As a new college graduate, managing your finances effectively can seem like a daunting task. However, with the right guidance, you can set yourself up for long-term financial success. By learning essential financial tips, you can make informed decisions about your money and avoid common pitfalls that can hinder your financial growth.

One of the most important things to consider is creating a budget that works for you. This involves tracking your income and expenses, identifying areas where you can cut back, and making conscious decisions about how you want to allocate your resources. For example, you can start by categorizing your expenses into needs and wants, and then prioritize your spending accordingly.

To get started, consider the following key areas to focus on:

- Building an emergency fund to cover unexpected expenses

- Paying off high-interest debt, such as credit card balances

- Investing in a retirement account, like a 401(k) or IRA

By addressing these areas, you can lay the foundation for a healthy financial future and make progress towards your long-term goals.

As you navigate the world of personal finance, it's essential to stay informed and adapt to changing circumstances. This may involve learning about different investment options, understanding credit scores, and staying up-to-date on tax laws and regulations. By taking a proactive approach to your finances, you can avoid costly mistakes and make the most of your hard-earned money.

Budgeting 101 for New Grads

As a new grad, managing your finances effectively is crucial to setting yourself up for long-term success. To get started, create a budget that accounts for all income sources, including your entry-level salary, part-time jobs, and freelance work. This will give you a clear picture of your overall financial situation and help you make informed decisions about how to allocate your money.

When it comes to expenses, it's essential to categorize them into needs and wants to prioritize your spending. Needs include essential expenses like rent, utilities, and food, while wants include discretionary spending like entertainment and hobbies. By distinguishing between these two categories, you can ensure that you're meeting your basic needs before spending on non-essential items.

To allocate your income effectively, consider using the 50/30/20 rule as a guideline. This means that:

- 50% of your income goes towards necessities like rent, utilities, and food

- 30% towards discretionary spending like entertainment, hobbies, and travel

- 20% towards saving and debt repayment, such as paying off student loans or building an emergency fund

For example, if you earn $4,000 per month, you would allocate $2,000 towards necessities, $1,200 towards discretionary spending, and $800 towards saving and debt repayment.

By following the 50/30/20 rule and prioritizing your spending, you can create a budget that works for you and sets you up for long-term financial stability. Remember to review and adjust your budget regularly to ensure that it continues to align with your changing needs and financial goals. With a solid budget in place, you'll be well on your way to achieving financial freedom and making the most of your post-grad life.

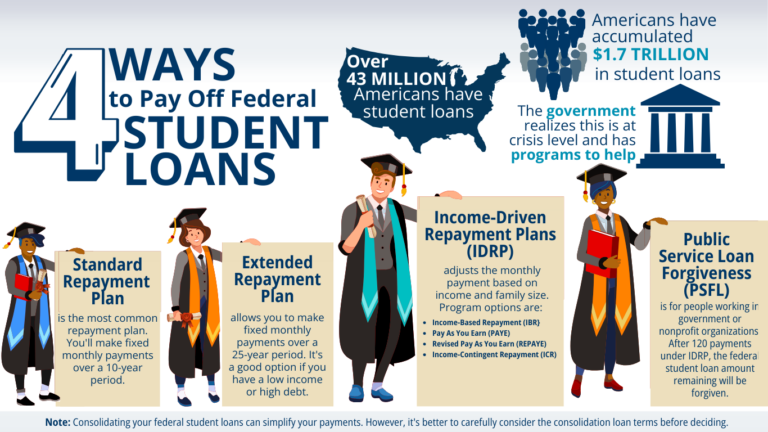

Managing Student Loan Debt

When it comes to managing student loan debt, it's essential to understand the different types of student loans available. Federal loans, such as Stafford and Perkins loans, typically have lower interest rates and more flexible repayment terms compared to private loans. For instance, federal loans may offer income-driven repayment plans, which can help reduce monthly payments.

To get a better grasp of your loan situation, consider making a list of your loans, including their interest rates and repayment terms. This can be done by:

- checking your loan documents or statements

- logging into your loan servicer's website

- contacting your loan servicer directly

Having this information readily available will help you make informed decisions about your loans.

Income-driven repayment plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), can be a great option for reducing monthly payments. These plans cap your monthly payments at a certain percentage of your income, making it more manageable to pay off your loans. Additionally, some loans may be eligible for loan forgiveness programs, which can forgive a portion of your loan balance after a certain number of payments.

Making timely payments is crucial to avoiding late fees and negative credit reporting. To stay on track, consider setting up automatic payments or reminders to ensure you never miss a payment. If you have high-interest loans, you may also want to explore options for consolidating or refinancing them, which can help lower your interest rates and simplify your payments.

Consolidating or refinancing high-interest loans can be a great way to save money on interest and reduce your monthly payments. For example, if you have multiple private loans with high interest rates, you may be able to consolidate them into a single loan with a lower interest rate. Be sure to carefully review the terms and conditions of any consolidation or refinancing option before making a decision, as it may affect your loan's repayment terms and interest rates.

Building Multiple Income Streams

Having a single source of income can be limiting, which is why building multiple income streams is essential for financial stability and growth. Exploring side hustles that align with your skills and interests is a great place to start, as it allows you to earn extra money while doing something you enjoy. For example, if you're skilled in writing, consider freelancing or tutoring to supplement your income.

Some popular side hustles include freelancing, tutoring, or ride-sharing, which can be done on a part-time basis to generate additional income. These side hustles can be managed around your primary job, allowing you to earn extra money without compromising your main source of income. You can use platforms like Upwork or Fiverr to find freelancing work, or use social media to advertise your tutoring services.

To generate passive income, consider starting a part-time business or investing in dividend-paying stocks. This can include investing in real estate investment trusts (REITs) or peer-to-peer lending, which can provide a steady stream of income with minimal effort. You can also start a small online business, such as selling products on Etsy or eBay, to generate passive income.

When building multiple income streams, it's essential to have a plan in place to allocate your extra income. Here are some ways to use your extra income:

- Save for emergencies, such as a car repair or medical bill

- Pay off high-interest debt, such as credit card debt or student loans

- Invest in long-term investments, such as a retirement account or a down payment on a house

By allocating your extra income wisely, you can achieve financial stability and build wealth over time. Remember to review and adjust your plan regularly to ensure you're on track to meet your financial goals.

Developing a plan to manage your multiple income streams is crucial to achieving financial success. This includes tracking your income and expenses, setting financial goals, and adjusting your plan as needed. By following these steps and staying committed to your goals, you can build a secure financial future and achieve financial freedom.

Investing for the Future

When it comes to investing for the future, one of the most important steps you can take is to utilize employer-matched retirement accounts. This can include options like a 401(k) or Roth IRA, which allow you to contribute a portion of your income to a retirement fund while also receiving matching funds from your employer. For example, if your employer offers a 401(k) matching program, they may match 50% of your contributions up to a certain percentage of your salary.

To make the most of your investments, it's essential to research low-cost index funds or ETFs, which can provide long-term growth with minimal fees. These types of investments can be a great option for beginners, as they offer diversification and often have lower fees compared to actively managed funds. By investing in a mix of index funds or ETFs, you can spread out your risk and increase potential returns over time.

Setting clear financial goals is also crucial when it comes to investing for the future. Some common goals include saving for a down payment on a house, retirement, or a big purchase. To achieve these goals, consider creating a plan that includes:

- Assessing your current financial situation and identifying areas for improvement

- Breaking down large goals into smaller, manageable steps

- Automating your investments and savings to make consistent progress

By taking a proactive and informed approach to investing, you can set yourself up for long-term financial success.

Consulting a financial advisor can also be a great way to get personalized guidance and create a tailored investment plan. They can help you navigate the world of investing, identify potential risks and opportunities, and make informed decisions about your financial future. Whether you're just starting out or looking to optimize your existing investments, a financial advisor can provide valuable insights and help you stay on track to achieve your goals.

Maintaining Financial Health

To maintain good financial health, it's essential to keep a close eye on your credit scores and reports. Regular monitoring can help you detect any errors or inaccuracies, which can negatively impact your credit score and overall financial well-being. For example, you can check your credit report for free once a year from each of the three major credit reporting agencies.

Monitoring your credit report regularly can also help you identify potential identity theft, allowing you to take swift action to protect your finances. This can include reporting any suspicious activity to the credit reporting agency and placing a fraud alert on your credit report. By being proactive, you can prevent further damage to your credit score and financial reputation.

Building an emergency fund is another crucial aspect of maintaining financial health. This fund should cover 3-6 months of living expenses, providing a safety net in case of unexpected events such as job loss or medical emergencies. Having a cushion of savings can help reduce financial stress and prevent you from going into debt when unexpected expenses arise.

Some practical tips for building an emergency fund include setting aside a fixed amount each month, automating your savings, and avoiding the temptation to dip into your fund for non-essential expenses. You can also consider the following strategies:

- Start small and gradually increase your savings over time

- Take advantage of high-yield savings accounts to earn interest on your emergency fund

- Review and adjust your emergency fund regularly to ensure it remains adequate

Staying informed about personal finance is also vital for maintaining financial health. This includes continuing to learn about money management strategies, such as budgeting, investing, and debt management. By expanding your knowledge and skills, you can make informed decisions about your finances and achieve your long-term goals. Whether through online resources, financial books, or workshops, there are many ways to stay up-to-date with the latest personal finance trends and strategies.

Frequently Asked Questions (FAQ)

How do I prioritize paying off high-interest debt versus building an emergency fund?

When it comes to managing your finances, two of the most important goals are paying off high-interest debt and building an emergency fund. Paying off high-interest debt first is crucial because it can save you a significant amount of money in interest payments over time. For instance, if you have a credit card with an interest rate of 20%, paying off the balance as soon as possible can help you avoid accumulating more debt.

To prioritize paying off high-interest debt, start by making a list of all your debts, including the balance, interest rate, and minimum payment for each. Use the debt avalanche method, which involves paying off debts with the highest interest rates first, while still making the minimum payments on other debts. This approach can help you save money on interest and pay off your debts more efficiently.

While paying off high-interest debt is a priority, it's also essential to allocate a small amount towards building an emergency fund. This fund will help you cover unexpected expenses, such as car repairs or medical bills, without going further into debt. Aim to save $1,000 to start, and then work your way up to three to six months' worth of living expenses.

Here are some tips to help you balance paying off high-interest debt and building an emergency fund:

- Set a budget that accounts for both debt repayment and emergency fund savings

- Automate your payments to ensure you're making progress on both goals

- Consider using a savings app or spreadsheet to track your progress

- Review and adjust your budget regularly to make sure you're on track to meet your goals

By following these steps, you can make progress on paying off high-interest debt while also building a safety net to protect yourself from financial shocks. Remember, it's all about finding a balance and making progress towards your financial goals, even if it's just a small step at a time. With patience and discipline, you can achieve financial stability and secure a brighter financial future.

What are some common budgeting mistakes new graduates should avoid?

As a new graduate, managing your finances effectively is crucial for achieving financial stability. One of the biggest hurdles is creating a budget that accurately accounts for all expenses, including small, recurring costs that can add up quickly. For instance, expenses like subscription services, such as streaming platforms or gym memberships, can be easy to overlook.

To avoid common budgeting mistakes, it's essential to prioritize needs over wants, distinguishing between essential expenses like rent, utilities, and groceries, and discretionary spending like dining out or entertainment. By doing so, you can allocate your income more effectively and make conscious financial decisions. This mindset will help you stay on track and achieve your long-term financial goals.

Some common budgeting mistakes to watch out for include:

- not accounting for irregular expenses, like car maintenance or property taxes

- failing to prioritize needs over wants, leading to overspending on non-essential items

- not regularly reviewing and adjusting the budget to reflect changes in income or expenses

Regularly reviewing your budget can help you identify areas for improvement and make adjustments as needed, ensuring you're on track to meet your financial objectives.

By being aware of these common pitfalls, new graduates can take proactive steps to manage their finances effectively and set themselves up for long-term financial success. This includes tracking expenses, creating a budget that works for them, and making adjustments as their financial situation evolves. With time and practice, budgeting becomes second nature, allowing you to make the most of your hard-earned money.

How can I get started with investing if I have little to no experience?

Getting started with investing can seem daunting, especially if you have little to no experience. A good first step is to research low-cost index funds or ETFs, which offer a diversified portfolio and often have lower fees compared to actively managed funds. This can help you spread your risk and potentially earn higher returns over the long term.

When choosing an investment, consider your financial goals and risk tolerance, and look for funds with a track record of consistent performance. You can also consult online resources, such as Morningstar or Investopedia, to learn more about different types of investments and their potential benefits. Additionally, you can use online brokerages like Vanguard or Fidelity to buy and sell investments.

If you're still unsure about where to start, consider consulting a financial advisor who can provide personalized guidance and help you create a customized investment plan. Some key benefits of working with a financial advisor include:

- Expert knowledge and guidance

- Customized investment plans tailored to your goals and risk tolerance

- Ongoing support and portfolio management

They can also help you take advantage of tax-advantaged accounts, such as 401(k) or IRA, to maximize your returns.

Another way to get started with investing is to take advantage of employer-matched retirement accounts, such as a 401(k) or 403(b). These accounts offer a matching contribution from your employer, which can help your investments grow faster over time. For example, if your employer matches 50% of your contributions up to 6% of your salary, contributing 6% of your income can result in an additional 3% from your employer, essentially giving you a 50% return on your investment. By starting early and being consistent, you can make the most of these accounts and set yourself up for long-term financial success.