As a graduate student, financing your education can be a daunting task, but with the right resources, you can make informed decisions. The best graduate student loans for 2025 offer competitive interest rates, flexible repayment terms, and generous borrowing limits. For instance, federal loans like the Direct Unsubsidized Loan and the Grad PLUS Loan are popular options among graduate students.

When exploring graduate student loan options, it's essential to consider key features such as interest rates, fees, and repayment terms. Some lenders offer perks like autopay discounts, cosigner release options, and forbearance programs. Graduate students should also look for loans with low or no origination fees, as these can save them hundreds or even thousands of dollars in the long run.

To get started, research and compare different loan options using online tools and resources. Here are some factors to consider when applying for graduate student loans:

- Check your credit score and history to determine your eligibility and potential interest rate

- Complete the Free Application for Federal Student Aid (FAFSA) to explore federal loan options

- Compare rates and terms from multiple lenders to find the best fit for your needs

By following these tips and doing your research, you can find the right graduate student loan to help you achieve your academic and financial goals.

In the following sections, we'll delve into the specifics of the best graduate student loans for 2025, including application tips and strategies for managing your debt. Whether you're pursuing a master's degree, PhD, or professional certification, we'll provide you with the information and guidance you need to make informed decisions about your financial aid.

Understanding Graduate Student Loans

As a graduate student, navigating the world of student loans can be overwhelming. Federal and private graduate student loans are two distinct options, each with its own set of interest rates and repayment terms. Federal loans, for instance, typically offer fixed interest rates and more flexible repayment plans.

When exploring private loan options, credit scores play a significant role in determining eligibility and interest rates. A good credit score can help you qualify for lower interest rates, while a poor credit score may lead to higher rates or even loan denial. It's essential to check your credit report and work on improving your score before applying for private loans.

Federal loans are often a more popular choice among graduate students due to their favorable terms. Some examples of federal loans include:

- Direct Unsubsidized Loans, which offer a fixed interest rate and a six-month grace period after graduation

- Grad PLUS Loans, which require a credit check but offer more flexible repayment plans and higher borrowing limits

These loans can be used to cover various expenses, including tuition, fees, and living costs.

In contrast, private loans often have variable interest rates and stricter repayment terms. However, they may be a viable option for students who have exhausted their federal loan options or need additional funding. When shopping for private loans, it's crucial to compare interest rates and repayment terms from different lenders to find the best deal.

To make the most of your graduate student loans, it's essential to borrow wisely and create a repayment plan that works for you. Consider factors like interest rates, fees, and repayment terms when choosing a loan, and don't hesitate to reach out to your school's financial aid office or a financial advisor for guidance. By being informed and proactive, you can manage your debt effectively and achieve your academic and financial goals.

Best Federal Graduate Student Loans

As a graduate student, navigating the world of federal loans can be overwhelming. Direct Unsubsidized Loans are a popular option, offering benefits like fixed interest rates and flexible repayment terms. These loans are available to students who are enrolled at least half-time in a graduate program.

The application process for Direct Unsubsidized Loans typically begins with completing the Free Application for Federal Student Aid (FAFSA). This form helps determine your eligibility for federal loans, and you can submit it online or through your school's financial aid office. By completing the FAFSA, you'll also be considered for other types of federal aid.

To be eligible for Direct Unsubsidized Loans, you must be a U.S. citizen or eligible non-citizen, have a valid Social Security number, and be enrolled in a graduate program. You'll also need to maintain satisfactory academic progress and not be in default on any federal loans. Some examples of eligible graduate programs include master's and doctoral degrees.

In addition to Direct Unsubsidized Loans, Grad PLUS Loans are another option for graduate students. The eligibility criteria for Grad PLUS Loans include a decent credit history and enrollment in a graduate program. You can check your credit report for free and work on improving your credit score before applying for a Grad PLUS Loan.

The application process for Grad PLUS Loans involves completing the FAFSA and a separate application for the Grad PLUS Loan. You'll need to provide personal and financial information, as well as details about your graduate program. Some key things to keep in mind when applying for a Grad PLUS Loan include:

- Checking your credit report for errors or negative marks

- Gathering required documents, such as tax returns and identification

- Completing the application carefully and accurately

One of the advantages of federal loans is the availability of income-driven repayment plans. These plans can help make your monthly payments more manageable by basing them on your income and family size. For example, the Income-Based Repayment (IBR) plan can cap your monthly payments at 10% or 15% of your discretionary income.

Federal loans also offer loan forgiveness options, which can be a huge relief for graduate students. Some examples of loan forgiveness programs include:

- Public Service Loan Forgiveness (PSLF), which forgives loans for borrowers working in public service jobs

- Teacher Loan Forgiveness, which forgives loans for teachers working in low-income schools

- Perkins Loan Cancellation, which forgives loans for borrowers working in certain fields, such as nursing or law enforcement

Overall, federal loans can provide a range of benefits and options for graduate students. By understanding the application process and eligibility criteria for Direct Unsubsidized Loans and Grad PLUS Loans, you can make informed decisions about your financing options. Be sure to explore income-driven repayment plans and loan forgiveness options to find the best fit for your situation.

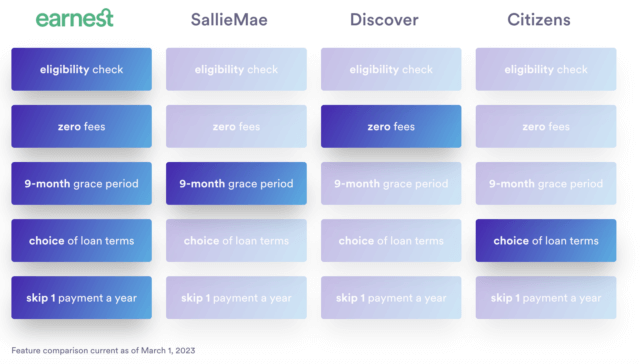

Top Private Graduate Student Loans

When exploring private graduate student loans, it's essential to compare interest rates and repayment terms from various lenders. SoFi and Discover are two popular options, offering competitive interest rates and flexible repayment plans. For instance, SoFi offers variable interest rates ranging from 4.13% to 11.23%, while Discover provides fixed interest rates between 4.99% and 12.99%.

To make an informed decision, consider lender fees, such as origination fees, late payment fees, and returned payment fees. These fees can add up quickly, increasing the overall cost of the loan. Borrowers should also look into borrower benefits, such as career support and loan forgiveness programs, which can provide a safety net in case of financial hardship.

Some private lenders offer unique benefits, such as:

- Career coaching and job placement assistance

- Loan forgiveness or discharge options

- Autopay discounts and loyalty rewards

These benefits can provide valuable support and protection for graduate students navigating their financial futures.

When comparing private loans, consider your individual circumstances, such as your credit score, income, and debt-to-income ratio. It's crucial to evaluate the total cost of the loan, including interest rates, fees, and repayment terms. By doing so, you can choose the best private loan for your needs and avoid unnecessary debt.

To get started, research and compare rates from multiple lenders, and consider the following tips:

- Check your credit report and score to determine your eligibility

- Read reviews and testimonials from current and former borrowers

- Calculate your total loan costs using online tools and calculators

By taking the time to compare and evaluate private graduate student loans, you can make an informed decision and set yourself up for long-term financial success.

Applying for Graduate Student Loans

To get started with graduate student loans, you'll need to fill out the Free Application for Federal Student Aid (FAFSA). This application is used to determine your eligibility for federal, state, and institutional financial aid, including loans and grants. The FAFSA process typically begins in October of each year, and it's essential to submit your application as early as possible to ensure you receive the best possible aid package.

The FAFSA application will ask for personal and financial information, including your social security number, tax returns, and family income. You'll also need to provide information about the schools you're interested in attending, as this will help determine your aid eligibility. For example, if you're planning to attend a public university, you may be eligible for state-specific aid, such as the Federal Pell Grant or the Federal Supplemental Educational Opportunity Grant.

Once you've submitted your FAFSA, you'll receive a Student Aid Report (SAR) that summarizes your application and provides an Expected Family Contribution (EFC). Your EFC will be used to determine your eligibility for federal loans, including the Direct Unsubsidized Loan and the Graduate PLUS Loan. To compare and choose the best loan options, consider the following factors:

- Interest rates: Look for loans with lower interest rates to save money over the life of the loan

- Repayment terms: Consider loans with flexible repayment plans, such as income-driven repayment or deferment options

- Fees: Check for any origination fees or late payment fees that may apply

When completing loan applications, make sure to carefully review the terms and conditions before signing. It's also essential to avoid common mistakes, such as not borrowing enough to cover all your expenses or not understanding the repayment terms. For instance, if you borrow a Direct Unsubsidized Loan, you'll be responsible for paying the interest that accrues while you're in school, which can add up quickly.

To avoid mistakes, take the time to read and understand the loan application, and don't hesitate to ask for help if you need it. You can also use online resources, such as the Federal Student Aid website, to get personalized guidance and advice. Additionally, consider the following tips:

- Keep track of your loan applications and deadlines using a spreadsheet or planner

- Make sure to sign and submit your loan applications electronically to avoid delays

- Review and understand your loan disclosure statements before accepting the loan

By following these steps and tips, you can navigate the graduate student loan process with confidence and make informed decisions about your financial aid. Remember to stay organized, ask for help when needed, and carefully review your loan options to ensure you're making the best choices for your financial situation.

Managing Graduate Student Loan Debt

When it comes to managing graduate student loan debt, it's essential to start by borrowing only what you need. This means carefully calculating your expenses and avoiding the temptation to take out more loans than necessary. By doing so, you can minimize your debt burden and set yourself up for long-term financial stability.

To further reduce your debt, consider exploring income-driven repayment plans, which can help lower your monthly payments based on your income level. For example, the Pay As You Earn (PAYE) plan and the Income-Based Repayment (IBR) plan are two popular options that can provide relief for borrowers. These plans can be especially helpful for graduates who are just starting their careers and may not have a high income.

Another effective strategy for managing debt is loan consolidation and refinancing. This involves combining multiple loans into one loan with a single interest rate and monthly payment, which can simplify your finances and potentially save you money. The benefits of loan consolidation and refinancing include:

- simplified payments, as you'll only have to make one payment per month

- potentially lower interest rates, which can save you thousands of dollars over the life of the loan

- more flexible repayment terms, which can help you avoid default and stay on track with your payments

In addition to these strategies, there are many resources available to help you manage your debt and achieve financial stability. Budgeting tools, such as Mint and You Need a Budget (YNAB), can help you track your expenses and stay on top of your finances. Credit counseling services, such as the National Foundation for Credit Counseling (NFCC), can also provide personalized advice and support to help you develop a plan to pay off your debt.

By taking advantage of these resources and strategies, you can take control of your graduate student loan debt and set yourself up for long-term financial success. Remember to always prioritize your financial well-being and seek help when you need it – with the right tools and support, you can overcome debt and achieve your financial goals. For more information and guidance, be sure to check out the resources and tools available on our website, which can provide you with the knowledge and expertise you need to manage your debt and build a brighter financial future.

Frequently Asked Questions (FAQ)

What are the current interest rates for federal graduate student loans?

To find the most up-to-date information on interest rates for federal graduate student loans, it's essential to check the official Federal Student Aid website. This website provides the latest details on interest rates, repayment terms, and other vital information. By visiting the site, you can get a clear understanding of the current rates and plan your finances accordingly.

When checking the Federal Student Aid website, you can find the current interest rates for different types of federal graduate student loans, including Direct Unsubsidized Loans and Graduate PLUS Loans. These rates can change from year to year, so it's crucial to verify the information before taking out a loan. You can also compare the interest rates of different loan options to make an informed decision.

Here are some key points to consider when reviewing the current interest rates:

- Direct Unsubsidized Loans typically have a fixed interest rate, which can vary depending on the loan disbursement period

- Graduate PLUS Loans often have a higher interest rate compared to Direct Unsubsidized Loans, but may offer more flexible repayment terms

- Interest rates can impact the total cost of your loan over time, so it's essential to factor this into your decision

It's also important to note that interest rates are just one factor to consider when choosing a federal graduate student loan. You should also think about the loan's repayment terms, fees, and borrower benefits. By taking the time to research and compare your options, you can make a more informed decision and create a smart plan for managing your graduate school debt.

Can I refinance my graduate student loans to a lower interest rate?

Refinancing your graduate student loans can be a great way to save money on interest and lower your monthly payments. If you have a good credit score and a stable income, you may be able to refinance your loans to a lower interest rate. This can be especially beneficial if you have high-interest loans, such as those with variable rates or high origination fees.

When considering refinancing, it's essential to evaluate your individual creditworthiness and lender criteria. Lenders typically look at factors such as your credit score, income, and debt-to-income ratio to determine your eligibility for refinancing. For example, if you have a credit score above 700 and a steady income, you may be more likely to qualify for a lower interest rate.

Here are some things to consider when refinancing your graduate student loans:

- Check your credit report to ensure it's accurate and up-to-date

- Compare rates and terms from multiple lenders to find the best option

- Consider working with a lender that offers flexible repayment terms and no origination fees

By doing your research and shopping around, you can find a refinancing option that works for you and helps you save money on your graduate student loans. It's also important to read reviews and ask questions to ensure you're working with a reputable lender. Refinancing can be a great way to simplify your finances and reduce your debt burden.

Are there any income-driven repayment plans available for graduate student loans?

As a graduate student, managing your student loan debt can be overwhelming. Fortunately, there are options available to help make your payments more affordable. Income-driven repayment plans, for instance, can be a valuable resource in reducing your monthly payments.

Income-driven repayment plans, such as Income-Based Repayment and Pay As You Earn, are designed to adjust your monthly payments according to your income and family size. This means that if you have a lower income, your monthly payments will be lower as well. For example, if you're working part-time or have a lower-paying job, these plans can help make your payments more manageable.

Some of the benefits of income-driven repayment plans include:

- Lower monthly payments, which can help reduce financial stress

- Flexibility to adjust your payments as your income changes

- Potential for loan forgiveness after a certain number of payments

These plans are typically available for federal graduate student loans, such as Direct Unsubsidized Loans and Grad PLUS Loans. It's essential to review the specific eligibility requirements and terms for each plan to determine which one is best for you.

To get started with an income-driven repayment plan, you'll typically need to submit an application and provide documentation of your income and family size. You can usually do this through your loan servicer's website or by contacting them directly. By taking advantage of these plans, you can make your graduate student loan payments more affordable and focus on building a stable financial future.