As a young adult considering an MBA, navigating the world of business school loans can be overwhelming. With so many options available, it's essential to find the right loan that fits your financial situation and goals. In this article, we'll explore the best MBA loans for business school in 2025, helping you make informed decisions about your financial future.

Pursuing an MBA can be a significant investment, with costs ranging from $50,000 to over $100,000 per year. To cover these expenses, many students rely on loans to help fund their education. Whether you're attending a top-tier university or a smaller program, finding the right loan is crucial to avoiding debt burdens and achieving long-term financial stability.

When searching for the best MBA loans, there are several factors to consider, including:

- Interest rates and repayment terms

- Loan amounts and eligibility requirements

- Fees and charges associated with the loan

By understanding these key factors, you can compare different loan options and choose the one that best suits your needs. In the following sections, we'll delve into the world of MBA loans, providing practical tips and examples to help you make the most informed decision possible.

Understanding MBA Loan Options

Pursuing an MBA can be a significant investment, and many students rely on loans to fund their education. To make informed decisions, it's essential to understand the different types of MBA loans available. Federal loans, such as the Federal Stafford Loan and the Federal Grad PLUS Loan, offer fixed interest rates and flexible repayment terms.

Private loans, on the other hand, are offered by banks, credit unions, and online lenders, and may have variable interest rates and stricter repayment terms. When considering private loans, it's crucial to weigh the pros and cons, including interest rates, fees, and repayment terms. For example, some private lenders may offer more competitive interest rates, but may also have less flexible repayment options.

Some popular MBA loan providers include:

- SoFi, which offers variable interest rates and no origination fees

- CommonBond, which provides fixed interest rates and a range of repayment terms

- Discover, which offers variable interest rates and no fees

These lenders often cater specifically to graduate students, offering loan options tailored to their needs. It's essential to research and compares the terms and conditions of each lender to find the best fit for your financial situation.

When evaluating loan options, consider factors such as interest rates, repayment terms, and fees. For instance, a loan with a lower interest rate may be more attractive, but if it comes with stringent repayment terms, it may not be the best choice. Additionally, some lenders may offer benefits such as unemployment protection or career support, which can be valuable resources for MBA students.

Ultimately, choosing the right MBA loan requires careful consideration of your financial goals and circumstances. By understanding the different types of loans available and weighing the pros and cons of each, you can make an informed decision and set yourself up for success. It's also important to remember that borrowing should be done responsibly, and it's essential to only borrow what you need to fund your education.

How to Choose the Best MBA Loan

When it comes to funding your MBA, choosing the right loan can be a daunting task. Considering interest rates and fees is crucial, as they can significantly impact the overall cost of your loan. For instance, a loan with a 6% interest rate may seem attractive, but if it comes with an origination fee of 2%, you'll need to factor that into your decision.

To evaluate loan repayment terms, you'll want to consider deferment and forbearance options. Deferment allows you to temporarily suspend payments, while forbearance reduces or postpones payments. Understanding these options can help you plan for unexpected financial setbacks, such as a job loss or medical emergency.

Here are some key factors to consider when evaluating loan repayment terms:

- Loan term length: How long you have to repay the loan

- Monthly payment amount: How much you'll need to pay each month

- Deferment and forbearance options: What temporary repayment relief is available

By carefully reviewing these terms, you can choose a loan that aligns with your financial situation and goals.

Comparing loan offers from multiple lenders is essential to finding the best deal. Be sure to review the fine print and ask questions about any fees or charges. You can also try negotiating with lenders to see if they can offer more favorable terms. For example, you might ask if they can waive the origination fee or offer a lower interest rate.

When negotiating with lenders, it's essential to be prepared and confident. Make a list of your questions and concerns, and don't be afraid to walk away if the terms aren't favorable. By doing your research and being proactive, you can secure an MBA loan that sets you up for financial success. Remember to also consider the lender's customer service and reputation, as these can impact your overall borrowing experience.

MBA Loan Forgiveness and Assistance Programs

Pursuing an MBA can be a costly endeavor, leaving many graduates with significant student loan debt. Fortunately, there are various loan forgiveness programs available to help alleviate this burden. One such program is the Public Service Loan Forgiveness (PSLF) program, which forgives the remaining balance on a graduate's loan after 120 qualifying payments.

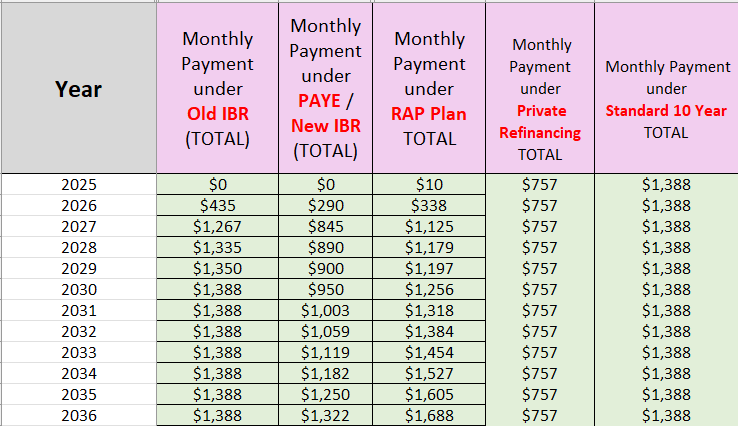

To be eligible for PSLF, MBA graduates must work full-time for a qualifying employer, such as a government agency or non-profit organization. Additionally, they must be enrolled in a qualifying repayment plan, such as an income-driven repayment plan. These plans, such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE), can help reduce monthly loan payments by capping them at a percentage of the graduate's income.

Income-driven repayment plans are a great option for MBA graduates who are struggling to make their monthly loan payments. These plans can help lower monthly payments and potentially lead to loan forgiveness after 20 or 25 years of qualifying payments. For example, if an MBA graduate has a starting salary of $60,000 and is enrolled in an IBR plan, their monthly loan payment could be significantly reduced, making it easier to manage their debt.

Some popular income-driven repayment plans include:

- Income-Based Repayment (IBR) plan, which caps monthly payments at 10% or 15% of discretionary income

- Pay As You Earn (PAYE) plan, which also caps monthly payments at 10% of discretionary income

- Revised Pay As You Earn (REPAYE) plan, which caps monthly payments at 10% or 5% of discretionary income

Loan assistance programs, such as loan deferment and forbearance, can also provide temporary relief to MBA graduates who are struggling to make their loan payments. These programs allow graduates to temporarily suspend or reduce their payments, giving them time to get back on their feet. For instance, if an MBA graduate loses their job, they may be able to defer their loan payments for a few months until they find new employment.

It's essential for MBA graduates to explore these loan forgiveness and assistance programs to determine which ones they may be eligible for. By understanding the options available, graduates can make informed decisions about their loan repayment and potentially save thousands of dollars in interest and principal payments over the life of their loan. By taking advantage of these programs, MBA graduates can better manage their debt and achieve financial stability.

Budgeting and Managing MBA Loan Debt

When it comes to managing MBA loan debt, creating a budget is essential. This involves tracking your income and expenses to understand where your money is going and making conscious decisions about how to allocate your resources. By prioritizing needs over wants, you can free up more money in your budget to tackle your loan debt.

To get started, make a list of your necessary expenses, such as rent, utilities, and groceries, and then identify areas where you can cut back on discretionary spending. For example, you could consider cooking at home instead of eating out or canceling subscription services you don't use. This will help you build a safety net and make progress on your loan debt.

Building an emergency fund is also crucial for managing loan debt. This fund will provide a cushion in case of unexpected expenses or financial setbacks, allowing you to avoid going further into debt. Aim to save 3-6 months' worth of living expenses in an easily accessible savings account.

In addition to building an emergency fund, it's also important to think about saving for retirement. Even if it seems far off, contributing to a retirement account, such as a 401(k) or IRA, can have a significant impact over time. Consider setting up automatic transfers from your paycheck to make saving easier and less prone to being neglected.

To pay off MBA loans quickly, consider the following strategies:

- Making extra payments: Paying more than the minimum payment each month can help you pay off your loans faster and reduce the amount of interest you owe.

- Using the snowball method: This involves paying off your loans with the smallest balances first, while making minimum payments on your other loans, to build momentum and see progress more quickly.

- Consolidating your loans: If you have multiple loans with high interest rates, you may be able to consolidate them into a single loan with a lower interest rate and lower monthly payments.

By implementing these strategies and staying committed to your budget, you can make progress on your loan debt and set yourself up for long-term financial success.

Alternatives to MBA Loans

When it comes to funding an MBA, many students immediately think of loans. However, there are several alternatives to consider, including scholarships and grants. These options can provide a significant source of funding without the burden of debt, making them an attractive choice for many students.

Scholarships and grants are available from a variety of sources, including universities, private organizations, and government agencies. To apply for MBA scholarships and grants, students typically need to submit an application, which may include an essay, transcripts, and letters of recommendation. By researching and applying for these opportunities, students can potentially secure thousands of dollars in funding.

To increase their chances of securing a scholarship or grant, students should focus on writing a strong application essay. This essay should clearly outline their career goals, motivation for pursuing an MBA, and any relevant experience or skills. For example, a student who has worked in a non-profit organization may want to highlight their experience and passion for social impact in their essay.

Some popular MBA scholarships and grants include:

- Forte Fellowship: a scholarship program for women pursuing an MBA

- Consortium for Graduate Study in Management: a fellowship program for underrepresented minorities

- National Black MBA Association: a scholarship program for African American students

These are just a few examples, and there are many more opportunities available to students.

In addition to traditional scholarships and grants, students may also want to consider crowdfunding as a funding option. Crowdfunding platforms, such as GoFundMe or Kickstarter, allow students to create a campaign and raise money from friends, family, and community members. This can be a great way to raise a small amount of money for specific expenses, such as textbooks or living expenses.

Other non-traditional funding options may include:

- Employer tuition reimbursement: some companies offer to reimburse employees for tuition expenses

- Personal savings: students can use their own savings to fund their education

- Income share agreements: some companies offer to fund a student's education in exchange for a percentage of their future income

By exploring these alternative funding options, students can reduce their reliance on loans and create a more sustainable financial plan for their MBA.

Frequently Asked Questions (FAQ)

What are the best MBA loans for international students?

As an international student pursuing an MBA, navigating the landscape of available loan options can be daunting. Private loan options are often a viable consideration, as they can provide the necessary funding to support your educational endeavors. For instance, lenders like Prodigy Finance or MPower Financing cater specifically to international students.

When exploring private loan options, it's essential to weigh the terms and conditions carefully. Factors such as interest rates, repayment terms, and eligibility criteria should be thoroughly evaluated. International students can also consider reaching out to their university's financial aid office for guidance on available loan options.

Some popular private loan options for international students include:

- Prodigy Finance, which offers loans with competitive interest rates and flexible repayment terms

- MPower Financing, which provides loans with no cosigner or collateral requirements

- Other lenders that specialize in international student loans, such as Discover or Sallie Mae

These lenders often have experience working with international students and can provide tailored loan solutions to meet their unique needs.

To increase your chances of securing a favorable loan, it's crucial to maintain a good credit score, research the lender thoroughly, and carefully review the loan agreement before signing. Additionally, consider applying for loans with a cosigner, if possible, as this can help reduce the interest rate and improve the overall loan terms. By doing your due diligence and exploring available options, you can find the best MBA loan for your needs as an international student.

Can I use an MBA loan to pay for living expenses?

When considering an MBA loan, it's essential to understand how you can use the funds. Many MBA loan programs allow borrowers to use loan funds to cover living expenses, such as housing and food. This can be a huge relief for students who need to support themselves while pursuing their degree.

In general, MBA loans can be used to cover a wide range of expenses, including tuition, fees, and living costs. For example, if you're attending a program in a city with a high cost of living, you may be able to use your loan funds to help pay for housing, utilities, and other necessities. This can help you focus on your studies without worrying about how you'll make ends meet.

Some common living expenses that can be covered with an MBA loan include:

- Housing, including rent or mortgage payments

- Food and other household expenses

- Transportation costs, such as car payments or public transportation fees

- Health insurance and other medical expenses

It's essential to review your loan agreement to understand what expenses are eligible for coverage. You should also make sure you're not overspending, as you'll need to repay the loan, plus interest, after you graduate.

To make the most of your MBA loan, it's a good idea to create a budget that accounts for all your expenses, including living costs. This will help you manage your finances effectively and avoid taking on too much debt. By being mindful of your spending and using your loan funds wisely, you can set yourself up for success and make the most of your MBA program.

How do I apply for MBA loan forgiveness programs?

Applying for MBA loan forgiveness programs can be a straightforward process if you have the right information and documentation. To get started, borrowers typically need to submit an application and provide proof of income and employment, which can be in the form of pay stubs or a letter from their employer. This documentation helps lenders verify that borrowers meet the program's eligibility criteria.

In addition to proof of income and employment, borrowers may also need to provide other documentation, such as tax returns or proof of enrollment in an MBA program. It's essential to review the specific requirements for each loan forgiveness program to ensure you have all the necessary documents. For example, some programs may require borrowers to have made a certain number of payments or to be working in a specific field.

To apply for MBA loan forgiveness programs, follow these steps:

- Research and review the eligibility criteria for each program to determine which ones you qualify for

- Gather all required documentation, including proof of income and employment

- Submit your application and supporting documents according to the program's instructions

By following these steps and providing the necessary documentation, borrowers can increase their chances of being approved for an MBA loan forgiveness program. It's also a good idea to keep track of your application and follow up with the lender if you have any questions or concerns.