial aid.

It's essential to note that the FAFSA does not use a simple income cutoff to determine eligibility for financial aid. Instead, it considers the family's overall financial situation, including income, assets, and expenses. This approach helps ensure that aid is targeted to those who need it most, while also providing opportunities for middle- and higher-income families to receive some level of assistance. By completing the FAFSA, families can access a range of financial aid options, including grants, loans, and work-study programs, to help make college more affordable.

Can I still receive aid if my family income is above the limit?

When it comes to receiving financial aid, many students and their families assume that having an income above a certain limit automatically disqualifies them from receiving assistance. However, this is not always the case. Depending on other factors such as family size and assets, it's possible to receive aid even if your family income is above the limit.

Family size plays a significant role in determining aid eligibility, as larger families are often considered to have a higher cost of living. For example, a family of four with an income of $100,000 may be eligible for more aid than a family of two with the same income. This is because the cost of living for a larger family is typically higher, leaving less disposable income for education expenses.

Some key factors that can affect aid eligibility, even with an income above the limit, include:

- Family size and number of dependents

- Assets, such as savings and investments

- Number of family members attending college

- Other financial obligations, such as debts or medical expenses

By considering these factors, financial aid officers can get a more accurate picture of a family's financial situation and determine whether they are eligible for assistance. It's essential to fill out the Free Application for Federal Student Aid (FAFSA) to see what options are available, even if you think your family income is above the limit.

Practical tips for maximizing aid eligibility include minimizing assets, such as savings and investments, and avoiding large purchases or financial transactions before applying for aid. Additionally, keeping track of expenses and financial obligations can help demonstrate a family's financial need and increase their chances of receiving assistance. By understanding the factors that affect aid eligibility and taking steps to maximize their chances, students and their families can access the financial resources they need to pursue higher education.