As a member of Gen Z, you're likely no stranger to the concept of financial independence. With the rising cost of living and an increasingly competitive job market, it's more important than ever to develop smarter money habits that will set you up for success. By adopting a proactive approach to your finances, you can achieve your long-term goals and enjoy a more secure financial future.

One key aspect of smarter money habits is exploring side hustles that can supplement your primary income. This could be anything from freelancing or selling products online to participating in the gig economy or renting out a spare room on Airbnb. For example, if you have a talent for writing or graphic design, you could offer your services on freelance platforms like Upwork or Fiverr.

In addition to side hustles, investing is another crucial component of building wealth over time. By starting to invest early, you can take advantage of compound interest and potentially earn significant returns on your money. Some popular investment options for beginners include:

- Index funds or ETFs, which provide broad diversification and tend to be low-cost

- Robo-advisors, which offer automated investment management and professional guidance

- Crypto or blockchain-based investments, which can be more high-risk but also offer potential for high rewards

When it comes to investing, it's essential to do your research and consider your individual financial goals and risk tolerance before making any decisions.

By combining side hustles and investing, you can create a powerful financial foundation that will serve you well throughout your life. Whether you're looking to pay off student loans, build up your savings, or achieve long-term financial independence, the key is to start taking action and making progress towards your goals. With the right mindset and strategies, you can overcome any financial challenges and achieve a brighter financial future.

Building Side Hustles for Financial Freedom

To achieve financial freedom, it's essential to explore opportunities beyond your primary income source. Building side hustles can help you earn extra money, pay off debt, and create a safety net. By identifying profitable skills to monetize, such as writing, designing, or coding, you can turn your passions into lucrative ventures.

One of the most significant advantages of side hustles is the ability to utilize online platforms to find clients. Websites like Upwork, Fiverr, or Freelancer offer a vast marketplace for freelancers to showcase their skills and connect with potential clients. For instance, if you have a talent for writing, you can create a profile on these platforms and bid on projects that match your expertise.

Creating a schedule is crucial to balance your side hustles with primary responsibilities, such as work or study. This will help you avoid burnout and ensure that your side hustles complement your existing commitments. Here are some tips to get you started:

- Set aside dedicated time for your side hustles, such as evenings or weekends

- Prioritize tasks and focus on high-earning activities

- Use time-management tools, like calendars or apps, to stay organized

As you build your side hustles, it's essential to be flexible and adapt to changing circumstances. Be open to learning new skills, taking on new challenges, and adjusting your strategy as needed. With persistence and dedication, you can turn your side hustles into a reliable source of income and move closer to achieving financial freedom. By diversifying your income streams, you'll be better equipped to handle financial setbacks and make progress towards your long-term goals.

Introduction to SIPs and Investing

When it comes to investing, one of the most popular and effective ways to grow your wealth is through Systematic Investment Plans, or SIPs. This approach allows you to invest a fixed amount of money at regular intervals, helping you to reduce the impact of market volatility and timing risks. By doing so, you can make the most of the power of compounding and potentially earn higher returns over the long term.

To get started with SIPs, it's essential to research and choose the right investment options, such as mutual funds or stocks, that align with your financial goals and risk tolerance. You can consider factors like the fund's historical performance, expense ratio, and investment strategy to make an informed decision. For instance, if you're a beginner, you may want to opt for a diversified equity mutual fund that spreads risk across various sectors and asset classes.

Before investing, it's crucial to set clear financial goals, such as saving for a car, education, or retirement. This will help you determine the right investment amount, tenure, and risk level for your SIP. You can ask yourself questions like: What am I investing for? How much can I afford to invest each month? And when do I need the money?

Some benefits of SIPs include:

- Reduced timing risk, as you invest a fixed amount at regular intervals

- Averaging out market volatility, which can help you earn higher returns over the long term

- Disciplined investing, which encourages you to invest regularly and avoid emotional decisions

By understanding these benefits and setting clear financial goals, you can make the most of SIPs and achieve your investment objectives.

To choose the right investment option, consider the following factors:

- Risk tolerance: How much risk are you willing to take, and what's your capacity to absorb potential losses?

- Investment horizon: When do you need the money, and how long can you afford to stay invested?

- Financial goals: What are you investing for, and how much do you need to achieve your goals?

By considering these factors and doing your research, you can make informed investment decisions and create a tailored SIP plan that suits your needs and goals.

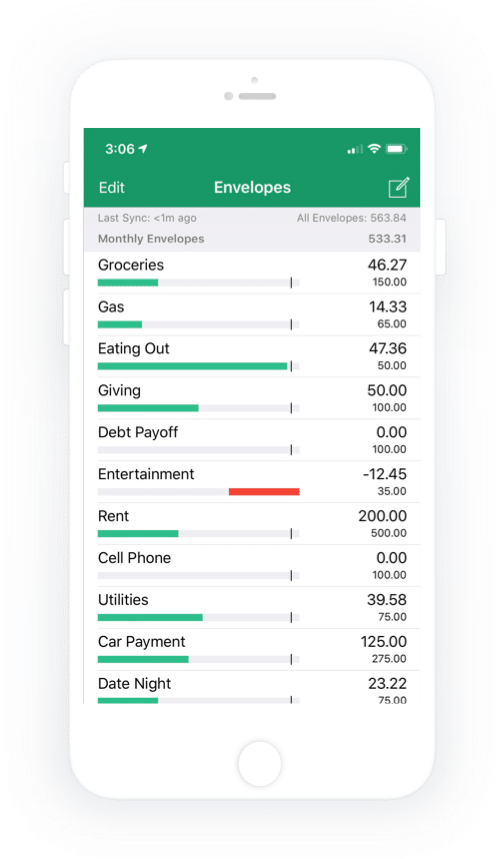

Budgeting for Success

To achieve financial stability, it's essential to start by tracking your income and expenses. This will give you a clear picture of where your money is going and help you create a personalized budget that suits your needs. By monitoring your finances, you can identify areas where you can cut back and make adjustments to achieve your financial goals.

A general rule of thumb is to allocate your income into three main categories: necessary expenses, discretionary spending, and saving and debt repayment.

- Necessary expenses, such as rent, utilities, and groceries, should account for about 50% of your income.

- Discretionary spending, including entertainment and hobbies, should make up around 30% of your income.

- Saving and debt repayment, such as paying off loans or building an emergency fund, should account for approximately 20% of your income.

This 50-30-20 rule can serve as a guideline to help you prioritize your spending and make conscious financial decisions.

To make budgeting easier and more efficient, consider using budgeting apps like Mint or You Need a Budget (YNAB). These apps allow you to track your expenses, set financial goals, and receive alerts when you go over budget. For example, Mint can help you identify areas where you can cut back on unnecessary expenses, while YNAB provides a more hands-on approach to managing your finances. By leveraging these tools, you can streamline your budgeting process and stay on top of your finances.

Creating a budget is not a one-time task, but rather an ongoing process that requires regular monitoring and adjustments. As your income and expenses change, you may need to revisit your budget and make adjustments to ensure you're still on track to meet your financial goals. By staying committed to your budget and making adjustments as needed, you can set yourself up for long-term financial success.

Managing Debt and Credit

When it comes to managing debt, it's essential to understand the different types of debt you may have. Credit card debt, student loans, and personal loans are common types of debt that can quickly add up if not managed properly. For instance, credit card debt can be particularly problematic due to high interest rates, making it crucial to tackle these debts first.

To create a debt repayment plan, start by listing all your debts, including the balance, interest rate, and minimum payment for each. This will help you prioritize your debts and focus on the most critical ones first. You can use a spreadsheet or a debt repayment app to make this process easier and more manageable.

Focusing on high-interest debts first is a good strategy, as it can save you a significant amount of money in interest payments over time. For example, if you have a credit card with a balance of $2,000 and an interest rate of 18%, you'll want to pay off this debt as quickly as possible. Here are some tips to consider:

- Prioritize debts with the highest interest rates

- Consider consolidating debts into a single, lower-interest loan

- Make extra payments whenever possible to pay off debts faster

Building credit is also an important aspect of managing debt and credit. By making timely payments and keeping credit utilization low, you can establish a positive credit history and improve your credit score. For example, if you have a credit card with a limit of $1,000, try to keep your balance below $300 to maintain a credit utilization ratio of 30% or less.

In addition to making timely payments, it's also essential to monitor your credit report regularly to ensure there are no errors or inaccuracies. You can request a free credit report from each of the three major credit bureaus once a year, which can help you stay on top of your credit and make informed decisions about your debt and credit. By following these tips and staying committed to your debt repayment plan, you can manage your debt and credit effectively and achieve financial stability.

Achieving Long-Term Financial Health

To start building a secure financial future, it's essential to set realistic, achievable long-term financial goals. These goals can include significant milestones like buying a house, retiring early, or paying off student loans. By having clear objectives in mind, you can create a roadmap for your financial journey and make progress towards a more stable future.

Setting long-term financial goals requires careful consideration of your current financial situation, income, and expenses. It's also important to make sure your goals are specific, measurable, and attainable. For example, instead of simply saying "I want to be rich," you could set a goal to save $10,000 in the next two years or pay off your credit card debt within the next 12 months.

Developing a strategy for overcoming financial setbacks is also crucial for achieving long-term financial health. This can include building an emergency fund to cover unexpected expenses, such as job loss or medical emergencies. Here are some ways to prepare for financial setbacks:

- Save 3-6 months' worth of living expenses in an easily accessible savings account

- Invest in disability insurance to protect your income in case of illness or injury

- Build a support network of friends and family who can provide financial assistance if needed

Regularly reviewing and adjusting your financial plans is vital to ensure you're making progress towards your goals. This can involve tracking your expenses, monitoring your credit score, and adjusting your budget as needed. By staying on top of your finances and making adjustments as needed, you can stay on track and achieve long-term financial health. For instance, you can use budgeting apps or spreadsheets to track your expenses and identify areas where you can cut back and save more.

Frequently Asked Questions (FAQ)

What is the best side hustle for beginners?

When it comes to finding a side hustle, beginners often feel overwhelmed by the numerous options available. The key to success lies in identifying opportunities that utilize existing skills and have a low barrier to entry. This approach allows individuals to hit the ground running and start earning money quickly.

Freelancing is an excellent example of a beginner-friendly side hustle, as it enables individuals to offer services such as writing, graphic design, or social media management to clients. Websites like Upwork and Fiverr provide a platform for freelancers to showcase their skills and connect with potential clients. By leveraging existing skills, freelancers can start working on projects immediately.

Online surveys are another viable option for those new to side hustles, as they require minimal skill and can be completed in a short amount of time.

- Swagbucks and Survey Junkie are popular platforms that offer paid surveys and other opportunities to earn money

- Users can redeem points for gift cards or cash, making it a simple way to earn some extra money

- While the pay may not be high, online surveys are a great way to get started with side hustles and can be done in spare time

These platforms are easy to use and provide a flexible way to earn money, making them perfect for beginners.

In addition to freelancing and online surveys, there are many other side hustles that beginners can explore, such as selling products online or delivering food. The most important thing is to find an opportunity that aligns with existing skills and interests, and to be willing to learn and adapt as you go. By starting small and being consistent, beginners can build a successful side hustle and achieve their financial goals.

How do I start investing with SIPs?

When it comes to investing with SIPs, the first step is to research and choose a reputable investment platform. This could be a mutual fund company, a brokerage firm, or a financial institution that offers SIP services. By selecting a reliable platform, you can ensure that your investments are secure and well-managed.

To get started, you'll need to select a suitable investment option that aligns with your financial goals and risk tolerance. This could be a equity fund, debt fund, or a hybrid fund, depending on your investment objectives. It's essential to evaluate the performance, fees, and other key features of the investment option before making a decision.

Here are some key factors to consider when selecting an investment option:

- Investment objectives: What are your short-term and long-term financial goals?

- Risk tolerance: How much risk are you willing to take on?

- Time horizon: When do you need the money?

- Investment amount: How much can you afford to invest each month?

Once you've chosen your investment option, you'll need to set up a systematic transfer plan from your bank account. This involves linking your bank account to the investment platform and setting up a monthly transfer of funds. For example, you can set up an auto-debit instruction with your bank to transfer a fixed amount, say Rs. 1,000, from your account to the investment platform on a specific date each month.

By following these steps, you can start investing with SIPs and make steady progress towards your financial goals. It's essential to review and adjust your investment portfolio periodically to ensure that it remains aligned with your changing financial needs and goals. With a well-planned SIP investment strategy, you can potentially earn higher returns over the long term and achieve financial stability.

What are some common budgeting mistakes to avoid?

Creating a budget is a great step towards taking control of your finances, but it's just the beginning. To make the most of your budget, it's essential to avoid common mistakes that can derail your financial progress. One of the most significant errors is not tracking expenses, which can lead to overspending and a lack of awareness about where your money is going.

Failing to prioritize needs over wants is another common budgeting mistake. It's easy to get caught up in discretionary spending, but it's crucial to distinguish between essential expenses, such as rent and utilities, and discretionary expenses, like dining out or entertainment. By prioritizing needs over wants, you can ensure that you're allocating your resources effectively.

Some other budgeting mistakes to avoid include:

- not regularly reviewing and adjusting your budget to reflect changes in income or expenses

- not accounting for irregular expenses, such as car maintenance or property taxes

- not building an emergency fund to cover unexpected expenses

By being aware of these potential pitfalls, you can take steps to avoid them and create a budget that truly works for you. For example, you can set aside time each month to review your budget and make adjustments as needed, or you can use the 50/30/20 rule to allocate your income towards essential expenses, discretionary spending, and savings.

Regularly reviewing and adjusting your budget can help you stay on track and achieve your financial goals. This might involve adjusting your spending habits, finding ways to reduce expenses, or exploring new sources of income. By taking a proactive and flexible approach to budgeting, you can overcome common mistakes and make progress towards financial stability and success.