As a graduate, managing student loan repayment can be overwhelming, especially when considering external factors like inflation. Inflation can significantly impact your repayment plan, making it essential to understand its effects and develop strategies to mitigate them. For instance, if you have a variable interest rate loan, inflation can cause your interest rate to rise, increasing your monthly payments.

Inflation can erode the purchasing power of your money, making it more challenging to repay your loans. This means that even if you're paying the same amount each month, the value of your payments decreases over time, potentially prolonging your repayment period. To combat this, it's crucial to create a tailored plan that takes into account the potential impact of inflation on your loans.

There are several ways to minimize the effects of inflation on your student loan repayment, including:

- Refinancing your loans to a fixed interest rate

- Increasing your monthly payments to pay off the principal balance faster

- Exploring income-driven repayment plans that can help lower your monthly payments

By understanding how inflation affects your loans and implementing these strategies, you can better manage your debt and make progress towards becoming debt-free.

It's also important to regularly review and adjust your budget to ensure you're allocating enough funds towards your loans, considering the rising costs of living due to inflation. This might involve making lifestyle adjustments, such as reducing discretionary spending or finding ways to increase your income. By taking a proactive approach, you can stay on top of your finances and achieve your long-term goals.

Understanding Inflation's Impact on Student Loans

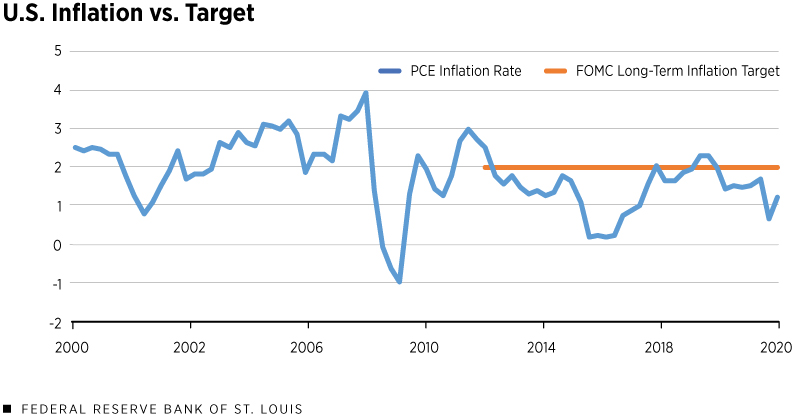

As a student loan borrower, it's essential to understand how inflation can impact your debt. Inflation reduces the purchasing power of money, meaning that the same amount of money can buy fewer goods and services over time. This can make fixed loan payments more valuable to lenders, as the amount you pay each month can effectively increase in value.

Inflation can also lead to higher interest rates, which can significantly increase the total cost of borrowing for variable-rate loans. When inflation rises, lenders often raise interest rates to keep pace with the decreasing value of money. This can result in higher monthly payments and a larger total amount paid over the life of the loan.

Some key ways inflation can affect student loan borrowers include:

- Reduced purchasing power of fixed payments

- Higher interest rates for variable-rate loans

- Increased total cost of borrowing over time

For example, if you have a variable-rate loan with an initial interest rate of 4%, an increase in inflation could cause the interest rate to rise to 6%, resulting in higher monthly payments and a larger total amount paid.

Historically, inflation has had a significant impact on student loan borrowers. In the 1980s, inflation soared, and interest rates on student loans rose accordingly, leaving many borrowers with high-interest debt. More recently, low inflation rates have kept interest rates relatively low, but borrowers should still be aware of the potential for inflation to rise and impact their loans.

To mitigate the effects of inflation on your student loans, consider making extra payments or refinancing to a fixed-rate loan. You can also keep an eye on inflation rates and interest rate trends to anticipate potential changes to your loan payments. By understanding how inflation works and taking proactive steps, you can make informed decisions about your student loan debt and reduce the impact of inflation on your finances.

Strategies to Combat Inflation's Effects on Loan Repayment

When it comes to loan repayment, inflation can be a significant obstacle. As prices rise, the purchasing power of your money decreases, making it more challenging to pay off debts. To combat this, it's essential to create a budget that accounts for inflation, allocating a portion of your income towards loan repayment.

A crucial step in managing loan repayment during inflation is to review your budget and prioritize your debts. Consider allocating a fixed percentage of your income, such as 10% to 15%, towards loan repayment. This will help you stay on track and ensure that you're making progress on paying off your loans, even as inflation rises.

Refinancing or consolidating loans to a fixed interest rate can also be beneficial in managing loan repayment during inflation. This can help you avoid rising interest rates and make your monthly payments more predictable. For example, if you have multiple loans with variable interest rates, you may be able to consolidate them into a single loan with a fixed interest rate, simplifying your payments and reducing your overall interest costs.

Some benefits of refinancing or consolidating loans include:

- Lower monthly payments

- Fixed interest rates, which can provide more stability and predictability

- Simplified payment processes, as you'll only need to make one payment per month

It's essential to explore your options and determine if refinancing or consolidating loans is the right choice for your financial situation.

Income-driven repayment plans can also be a helpful strategy for managing loan repayment during inflation. These plans can help lower your monthly payments by tying them to your income and family size. For instance, if you're experiencing financial difficulties due to inflation, an income-driven repayment plan may be able to reduce your monthly payments, making it easier to stay on top of your debts.

To take advantage of income-driven repayment plans, consider the following:

- Research and explore different plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE)

- Understand the eligibility requirements and application process for each plan

- Review and adjust your budget to ensure you're making the most of your income-driven repayment plan

By exploring these strategies and creating a budget that accounts for inflation, you can better manage your loan repayment and stay on track, even in uncertain economic times.

Building a Safety Net Against Inflation

When it comes to protecting your finances from the impact of inflation, having a solid safety net in place is crucial. This starts with building an emergency fund that covers 3-6 months of living expenses, including loan payments, to ensure you can stay afloat during uncertain times. By doing so, you'll be able to weather any financial storms that come your way, without going into debt.

To get started, consider setting aside a portion of your income each month in a easily accessible savings account. This fund will serve as a cushion, allowing you to continue paying your bills and loan payments even if you experience a loss of income. For example, if you earn $4,000 per month, aim to save $12,000 to $24,000 in your emergency fund.

In addition to building an emergency fund, it's also important to invest in assets that historically perform well during periods of inflation. Some examples include:

- Precious metals, such as gold or silver, which tend to increase in value when the cost of living rises

- Real estate, which can provide a hedge against inflation and generate rental income

- Commodities, such as oil or gas, which are often in high demand during periods of economic growth

These investments can help you grow your wealth over time, even as inflation erodes the purchasing power of your money.

Maintaining a good credit score is also essential for building a safety net against inflation. With a good credit score, you'll qualify for better loan terms, including lower interest rates and more favorable repayment terms. This can help you save money on loan payments and free up more cash in your budget to invest in assets that will appreciate in value over time. By monitoring your credit report and making on-time payments, you can ensure you're in a strong financial position to weather any economic storms that come your way.

Staying Ahead of Inflation with Smart Financial Moves

As a graduate, it's essential to stay on top of your finances, especially when it comes to inflation. One way to do this is by taking advantage of tax-advantaged savings options, such as 529 plans or Roth IRAs, which can help your money grow faster over time. For example, contributing to a Roth IRA can provide tax-free growth and withdrawals in retirement, making it an excellent option for long-term savings.

To increase your income and pay off loans faster, consider exploring side hustles or freelance work. This can be as simple as dog walking, tutoring, or freelancing in a field you're passionate about. By dedicating just a few hours a week to a side hustle, you can earn extra money to put towards your loans or savings.

When it comes to debt repayment, there are several strategies to consider. Two popular methods include the snowball method and the avalanche method. The key is to find a approach that works for you and stick to it. Here are some benefits of each method:

- The snowball method involves paying off debts with the smallest balances first, which can provide a sense of accomplishment and motivation as you quickly eliminate smaller debts.

- The avalanche method involves paying off debts with the highest interest rates first, which can save you the most money in interest over time.

In addition to debt repayment strategies, it's crucial to prioritize needs over wants and make smart financial decisions. This can involve creating a budget, tracking expenses, and avoiding lifestyle inflation. By being mindful of your spending habits and making conscious financial choices, you can stay ahead of inflation and achieve your long-term goals.

To get started, take a close look at your budget and identify areas where you can cut back on unnecessary expenses. Consider using the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment. By following this rule and staying committed to your financial goals, you can build a stable financial foundation and thrive in the face of inflation.

Conclusion and Next Steps

As you've learned, understanding inflation's impact on student loans is crucial for managing your debt effectively. Inflation can erode the purchasing power of your money, making it more challenging to repay your loans over time. For instance, if you have a fixed interest rate loan, inflation can reduce the relative value of your monthly payments.

To mitigate the effects of inflation, it's essential to review your loan terms and create a plan. Start by checking your loan documents to see if you have a fixed or variable interest rate, as this will help you determine the best course of action. You can also use online financial planning tools to simulate different repayment scenarios and find the one that works best for you.

Here are some additional resources to help you get started:

- Financial planning tools, such as Mint or You Need a Budget, can help you track your expenses and create a budget that accounts for inflation

- Counseling services, like the National Foundation for Credit Counseling, can provide personalized advice on managing your debt and creating a plan to mitigate the effects of inflation

- Online forums and communities, such as Reddit's r/studentloans, can connect you with others who are facing similar challenges and provide valuable insights and support

By taking the time to understand inflation's impact on your student loans and creating a plan to mitigate its effects, you can save money and reduce your debt burden over time. Remember to stay informed and adapt your plan as needed to ensure you're making the most of your financial resources. With the right tools and knowledge, you can take control of your student loans and achieve financial stability.

Frequently Asked Questions (FAQ)

How does inflation affect fixed-rate student loans?

Inflation can have a significant impact on the economy, and it's essential to understand how it affects your financial obligations, including student loans. As a borrower, you may be concerned about how inflation will influence your fixed-rate student loan repayments. Generally, fixed-rate loans are less affected by interest rate changes, which can provide some stability in uncertain economic times.

When inflation rises, the purchasing power of money decreases, meaning the same amount of money can buy fewer goods and services. This can be a challenge for individuals with variable-rate loans, as rising interest rates can increase their monthly payments. However, fixed-rate loans are less exposed to interest rate fluctuations, making them a more predictable option for borrowers.

To illustrate this, consider a scenario where you have a fixed-rate student loan with an interest rate of 4%. If inflation rises, the interest rate on variable-rate loans may increase, but your fixed-rate loan will remain at 4%, providing a sense of stability. Here are some key points to keep in mind:

- Inflation can lead to higher interest rates on variable-rate loans, increasing monthly payments.

- Fixed-rate loans are less affected by interest rate changes, providing more predictable repayments.

- It's essential to review your loan terms and consider the potential impact of inflation on your repayments.

It's also important to note that while fixed-rate loans may be less affected by interest rate changes, inflation can still impact the overall cost of your loan. As the purchasing power of money decreases, the amount you repay may not go as far as it would have in the past. To mitigate this, consider making extra payments or exploring income-driven repayment plans to pay off your loan more efficiently.

Ultimately, understanding how inflation affects your fixed-rate student loan can help you make informed decisions about your finances. By considering the potential impact of inflation and exploring strategies to manage your debt, you can take control of your financial obligations and achieve long-term stability.

Can I refinance my student loans to a lower interest rate during inflation?

Refinancing your student loans to a lower interest rate can be a great way to save money, especially during times of inflation. When inflation rises, interest rates often follow, making it more expensive to borrow money. As a result, refinancing your student loans to a lower interest rate can help you avoid higher payments.

To refinance your student loans, you'll typically need to meet certain requirements, such as having a good credit score and a stable income. Your credit score plays a significant role in determining the interest rate you'll qualify for, so it's essential to check your credit report and work on improving your score if necessary. A good credit score can help you qualify for lower interest rates, which can save you thousands of dollars in interest over the life of your loan.

Here are some factors to consider when refinancing your student loans:

- Your current interest rate and loan terms

- Your credit score and history

- The interest rates and terms offered by refinancing lenders

- Any potential fees associated with refinancing

It's crucial to carefully review these factors to determine if refinancing is right for you. You can start by researching and comparing rates from different lenders to find the best option for your situation.

Refinancing your student loans can be a bit complex, but it can also be a great way to save money and simplify your finances. For example, let's say you have a $30,000 student loan with an interest rate of 6% and you refinance it to a 4% interest rate. Over the life of the loan, you could save thousands of dollars in interest, which can be a huge relief during times of inflation. By understanding your options and doing your research, you can make an informed decision about refinancing your student loans and taking control of your financial future.

What are some ways to protect my investments from inflation?

As a savvy investor, it's essential to consider the impact of inflation on your portfolio. Investing in assets that historically perform well during inflation, such as precious metals or real estate, can help protect your investments. For instance, gold and silver have traditionally been viewed as safe-haven assets during times of economic uncertainty.

One approach to shielding your investments from inflation is to diversify your portfolio with a mix of asset classes. This can include investing in real estate investment trusts (REITs) or real estate mutual funds, which can provide a hedge against inflation. By spreading your investments across different asset classes, you can reduce your exposure to any one particular market or economy.

Some of the best assets to invest in during inflationary periods include:

- Precious metals, such as gold, silver, and platinum

- Real estate, including rental properties or real estate investment trusts (REITs)

- Commodities, such as oil, natural gas, or agricultural products

- TIPS (Treasury Inflation-Protected Securities), which are government bonds that adjust for inflation

These assets have historically performed well during periods of inflation, making them attractive options for investors seeking to protect their portfolios.

In addition to investing in these assets, it's also essential to monitor your portfolio regularly and make adjustments as needed. This can include rebalancing your portfolio to ensure that your investments remain aligned with your long-term goals and risk tolerance. By taking a proactive approach to managing your investments, you can help protect your portfolio from the negative effects of inflation.

It's also worth considering the role of inflation-indexed investments, such as TIPS or inflation-indexed annuities, which can provide a guaranteed return that keeps pace with inflation. These investments can be an attractive option for investors seeking to protect their purchasing power over the long term. By incorporating these investments into your portfolio, you can help ensure that your investments keep pace with inflation and maintain their purchasing power.