As a student, managing finances can be overwhelming, especially when unexpected expenses arise. This article is designed to guide students in finding the most suitable personal loan options for their unique financial situations. By exploring the various types of loans available, students can make informed decisions that align with their needs and goals.

When it comes to personal loans, there are numerous options to consider, each with its own set of benefits and drawbacks. For instance, some loans may offer lower interest rates, while others may provide more flexible repayment terms. It's essential to weigh these factors carefully to determine which loan best fits your financial circumstances.

Some key factors to consider when evaluating personal loan options include:

- Interest rates and fees associated with the loan

- Repayment terms and flexibility

- Loan amounts and eligibility criteria

By understanding these factors, students can navigate the process of securing a personal loan with confidence and make a more informed decision about their financial future.

Students can think of personal loans as a tool to help bridge the financial gap during their academic journey, whether it's to cover tuition fees, living expenses, or unexpected costs. With the right loan, students can focus on their studies and achieve their academic goals without added financial stress. By exploring the options outlined in this article, students can take the first step towards securing a personal loan that meets their financial needs.

Understanding Personal Loans for Students

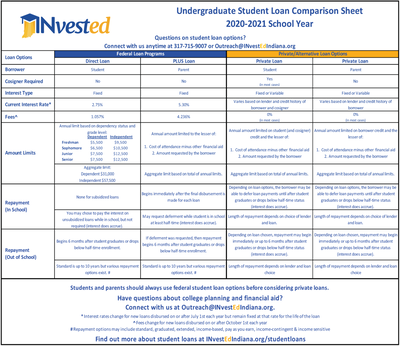

As a student, navigating the world of personal loans can be overwhelming. Federal loans are offered by the government and typically have fixed interest rates, while private loans are provided by banks, credit unions, or online lenders and often have variable interest rates. Understanding the differences between these two types of loans is crucial to making informed decisions about your financial aid.

When it comes to federal loans, the benefits include lower interest rates and more flexible repayment terms. However, the drawbacks include limited funding and strict eligibility requirements. For example, the Federal Direct Subsidized Loan has a fixed interest rate and does not require payments while the student is in school, making it a popular choice among students.

Private loans, on the other hand, can offer more funding options and faster approval processes, but often come with higher interest rates and less flexible repayment terms. To use personal loans responsibly, students can cover essential expenses such as:

- Tuition fees and other educational costs

- Living expenses, like rent and utilities

- Books and other course materials

By borrowing only what is necessary and creating a budget, students can avoid accumulating excessive debt.

To compare interest rates and terms among different lenders, students should research and evaluate their options carefully. This includes checking the annual percentage rate (APR), repayment terms, and any additional fees associated with the loan. For instance, a lender may offer a lower interest rate but charge an origination fee, which can increase the overall cost of the loan. By considering these factors, students can make informed decisions and choose the best personal loan for their needs.

Top Personal Loan Providers for Students in 2025

When it comes to finding the right personal loan as a student, it's essential to consider lenders that cater to your specific needs. Reputable lenders like SoFi, Discover, and LendingClub offer competitive interest rates and flexible repayment terms. For instance, SoFi provides unemployment protection, which can be a significant advantage for students entering the job market.

Some lenders offer special benefits for students, such as deferment options or career support. These benefits can make a significant difference in helping students manage their debt. For example, Discover offers a range of repayment term options, including the ability to defer payments for up to 3 months, giving students some breathing room after graduation.

Here are some top personal loan providers for students in 2025:

- SoFi: Offers variable interest rates and a range of repayment terms, including unemployment protection

- Discover: Provides fixed interest rates and flexible repayment terms, including deferment options

- LendingClub: Offers variable interest rates and a range of repayment terms, with a focus on creditworthiness

- Citizens Bank: Offers variable interest rates and a range of repayment terms, with a focus on student loan consolidation

Each lender has its own application process, but most require similar documentation, including proof of income, identification, and credit history. Typically, a good credit score can help you qualify for better interest rates and terms.

The application process for each lender is relatively straightforward, but it's essential to review the required documents and credit score requirements beforehand. For example, SoFi requires a minimum credit score of 680, while Discover requires a minimum credit score of 660. Having all the necessary documents ready, such as pay stubs and tax returns, can help speed up the application process.

In terms of customer service, some lenders stand out for their support and resources. For instance, LendingClub offers a range of financial education tools and resources to help students manage their debt. Citizens Bank also provides a dedicated customer service team to help students with their loan applications and repayment questions. By considering these factors and choosing the right lender, students can find a personal loan that meets their needs and helps them achieve their financial goals.

Managing Debt and Repayment Strategies

Creating a budget is a crucial step in managing debt, as it helps you understand where your money is going and identify areas for reduction. By prioritizing debt repayment, you can free up more funds to tackle your outstanding balances. For example, consider using the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment.

To minimize interest payments, it's essential to focus on high-interest loans first, such as credit card debt. You can also consider consolidating debt into a lower-interest loan or balance transfer credit card. Additionally, making timely payments and avoiding late fees can help reduce the overall cost of your debt.

Some effective strategies for paying off loans early include:

- Making bi-weekly payments instead of monthly payments, which can help reduce the principal amount and interest paid over time

- Applying extra funds towards the principal, such as tax refunds or bonuses

- Using the snowball method, where you pay off smaller loans first to build momentum and confidence

These strategies can help you pay off your loans faster and save money on interest.

Missing payments or defaulting on a loan can have severe consequences, including damage to your credit score, late fees, and even wage garnishment. It's essential to communicate with your lender if you're struggling to make payments and explore options such as deferment or forbearance. If you're a student struggling with debt, there are resources available to help, such as the National Foundation for Credit Counseling or the Financial Aid Office at your university.

For students struggling with debt, it's crucial to seek help as soon as possible to avoid long-term financial damage. You can start by reviewing your budget and identifying areas for reduction, then prioritizing your debt repayment. Remember, managing debt and repayment requires patience, discipline, and the right strategies – but with the right approach, you can achieve financial freedom and start building a brighter future.

Alternative Options to Consider

When it comes to managing student loan debt, exploring alternative funding sources can be a great way to reduce financial burden. Scholarships and grants are excellent options to consider, as they provide funding that does not need to be repaid. For example, students can search for scholarships on websites like Fastweb or Scholarships.com to find opportunities that match their eligibility criteria.

Income-driven repayment plans are another alternative to consider, offering benefits such as lower monthly payments and potential loan forgiveness. These plans, including Income-Based Repayment (IBR) and Pay As You Earn (PAYE), tie monthly payments to income and family size, making them more manageable for borrowers. To be eligible for these plans, borrowers typically need to have a partial financial hardship, which is determined by the federal government.

Some of the benefits of income-driven repayment plans include:

- Lower monthly payments, which can help borrowers avoid default

- Potential loan forgiveness after a certain number of payments, usually 20 or 25 years

- Flexibility to switch plans if income or family size changes

It's essential to review the terms and conditions of each plan to determine which one is the best fit.

While alternative options can provide relief, they also have potential drawbacks. For instance, income-driven repayment plans may result in longer repayment periods, which can increase the total amount paid over time. Additionally, some alternative options may come with higher interest rates, making it essential to carefully review the terms before committing. By weighing the pros and cons, borrowers can make informed decisions about their student loan debt and choose the best path forward.

Conclusion and Next Steps

As you consider taking out a personal loan, it's essential to remember that responsible borrowing and repayment are crucial for maintaining a healthy financial profile. By doing so, you can avoid accumulating excessive debt and instead use loans as a tool to achieve your financial goals. For instance, using a loan to cover unexpected expenses or consolidate debt can be a smart move when done thoughtfully.

To make informed decisions, it's vital to research and compare personal loan options, taking into account your individual financial needs and goals. This includes evaluating interest rates, repayment terms, and fees associated with each loan. You can start by exploring online resources, such as loan comparison websites or financial forums, to get a better understanding of what's available.

Some key factors to consider when evaluating personal loan options include:

- Interest rates and fees

- Repayment terms and flexibility

- Loan amounts and eligibility criteria

- Customer service and support

By carefully considering these factors, you can find a loan that aligns with your financial situation and helps you achieve your goals.

To manage your debt and achieve financial stability, it's also important to have the right tools and resources at your disposal. You can start by creating a budget and tracking your expenses to get a clear picture of your financial situation. Additionally, you can utilize online resources, such as debt repayment calculators or financial planning apps, to help you stay on track and make informed decisions.

For further guidance and support, you can visit the BudgetWiseGrad website, which offers a range of resources and tools to help students manage their debt and achieve financial stability. From in-depth guides and tutorials to interactive calculators and quizzes, you'll find everything you need to take control of your finances and build a brighter financial future.

Frequently Asked Questions (FAQ)

What are the typical interest rates for student personal loans?

When it comes to student personal loans, understanding the interest rates is crucial for making informed decisions. Interest rates vary by lender, but students can expect to see rates between 4% and 12% APR. This range can significantly impact the total cost of the loan, so it's essential to shop around and compare rates from different lenders.

To give you a better idea, here are some factors that can influence the interest rate you're offered:

- Credit score: A good credit score can help you qualify for lower interest rates

- Income: Lenders may offer better rates to borrowers with a stable income

- Loan term: Longer loan terms may come with higher interest rates

These factors can vary by lender, so it's essential to review the terms and conditions before applying for a loan.

For example, a student who borrows $10,000 at 6% APR will pay less in interest over the life of the loan compared to someone who borrows the same amount at 10% APR. By understanding how interest rates work and comparing rates from different lenders, students can make more informed decisions about their student personal loans and save money in the long run.

Can I use a personal loan to cover non-tuition expenses, such as living costs or travel?

As a student, managing finances can be challenging, especially when it comes to covering non-tuition expenses. Personal loans can be a viable option to consider, as some lenders allow students to use these loans for living costs, travel, and other expenses. However, it's essential to review the terms and conditions before borrowing to ensure you understand the repayment terms and interest rates.

When exploring personal loan options, it's crucial to consider the lender's requirements and restrictions. Some lenders may have specific rules about using personal loans for non-tuition expenses, so it's vital to read the fine print. For example, some lenders may require students to provide proof of enrollment or income to qualify for a personal loan.

Here are some key factors to consider when using a personal loan for non-tuition expenses:

- Interest rates: Compare rates among lenders to find the most competitive option

- Repayment terms: Understand the repayment schedule and any potential penalties for late payments

- Fees: Check for any origination fees, late payment fees, or other charges associated with the loan

By carefully evaluating these factors, students can make informed decisions about using personal loans to cover non-tuition expenses.

It's also important to explore alternative options for covering living costs and travel expenses, such as part-time jobs, scholarships, or grants. Additionally, students can consider budgeting and saving strategies to reduce their reliance on personal loans. By being mindful of their finances and exploring all available options, students can make the most of their personal loan and achieve their academic and financial goals.

How do I know if I qualify for a student personal loan, and what are the typical credit score requirements?

When it comes to qualifying for a student personal loan, the requirements can vary significantly from one lender to another. Generally, lenders consider factors such as credit score, income, and debt-to-income ratio to determine eligibility. For students, a good credit score can make a big difference in getting approved for a loan.

Typically, students can expect to need a credit score of 600 or higher to qualify for a personal loan, although some lenders may have more lenient requirements. It's essential to check the specific requirements of each lender, as some may offer more flexible terms than others. By researching and comparing different lenders, students can find the best options for their financial situation.

To give you a better idea, here are some general guidelines on credit score requirements:

- A credit score of 600-649 may qualify for a loan with a higher interest rate

- A credit score of 650-699 may qualify for a loan with a moderate interest rate

- A credit score of 700 or higher may qualify for a loan with a lower interest rate

Keep in mind that these are general guidelines, and the actual credit score requirements may vary depending on the lender and other factors.

It's also important to note that some lenders may offer personal loans specifically designed for students, which may have more flexible credit score requirements. These loans may also offer benefits such as deferred payments or lower interest rates, making them a more attractive option for students. By doing your research and comparing different lenders, you can find the best student personal loan to suit your needs.