As a young adult, managing personal finances can be overwhelming, especially with the introduction of new project finance norms. These norms can have a significant impact on how you approach budgeting, saving, and investing. For instance, changes in interest rates and borrowing costs can affect your ability to secure loans or credit cards.

New project finance norms can also influence your financial decisions, such as choosing between fixed and variable interest rates on loans. It's essential to understand how these norms work and how they can affect your financial situation. By staying informed, you can make better decisions about your money and achieve your long-term financial goals.

Some key aspects of new project finance norms that you should be aware of include:

- Changes in lending criteria and credit scoring

- Shifts in interest rates and borrowing costs

- New regulations on investment products and services

These changes can have a significant impact on your personal finance, and it's crucial to stay up-to-date with the latest developments to make informed decisions.

To navigate these changes, it's a good idea to start by reviewing your current financial situation and assessing how the new norms may affect you. You can also consider seeking advice from a financial advisor or using online resources to help you make sense of the changes. By taking a proactive approach, you can ensure that you're well-equipped to manage your finances effectively in the face of new project finance norms.

Understanding New Project Finance Norms

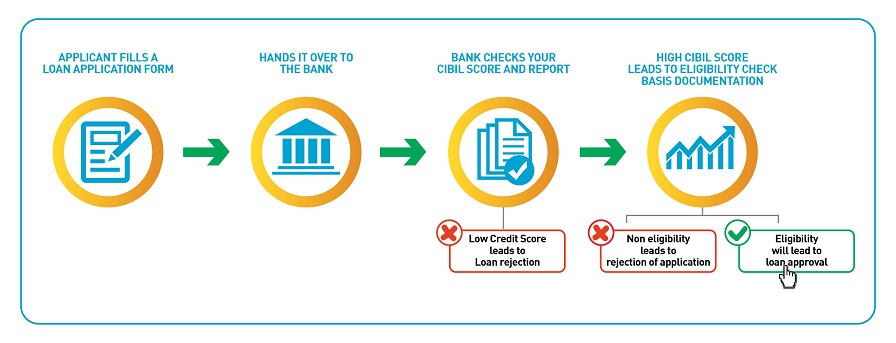

The financial landscape is constantly evolving, and recent changes in project finance norms have significant implications for borrowers. These new norms aim to enhance transparency and stability in the lending market, but they also introduce new challenges, particularly for smaller loans and individual borrowers. As a result, banks and financial institutions are seeking exemptions for smaller loans to mitigate the impact on their customers.

The exemption being sought by banks applies to loans below a certain amount, typically around $100,000, and includes types such as personal loans, credit card debt, and small business loans. This exemption would allow banks to continue offering these smaller loans without having to adhere to the stricter norms, which can be costly and time-consuming to implement. For instance, banks might be exempt from conducting thorough credit checks or providing detailed loan documentation for smaller amounts.

Some of the key loan types that might be exempt from the new norms include:

- Personal loans up to $50,000

- Credit card debt with limits below $20,000

- Small business loans totaling less than $100,000

These exemptions would enable banks to continue serving smaller borrowers and young adults who often rely on these types of loans to cover unexpected expenses or finance their education.

The new norms could significantly change the lending landscape for young adults, who may face stricter loan terms or higher interest rates if the exemptions are not granted. For example, a young adult applying for a personal loan to cover tuition fees might be subject to a more rigorous credit check or required to provide additional collateral. To navigate these changes, it's essential for young adults to understand the new norms and plan their finances accordingly, such as by building a good credit score or exploring alternative lending options.

In practice, the new norms might lead to a shift towards more conservative lending practices, with banks focusing on larger, more secure loans. However, this could also create opportunities for alternative lenders, such as peer-to-peer lending platforms or fintech companies, to fill the gap and offer more flexible loan options to smaller borrowers. By staying informed and adapting to these changes, young adults can make more informed decisions about their finances and find the best loan options for their needs.

Impact on Personal Finance for Young Adults

As young adults navigate the new financial landscape, it's essential to consider how the shifting norms could impact their borrowing costs and accessibility. For students and recent graduates, this may mean higher interest rates on student loans or credit cards, making it more challenging to manage debt. By understanding these changes, young adults can make informed decisions about their financial future.

The new norms may lead to increased borrowing costs, making it more difficult for young adults to access credit or loans. This could be particularly problematic for those who rely on smaller loans to cover unexpected expenses or finance their education. For instance, a student who needs a loan to cover tuition fees may face higher interest rates, making it more expensive to borrow.

When it comes to debt management, young adults may need to adapt their financial plans to account for the changing landscape. This could involve creating a budget that prioritizes debt repayment or exploring alternative financing options, such as income-driven repayment plans. By taking a proactive approach to debt management, young adults can minimize the impact of the new norms and achieve their long-term financial goals.

Some key considerations for young adults include:

- Shopping around for loans with competitive interest rates

- Building a solid credit history to improve credit scores

- Creating a budget that accounts for increased borrowing costs

By following these tips, young adults can navigate the changes in the financial landscape and make informed decisions about their borrowing and debt management.

To navigate the changes when applying for smaller loans, young adults should start by researching and comparing different lenders and loan options. This could involve reading reviews, checking interest rates, and evaluating repayment terms. By doing their due diligence, young adults can find the best loan options for their needs and avoid costly mistakes.

In terms of practical tips, young adults can also consider:

- Using online loan calculators to estimate borrowing costs

- Asking lenders about any fees or charges associated with the loan

- Reading the fine print to understand the terms and conditions of the loan

By taking a thoughtful and informed approach to borrowing, young adults can minimize the risks and make the most of the new financial landscape.

Strategies for Navigating the New Norms

As the financial landscape continues to evolve, young adults must be proactive in navigating the new norms. This includes preparing for potential changes in loan availability and interest rates, which can significantly impact their financial stability. By staying informed and adapting to these changes, young adults can make informed decisions about their financial futures.

To prepare for potential changes, young adults should consider reviewing their current loan agreements and understanding the terms and conditions. They should also research and explore alternative financing options, such as peer-to-peer lending or credit unions, which may offer more favorable interest rates and repayment terms. For example, a young adult with a good credit score may be able to secure a lower interest rate through a peer-to-peer lending platform.

Some alternative financing options that young adults might consider include:

- Peer-to-peer lending, which allows individuals to borrow from other individuals or groups

- Credit unions, which are member-owned cooperatives that offer more personalized and competitive financial services

- Community development financial institutions, which provide financial services to underserved communities

These options may offer more flexible repayment terms and lower interest rates, making them attractive alternatives to traditional loans.

Maintaining a good credit score is crucial in a changing loan environment, as it can significantly impact an individual's ability to secure loans and credit at favorable interest rates. Young adults can maintain a good credit score by making timely payments, keeping credit utilization low, and monitoring their credit reports for errors. By prioritizing credit score maintenance, young adults can position themselves for long-term financial success and stability.

In addition to exploring alternative financing options and maintaining a good credit score, young adults should also prioritize budgeting and saving. This includes creating a budget that accounts for potential changes in loan payments and interest rates, as well as building an emergency fund to cover unexpected expenses. By taking a proactive and informed approach to their finances, young adults can navigate the new norms with confidence and achieve their long-term financial goals.

Budgeting and Debt Management in the New Landscape

As the financial landscape continues to evolve, it's essential to have a budget that can adapt to changes in loan terms or interest rates. A flexible budget allows you to adjust your spending and savings accordingly, ensuring you stay on track with your financial goals. For instance, if your loan interest rate increases, you can allocate more funds towards debt repayment and cut back on non-essential expenses.

To create a flexible budget, start by tracking your income and expenses to understand where your money is going. Make a list of your necessary expenses, such as rent, utilities, and groceries, and prioritize them over discretionary spending. You can use the 50/30/20 rule as a guideline, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment.

When it comes to debt repayment, prioritizing your debts is crucial, especially for those with variable-rate loans. Consider the following strategies:

- Focus on paying off high-interest debts first, such as credit card balances or personal loans with high interest rates

- Consolidate multiple debts into a single loan with a lower interest rate and a longer repayment period

- Take advantage of debt snowballing, where you pay off smaller debts first to build momentum and confidence

By prioritizing your debts and creating a flexible budget, you can better manage your finances and stay on track with your debt repayment goals.

Having an emergency fund in place is also vital for financial stability during economic shifts. An emergency fund is a pool of money set aside to cover unexpected expenses, such as car repairs or medical bills. Aim to save 3-6 months' worth of living expenses in an easily accessible savings account, such as a high-yield savings account. This fund will help you avoid going further into debt when unexpected expenses arise and provide peace of mind during uncertain economic times.

In addition to emergency funds, it's essential to review and adjust your budget regularly to ensure you're on track with your financial goals. Consider scheduling regular budget reviews, such as every 3-6 months, to assess your progress and make adjustments as needed. By staying on top of your finances and being prepared for changes in the economic landscape, you can achieve financial stability and success.

Investing and Side Hustles as Alternatives

Investing in education or skill development can be a savvy strategy to boost earning potential and reduce reliance on loans. By acquiring new skills or certifications, young adults can increase their market value and qualify for higher-paying jobs. For instance, learning to code or becoming proficient in digital marketing can open up new career opportunities and increase earning potential.

Investing in oneself can take many forms, including online courses, workshops, or conferences. These investments can pay off in the long run by leading to better job prospects and higher salaries. Some popular platforms for investing in education and skill development include Coursera, Udemy, and LinkedIn Learning.

In addition to investing in education, starting a side hustle can be a great way to increase income and improve financial health. A side hustle can provide a supplementary source of income, reducing the need for smaller loans and helping young adults achieve their financial goals. Some popular side hustles for young adults include freelance writing, graphic design, and pet-sitting.

There are many resources and platforms available where young adults can find opportunities for investing in themselves or starting a side hustle. Some examples include:

- Upwork and Fiverr for freelance work

- Etsy and eBay for selling products online

- Ride-sharing and food delivery services like Uber and DoorDash

These platforms can provide a starting point for young adults looking to invest in themselves or start a side hustle and achieve financial stability.

To get started with investing in education or starting a side hustle, young adults can begin by identifying their strengths and interests. They can then research online courses or platforms that align with their goals and start taking action. With persistence and dedication, young adults can achieve their financial goals and reduce their reliance on loans.

Frequently Asked Questions (FAQ)

How will the new project finance norms affect my student loan?

As a student loan borrower, it's natural to wonder how the new project finance norms will impact your loan. The truth is, the impact depends on the specifics of your loan and the lender, so it's essential to review your loan agreement and understand the terms. This will help you prepare for potential changes in interest rates or repayment terms.

For instance, if you have a variable-rate loan, you may be more affected by the new norms than those with fixed-rate loans. It's crucial to check your loan documents to see if your lender has the flexibility to adjust interest rates or repayment terms in response to the new norms. This information will help you plan ahead and make informed decisions about your loan.

To prepare for potential changes, consider the following:

- Review your loan agreement to understand the terms and conditions

- Check with your lender to see if they plan to make any changes to interest rates or repayment terms

- Explore options for consolidating or refinancing your loan to take advantage of more favorable terms

By taking these steps, you can ensure that you're prepared for any changes that may come with the new project finance norms. It's also a good idea to stay informed about any updates or announcements from your lender or the government regarding the new norms.

In addition to reviewing your loan agreement, it's essential to continue making timely payments and communicating with your lender to avoid any potential issues. By being proactive and staying informed, you can navigate the potential impact of the new project finance norms on your student loan and make the best decisions for your financial situation. This will help you stay on track with your loan repayment and achieve your long-term financial goals.

Can I still get a small loan under the new norms?

The new norms in the lending industry have raised concerns among individuals seeking small loans. However, it is still possible to get a small loan, but the process and terms may differ from what you were used to. Banks are now more cautious and may have stricter eligibility criteria, so it's essential to review and understand the new requirements before applying.

One of the key changes is that banks are seeking exemptions that could affect loan availability and cost. This means that some lenders may not offer small loans or may charge higher interest rates to compensate for the increased risk. For instance, a bank may offer a small loan with a higher interest rate or a shorter repayment period to mitigate the risk.

To increase your chances of getting a small loan, consider the following tips:

- Check your credit score and history to ensure you have a good credit standing

- Explore alternative lenders, such as credit unions or online lenders, that may offer more flexible terms

- Compare loan offers from different lenders to find the best deal

By doing your research and understanding the new norms, you can still get a small loan that meets your needs, even if the process and terms have changed.

It's also important to note that some banks may have introduced new loan products or programs that are designed to help individuals with limited credit history or those who need small amounts of money. For example, a bank may offer a small loan with a lower interest rate for borrowers who agree to take a financial education course or set up automatic payments. Be sure to ask about these options when you apply for a loan.

What are some alternatives to traditional bank loans for young adults?

As a young adult, navigating the world of finance can be overwhelming, especially when it comes to borrowing money. Traditional bank loans may not always be the best option, and that's where alternative solutions come in. Peer-to-peer lending, for instance, allows individuals to borrow from other people, often with more flexible terms and lower interest rates.

One of the benefits of peer-to-peer lending is that it can be more accessible than traditional bank loans, with fewer requirements and a faster application process. Credit unions are another alternative, offering lower interest rates and more personalized service. These not-for-profit organizations are member-owned, which means they often have more favorable terms and conditions.

When considering alternatives to traditional bank loans, it's essential to think about the root cause of your borrowing needs. Investing in personal development can be a great way to reduce the need for loans in the first place. By acquiring new skills or certifications, you can increase your earning potential and avoid debt altogether.

Some ways to invest in personal development include:

- taking online courses or attending workshops to improve your career prospects

- reading books or articles to stay up-to-date with industry trends

- joining professional networks or associations to connect with like-minded individuals

By exploring these alternatives and investing in yourself, you can take control of your finances and make more informed decisions about borrowing and lending.