As a young entrepreneur, navigating the world of business loans can be overwhelming, especially when it comes to personal guarantees. Many traditional lenders require entrepreneurs to sign a personal guarantee, which puts their personal assets at risk in case the business defaults on the loan. However, there are alternative options available that can help young entrepreneurs explore business loan options without personal guarantees.

For instance, some online lenders offer business loans without personal guarantees, instead focusing on the business's creditworthiness and revenue. These lenders often have more lenient requirements and faster application processes, making it easier for young entrepreneurs to access the funds they need. By researching and comparing different lenders, entrepreneurs can find the best option for their business.

Some popular alternatives to traditional business loans include:

- Crowdfunding platforms, which allow entrepreneurs to raise funds from a large number of people, typically in exchange for rewards or equity

- Invoice financing, which provides businesses with immediate access to cash based on outstanding invoices

- Community development financial institutions, which offer affordable loans and technical assistance to entrepreneurs in underserved communities

These options can provide young entrepreneurs with the funding they need to grow their businesses without putting their personal assets at risk. By exploring these alternatives, entrepreneurs can make informed decisions about their business financing options and set themselves up for long-term success.

Understanding Business Loans Without Personal Guarantees

When starting a new business, young entrepreneurs often face the challenge of securing funding without putting their personal assets at risk. Business loans without personal guarantees offer a solution to this problem, allowing borrowers to access capital without pledging personal collateral. This type of loan is especially beneficial for young entrepreneurs who may not have a established credit history or personal assets to secure a loan.

One of the key benefits of business loans without personal guarantees is that they separate personal and business finances, protecting the borrower's personal assets in case the business defaults on the loan. This can be a huge relief for young entrepreneurs who are just starting out and may not have the financial resources to absorb a significant loss. For example, a startup founder can use a business loan without a personal guarantee to fund their new venture, without risking their own home or savings.

In the context of business loans without personal guarantees, it's essential to understand the difference between secured and unsecured loans. Secured loans require collateral, such as business assets or equipment, to secure the loan, while unsecured loans do not require any collateral. Unsecured loans are often more challenging to obtain and may have higher interest rates, but they can be a good option for businesses that do not have significant assets to pledge as collateral.

Some key characteristics of business loans without personal guarantees include:

- No personal collateral required

- Based on business creditworthiness, not personal credit score

- May have higher interest rates or fees

- Often require a solid business plan and financial projections

These loans can be an attractive option for young entrepreneurs who are looking to grow their business without putting their personal assets at risk.

However, there are potential risks and considerations for borrowers to be aware of, such as higher interest rates, stricter repayment terms, and the potential for business credit score damage if the loan is not repaid on time. Borrowers should carefully review the loan terms and conditions before signing any agreement, and consider seeking the advice of a financial advisor to ensure they are making an informed decision. By understanding the benefits and risks of business loans without personal guarantees, young entrepreneurs can make informed decisions about their business financing options and set themselves up for success.

Types of Business Loans Without Personal Guarantees

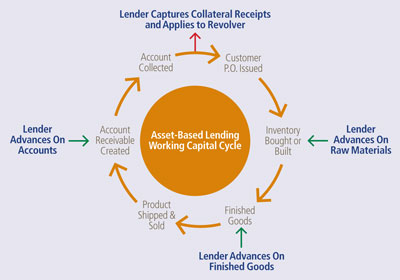

As a business owner, accessing financing without putting personal assets at risk can be a significant relief. Asset-based financing is one such option, where loans are secured by the business's assets, such as inventory, property, or accounts receivable. This type of financing often requires a thorough evaluation of the business's assets and financial performance.

Asset-based financing can be an attractive option for businesses with a strong asset base, as it allows them to leverage these assets to access capital. For example, a retail business with a large inventory of products can use asset-based financing to secure a loan, using the inventory as collateral. The requirements for asset-based financing typically include a detailed asset valuation and a solid business plan.

Another option for businesses is invoice financing, which is ideal for companies with outstanding invoices that are waiting to be paid. This type of financing allows businesses to receive an advance on their outstanding invoices, providing much-needed cash flow to support operations. Invoice financing can be particularly useful for businesses with long payment terms or slow-paying clients.

Some of the key benefits of invoice financing include:

- Improved cash flow to support business operations

- Reduced reliance on personal assets as collateral

- Increased flexibility to invest in business growth

Equipment financing is another option for businesses that need to purchase specific equipment to support their operations. This type of financing allows businesses to acquire the necessary equipment without having to pay the full cost upfront. For instance, a manufacturing business may use equipment financing to purchase new machinery, using the equipment itself as collateral.

These financing options can support business growth without risking personal assets by providing access to capital without requiring personal guarantees. By leveraging business assets, such as equipment or outstanding invoices, businesses can secure the funding they need to invest in growth and expansion. This can be a significant advantage for businesses looking to scale up their operations without putting their owners' personal assets at risk.

Qualifying for Business Loans Without Personal Guarantees

To qualify for a business loan without a personal guarantee, you typically need to meet certain requirements. Lenders often consider your business credit score and revenue, with a good credit score and steady revenue increasing your chances of approval. For example, a business with a credit score of 700 or higher and annual revenue of $250,000 or more may be more likely to qualify for a loan.

A solid business plan and financial projections are also crucial in the loan application process. This plan should outline your business goals, target market, and financial projections, demonstrating your ability to repay the loan. By showing a clear understanding of your business and its financials, you can increase confidence in your ability to repay the loan.

Improving your business credit can significantly increase your loan eligibility, and there are several ways to do this.

- Paying bills on time to establish a positive payment history

- Monitoring your credit report for errors or inaccuracies

- Keeping credit utilization low to demonstrate responsible credit management

By following these tips, you can improve your business credit score and increase your chances of qualifying for a loan.

The industry and type of business you operate can also play a role in loan approval, with some lenders being more willing to lend to certain types of businesses. For example, a lender may be more likely to approve a loan for a retail business with a stable cash flow than a startup with an unproven business model. Understanding the lender's preferences and tailoring your loan application accordingly can help you increase your chances of approval.

It's essential to research and understands the lender's requirements and preferences before applying for a business loan. By doing so, you can prepare a strong loan application and increase your chances of qualifying for a loan without a personal guarantee. This can help you protect your personal assets and separate your business and personal finances.

Alternative Funding Options for Young Entrepreneurs

As a young entrepreneur, securing funding can be a daunting task, but there are several alternative funding options available. Crowdfunding is a community-driven funding option that allows you to raise money from a large number of people, typically through online platforms. For example, platforms like Kickstarter and Indiegogo have helped numerous startups raise millions of dollars in funding.

Venture capital and angel investors are another option for young entrepreneurs with high-growth potential businesses. These investors provide funding in exchange for equity in your business and can also offer valuable guidance and mentorship. To attract venture capital and angel investors, it's essential to have a solid business plan, a clear vision, and a strong team in place.

Small business grants are a great option for young entrepreneurs who are looking for non-repayable funding. These grants are typically offered by government agencies, foundations, and non-profit organizations to support specific industries or business types. Some examples of small business grants include the Small Business Innovation Research (SBIR) grant and the Small Business Technology Transfer (STTR) grant.

When it comes to securing funding, networking and building relationships with potential investors is crucial. This can be done by attending industry events, joining business organizations, and connecting with other entrepreneurs and investors on social media. Here are some tips for building relationships with potential investors:

- Be clear and concise about your business idea and vision

- Show a strong understanding of your target market and industry

- Demonstrate a solid business plan and financial projections

- Be prepared to answer tough questions and provide updates on your business progress

By exploring these alternative funding options and building relationships with potential investors, young entrepreneurs can increase their chances of securing the funding they need to launch and grow their businesses. It's also essential to be flexible and open to different funding options, as what works for one business may not work for another. With the right funding and support, young entrepreneurs can turn their business ideas into successful and sustainable ventures.

Best Practices for Managing Business Loans

Maintaining a healthy business credit score is crucial for any organization, and one key aspect of achieving this is making timely repayments on business loans. Late payments can negatively impact your credit score, making it more difficult to secure loans in the future. For example, setting up automatic payments can help ensure that you never miss a payment.

Managing cash flow is essential to ensure that loan repayments are made on time. This involves tracking income and expenses, creating a budget, and prioritizing loan repayments. By doing so, you can avoid late payment fees and penalties, and also maintain a positive relationship with your lender.

When it comes to managing business loans, reviewing and understanding loan terms before signing is vital. This includes understanding the interest rate, repayment terms, and any fees associated with the loan. It's also important to ask questions and seek clarification if you're unsure about any aspect of the loan.

Some key strategies for managing cash flow to ensure loan repayments include:

- Creating a cash flow forecast to anticipate and prepare for any shortfalls

- Building an emergency fund to cover unexpected expenses

- Negotiating with suppliers to extend payment terms if necessary

By implementing these strategies, you can ensure that you have sufficient funds to make loan repayments and maintain a healthy cash flow.

Seeking professional advice from a financial advisor or accountant can be incredibly valuable when it comes to managing business loans. They can help you review loan terms, create a repayment plan, and provide guidance on managing cash flow. This can be especially helpful if you're new to business loan management or are unsure about how to navigate the process.

Ultimately, managing business loans requires careful planning, attention to detail, and a commitment to making timely repayments. By following these best practices and seeking professional advice when needed, you can maintain a healthy business credit score and ensure the long-term success of your organization.

Frequently Asked Questions (FAQ)

What are the typical interest rates for business loans without personal guarantees?

When exploring business loan options without personal guarantees, it's essential to understand the various interest rates that come with these loans. Interest rates vary based on the lender, loan type, and business creditworthiness, making it crucial to research and compare rates before making a decision. This will help you find the most suitable loan for your business needs.

The lender plays a significant role in determining the interest rate, with traditional banks typically offering lower rates compared to alternative lenders. However, alternative lenders may have more flexible repayment terms and fewer requirements, making them an attractive option for some businesses. For instance, online lenders may offer more competitive rates for businesses with a strong credit history.

The type of loan also impacts the interest rate, with some common options including:

- Term loans, which offer a fixed interest rate and repayment schedule

- Lines of credit, which provide a revolving credit limit with variable interest rates

- Invoice financing, which uses outstanding invoices as collateral and often has higher interest rates

Each loan type has its unique characteristics, and understanding these differences can help you choose the best option for your business.

Business creditworthiness is another critical factor in determining interest rates, as lenders view businesses with excellent credit as less risky. To improve your business credit, focus on making timely payments, reducing debt, and monitoring your credit report for errors. By taking these steps, you can demonstrate your business's creditworthiness and potentially qualify for lower interest rates.

In general, interest rates for business loans without personal guarantees can range from 5% to 30% or more, depending on the lender and loan type. To get the best rate, it's crucial to shop around, compare offers, and consider working with a loan broker or financial advisor who can guide you through the process. By doing your research and understanding the factors that influence interest rates, you can make an informed decision and find a loan that supports your business growth.

Can I get a business loan without a personal guarantee if I have bad credit?

As a business owner with bad credit, obtaining a business loan without a personal guarantee can be a daunting task. However, some lenders offer options for businesses with less-than-perfect credit, providing a glimmer of hope. These lenders often consider other factors, such as business revenue and cash flow, when making lending decisions.

When exploring loan options, it's essential to understand that lenders typically require a personal guarantee to mitigate risk. However, some alternative lenders and online loan providers offer no-personal-guarantee loans or use alternative forms of collateral. For instance, invoice financing or equipment financing may be available without a personal guarantee.

To increase your chances of getting approved for a business loan without a personal guarantee, consider the following:

- Improve your business credit score by making timely payments and reducing debt

- Provide a detailed business plan and financial projections to demonstrate stability and growth potential

- Explore lenders that specialize in bad credit business loans or no-personal-guarantee loans

These strategies can help you navigate the lending process and find options that cater to your business needs.

Some lenders also offer secured business loans, which use business assets as collateral instead of a personal guarantee. This can be a viable option for businesses with valuable assets, such as property or equipment. By using these assets as collateral, you may be able to secure a loan with more favorable terms.

It's crucial to carefully review the terms and conditions of any loan offer, including interest rates, repayment terms, and fees. Be sure to work with a reputable lender and seek professional advice if needed to ensure you're making an informed decision. By doing your research and exploring alternative options, you can increase your chances of getting a business loan without a personal guarantee, even with bad credit.

How do I apply for a business loan without a personal guarantee?

When applying for a business loan without a personal guarantee, it's essential to have a solid understanding of the process. This typically involves submitting business financials, a business plan, and other documentation to the lender. By doing so, you demonstrate your business's creditworthiness and ability to repay the loan.

To increase your chances of approval, make sure your business financials are up-to-date and accurately reflect your company's financial health. This includes balance sheets, income statements, and cash flow statements. Reviewing your financials carefully will help you identify areas for improvement and make a more compelling case to lenders.

Some lenders may also require additional documentation, such as:

- Business tax returns

- Accounts receivable and payable reports

- Inventory valuations

Having these documents ready will streamline the application process and show lenders that you're organized and prepared.

A well-crafted business plan is also crucial, as it outlines your company's goals, strategies, and financial projections. This plan should demonstrate a clear understanding of your industry, market, and competition, as well as a solid plan for repayment. By providing a comprehensive business plan, you can build trust with lenders and increase your chances of securing a loan without a personal guarantee.

Practical tips for applying for a business loan without a personal guarantee include working with a lender that specializes in business loans, maintaining a good business credit score, and being prepared to provide collateral or other forms of security. By following these tips and submitting a thorough application, you can improve your chances of approval and secure the funding your business needs to grow and succeed.