As we begin our journey to financial freedom, let's draw inspiration from a remarkable individual who achieved the unthinkable. Meet a man who retired at the young age of 45 with a staggering ₹4.7 crore, all without relying on side hustles or stock tips. His story serves as a testament to the power of disciplined investing and smart financial planning.

This individual's success can be attributed to his careful approach to money management, which involved creating a well-thought-out investment strategy and sticking to it. By doing so, he was able to build a substantial corpus over time, allowing him to retire early and live a life of financial independence. His story is a great example of how anyone can achieve their financial goals with the right mindset and approach.

Some key takeaways from his story include:

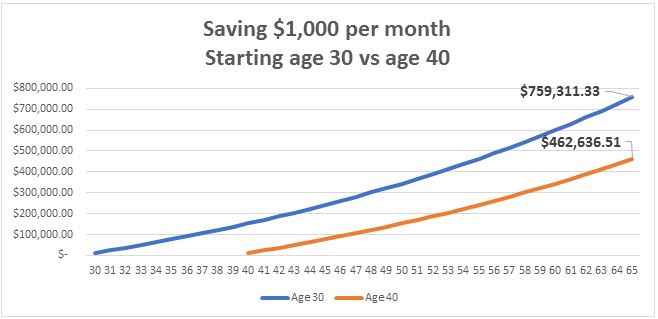

- Starting to invest early, even with a small amount, can make a significant difference in the long run

- Having a clear understanding of one's financial goals and creating a plan to achieve them is crucial

- Discipline and patience are essential when it comes to investing and achieving financial freedom

By following these principles and staying committed to his goals, this individual was able to achieve a life of financial freedom, and his story can serve as a motivation for us to do the same.

His approach to investing was simple, yet effective, and involved a deep understanding of his own financial needs and risk tolerance. By taking the time to educate himself and creating a personalized investment plan, he was able to make informed decisions that ultimately led to his success. This highlights the importance of financial literacy and the need to take control of our own financial lives.

Achieving Early Retirement Through Smart Investing

When it comes to achieving early retirement, setting clear financial goals is essential. This involves defining what you want to accomplish in both the short and long term, such as saving for a down payment on a house or building a retirement nest egg. By establishing specific, achievable objectives, you can create a roadmap for your financial future and make informed decisions about your investments.

Developing a diversified investment portfolio is crucial for achieving long-term financial success. This can include a mix of low-risk investments like bonds, CDs, and high-yield savings accounts, as well as higher-risk investments like stocks or real estate. For example, you might allocate 40% of your portfolio to low-risk investments and 60% to higher-risk investments, depending on your risk tolerance and financial goals.

Some key components of a diversified investment portfolio include:

- Low-risk investments like bonds, which provide a fixed income stream and relatively low risk

- High-yield savings accounts, which offer easy access to your money and a higher interest rate than traditional savings accounts

- Higher-risk investments like stocks or real estate, which offer the potential for higher returns over the long term

It's also important to consider your risk tolerance and adjust your investment portfolio accordingly, as this can help you avoid taking on too much risk and minimize potential losses.

To create a personalized investment plan tailored to your needs and goals, consider consulting a financial advisor. They can help you assess your risk tolerance, identify areas for improvement, and develop a customized investment strategy that aligns with your objectives. By working with a financial advisor, you can gain a deeper understanding of your investment options and make informed decisions about your financial future, ultimately helping you achieve your goal of early retirement.

Building Multiple Income Streams for Financial Security

Having a single source of income can be a significant financial risk, as it leaves you vulnerable to job loss, market fluctuations, and other unforeseen events. To mitigate this risk, it's essential to explore alternative sources of income that can provide a financial safety net. For instance, renting out a spare room on Airbnb or investing in a rental property can generate a steady stream of income and help diversify your financial portfolio.

Developing in-demand skills is another effective way to increase your earning potential and create new income streams. By acquiring skills like coding, writing, or designing, you can offer high-value services to clients and command higher rates. For example, learning to code can open up opportunities for freelance web development or app design, allowing you to work on a project-by-project basis and earn a significant income.

To get started, consider the following skills that are in high demand:

- Learning to code or web development

- Writing or content creation

- Graphic design or digital art

These skills can be learned through online courses or tutorials, and can be applied to a variety of industries and projects.

Creating and selling digital products is another lucrative way to generate passive income and build multiple income streams. Digital products, such as ebooks, courses, or software, can be created once and sold multiple times, providing a steady stream of income with minimal ongoing effort. For example, if you have expertise in a particular area, you can create an online course teaching others about that topic, and sell it on platforms like Udemy or Skillshare.

By creating and selling digital products, you can tap into the growing demand for online learning and entertainment, and earn a significant income from your creations. Some popular types of digital products include:

- Ebooks or Kindle books

- Online courses or tutorials

- Software or mobile apps

These products can be marketed and sold through various channels, including social media, email marketing, and affiliate marketing, allowing you to reach a wide audience and generate significant sales.

Budgeting and Saving Strategies for Long-Term Success

To achieve long-term financial success, it's essential to establish a solid foundation for budgeting and saving. Implementing a 50/30/20 budget is a great starting point, where 50% of your income goes towards necessary expenses like rent, utilities, and groceries. This allocation ensures you're covering your basic needs while leaving room for other financial goals.

When allocating your income, prioritize needs over wants to avoid unnecessary expenses. For instance, instead of dining out frequently, consider cooking at home and saving the difference. By cutting back on discretionary spending, you can redirect those funds towards saving and debt repayment, setting yourself up for long-term financial stability.

To make the most of your budget, consider the following strategies:

- Track your expenses to identify areas where you can cut back

- Create a list of financial goals, such as building an emergency fund or paying off debt

- Automate your savings by setting up regular transfers to your savings or investment accounts

By following these steps, you'll be better equipped to manage your finances effectively and make progress towards your long-term goals.

Taking advantage of tax-advantaged accounts is another key aspect of long-term financial planning. Consider contributing to a 401(k) or IRA, which can help optimize your savings and investments. For example, if your employer offers a 401(k) matching program, contribute enough to maximize the match, as this is essentially free money that can add up over time. By leveraging these accounts, you can reduce your tax liability while building a secure financial future.

Minimizing Debt and Optimizing Credit Scores

To get started on minimizing debt and optimizing credit scores, it's essential to create a debt repayment plan. This plan should focus on high-interest debts first, such as credit card balances, as they can quickly add up and become overwhelming. By prioritizing these debts, you can save money on interest payments and become debt-free faster.

When creating a debt repayment plan, consider consolidation or balance transfer options. For example, you can consolidate multiple credit card balances into a single personal loan with a lower interest rate, making it easier to manage your debt. This can simplify your payments and save you money on interest.

To maintain a healthy credit score, it's crucial to make on-time payments, keep credit utilization low, and avoid new credit inquiries. Here are some tips to help you achieve this:

- Set up automatic payments for your bills to ensure you never miss a payment

- Keep your credit utilization ratio below 30% to show lenders you can manage your debt responsibly

- Limit your credit applications to only when necessary, as too many inquiries can negatively affect your credit score

Working with a credit counselor or financial advisor can be beneficial in developing a personalized debt management plan. They can help you assess your financial situation, create a customized plan, and provide guidance on managing your debt and credit. With their expertise, you can make informed decisions about your financial situation and achieve your goals of minimizing debt and optimizing your credit score.

By following these steps and staying committed to your debt repayment plan, you can improve your financial health and achieve long-term stability. Remember to regularly review and adjust your plan as needed to ensure you're on track to meeting your financial goals. With patience, discipline, and the right guidance, you can minimize debt and optimize your credit score, setting yourself up for a more secure financial future.

Maintaining Financial Discipline and Avoiding Lifestyle Inflation

Maintaining financial discipline is crucial for achieving long-term financial stability. To start, practice mindful spending by being aware of your expenses and avoiding impulse purchases. This can be as simple as taking a few seconds to think before buying something, or implementing a 30-day waiting period for non-essential purchases.

One of the main reasons people struggle with financial discipline is the temptation to compare themselves to others. Set realistic expectations and focus on your own financial journey, rather than trying to keep up with your neighbors or friends. For example, instead of buying a luxury car to impress others, consider opting for a more affordable and reliable vehicle that fits within your budget.

To avoid lifestyle inflation, it's essential to regularly review and adjust your budget and investment plan. This can be done by:

- tracking your expenses to identify areas where you can cut back

- adjusting your budget to account for changes in income or expenses

- rebalancing your investment portfolio to ensure it remains aligned with your financial goals

By doing so, you can ensure you're on track to meet your goals and make progress towards financial freedom.

Another key aspect of maintaining financial discipline is avoiding the temptation to upgrade your lifestyle as your income increases. Instead of using raises or bonuses to buy luxury items, consider putting that money towards your savings or investments. For instance, you could use the 50/30/20 rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and investing.

By following these tips and staying committed to your financial goals, you can avoid lifestyle inflation and maintain financial discipline. Remember, financial freedom is a marathon, not a sprint, and it's essential to stay focused on your long-term goals. With time and practice, you'll develop the habits and mindset necessary to achieve financial stability and success.

Frequently Asked Questions (FAQ)

How can I start investing with little to no money?

Investing can seem daunting when you're just starting out, especially if you think you need a lot of money to get started. However, the truth is that you can begin investing with little to no money. By exploring low-cost options, you can start building your portfolio and working towards your financial goals.

One great place to start is with low-cost index funds, which offer a diversified portfolio of stocks or bonds at a lower cost than traditional mutual funds. These funds are often available through online brokerages or investment platforms, and they can provide a solid foundation for your investment portfolio. For example, Vanguard and Schwab offer a range of low-cost index funds with minimal investment requirements.

Robo-advisors are another option for investing with little to no money. These automated platforms use algorithms to create and manage a diversified portfolio based on your investment goals and risk tolerance. Some popular robo-advisors include Betterment and Wealthfront, which offer low fees and minimal investment requirements.

If you're looking for an even more accessible way to start investing, consider micro-investing apps like Acorns or Stash. These apps allow you to invest small amounts of money into a diversified portfolio, often with no minimum balance requirements. Here are some benefits of micro-investing apps:

- Low or no minimum investment requirements

- Automatic investments from your checking account or payroll

- Diversified portfolios with a range of investment options

These apps can be a great way to get started with investing, even if you only have a few dollars to spare. By taking advantage of low-cost investment options and micro-investing apps, you can start building wealth over time, even with a small amount of money.

What are some common mistakes to avoid when trying to retire early?

When it comes to retiring early, having a solid plan in place is crucial to ensure a smooth transition. Underestimating expenses is a common mistake that can quickly derail retirement plans, as it can lead to unexpected financial burdens. For instance, failing to account for expenses such as travel, hobbies, and entertainment can result in a significant shortfall in retirement savings.

Failing to plan for healthcare costs is another mistake that can have severe financial consequences. Healthcare costs can be significant, especially in retirement, and failing to account for them can lead to financial distress. It is essential to factor in healthcare costs, including insurance premiums, out-of-pocket expenses, and long-term care costs, when creating a retirement plan.

To avoid common mistakes, it is essential to create a comprehensive retirement plan that takes into account various expenses and financial considerations. Some key considerations to keep in mind include:

- underestimating expenses, such as housing, food, and transportation costs

- failing to plan for healthcare costs, including insurance premiums and out-of-pocket expenses

- not diversifying investments, which can lead to significant losses in the event of a market downturn

Not diversifying investments can also have severe financial consequences, as it can lead to significant losses in the event of a market downturn. By creating a diversified investment portfolio that includes a mix of low-risk and high-risk investments, retirees can help protect their retirement savings and ensure a steady income stream.

To get started on creating a comprehensive retirement plan, it is essential to track expenses, create a budget, and start saving and investing early. For example, using the 50/30/20 rule, which allocates 50% of income towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment, can help create a solid foundation for retirement planning. By avoiding common mistakes and creating a comprehensive plan, individuals can increase their chances of a successful and stress-free early retirement.

How can I stay motivated and disciplined on my path to financial independence?

Achieving financial independence requires a long-term commitment, and staying motivated is crucial to success. To maintain momentum, it's essential to set clear goals that align with your values and priorities. For instance, you might aim to pay off student loans, build an emergency fund, or save for a down payment on a house.

Tracking progress is also vital to staying motivated, as it allows you to see how far you've come and make adjustments as needed. You can use a budgeting app, spreadsheet, or even a simple notebook to monitor your expenses and income. By regularly reviewing your progress, you'll be able to identify areas for improvement and make informed decisions about your finances.

Celebrating small victories along the way can be a great motivator, as it helps to build confidence and reinforce positive financial habits. Some ways to celebrate your progress include:

- Treating yourself to a small reward, like a favorite meal or activity

- Sharing your achievements with a friend or family member to increase accountability

- Reflecting on your progress and adjusting your goals as needed

By acknowledging and celebrating your small wins, you'll be more likely to stay motivated and disciplined on your path to financial independence.

To maintain discipline, it's also important to establish a routine and make healthy financial habits a part of your daily life. This might involve setting aside a specific time each week to review your budget, or automating your savings and bill payments. By making financial management a habitual part of your routine, you'll be less likely to fall off track and more likely to achieve your long-term goals.

Ultimately, staying motivated and disciplined requires a combination of clear goals, tracking progress, and celebrating small victories. By following these principles and making healthy financial habits a part of your daily life, you'll be well on your way to achieving financial independence and securing a brighter financial future.