As a student, it's essential to stay informed about changes in student loan policies that can affect your financial future. Recently, Trump's spending bill introduced a significant change to student loans, which may have a lasting impact on students' ability to manage their debt. This change can be a cause for concern, but being aware of the implications can help you make informed decisions about your financial aid.

The new policy aims to simplify the student loan repayment process, but it also means that some benefits, such as Public Service Loan Forgiveness, may be limited. For instance, students who were relying on this program to forgive their loans after working in public service for a certain number of years may need to reassess their repayment strategy. It's crucial to understand how these changes can affect your individual circumstances and plan accordingly.

To navigate these changes, it's helpful to consider the following key points:

- Review your current loan terms and repayment options to see if you're eligible for any benefits that may be affected by the new policy

- Research alternative repayment plans, such as income-driven repayment, that can help you manage your debt

- Stay up-to-date with the latest developments in student loan policy to ensure you're making the most of your financial aid

By taking a proactive approach to your student loans, you can mitigate the potential impact of these changes and set yourself up for long-term financial success. It's also a good idea to consult with a financial advisor or student loan expert to get personalized advice on managing your debt.

Understanding the Change in Student Loans

The recent changes to student loans in Trump's spending bill have significant implications for students and families. These changes affect borrowing limits and repayment terms, which can impact the overall cost of higher education. For instance, the bill eliminates the subsidized loan program for graduate students, which means they will no longer be eligible for loans where the government pays the interest while they are in school.

This change could have a profound impact on students' decisions to pursue higher education, particularly in fields like law and medicine that often require significant debt. Students may need to consider alternative options, such as attending a community college or a public university, to reduce their debt burden. Additionally, students may need to explore other financing options, such as private scholarships or part-time jobs, to supplement their income.

Some of the key changes to student loans include:

- Increased borrowing limits for undergraduate students, which can lead to higher debt loads

- Changes to repayment terms, such as income-driven repayment plans, which can affect monthly payments

- Elimination of the Public Service Loan Forgiveness program, which can impact students who plan to work in public service

These changes can have far-reaching consequences for students, including increased debt loads or longer repayment periods. For example, a student who borrows the maximum amount for a graduate program may face repayment periods of 20-25 years, which can be daunting.

To navigate these changes, students should consider creating a personalized budget and repayment plan. This can involve calculating monthly payments, exploring income-driven repayment options, and prioritizing high-interest debt. By taking a proactive approach to managing their debt, students can minimize the impact of these changes and achieve their long-term financial goals. Students can also seek guidance from financial aid counselors or online resources to make informed decisions about their student loans.

Impact on Aspiring Doctors and Lawyers

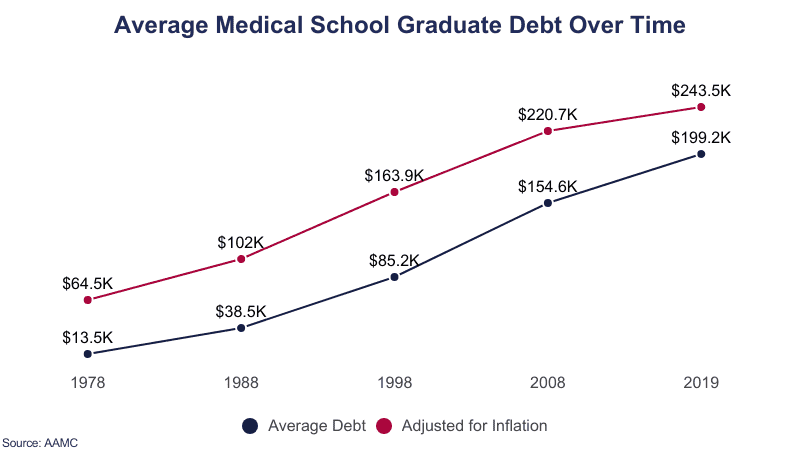

Pursuing a medical or law degree can be a costly endeavor, with many students graduating with significant debt. The financial implications of these degrees can be overwhelming, with potential increases in debt and a lasting impact on future financial health. For instance, the average medical student debt can range from $200,000 to over $500,000, depending on the institution and location.

Aspiring doctors and lawyers can navigate the changed loan landscape by exploring alternative options to offset costs. This includes searching for scholarship opportunities, such as the National Health Service Corps Scholarship for medical students or the American Bar Association's scholarship for law students. Additionally, side hustles like tutoring, freelancing, or part-time jobs can help alleviate some of the financial burden.

Some practical tips for students in these fields include:

- Creating a budget and tracking expenses to stay on top of finances

- Researching and applying for scholarships and grants

- Considering income-driven repayment plans or loan forgiveness programs

By taking proactive steps, students can better manage their debt and set themselves up for long-term financial stability.

The potential long-term effects of high debt burdens on the legal and medical professions are a concern, as they may discourage talented individuals from pursuing these careers. If bright minds are deterred from entering these fields due to financial constraints, it could have a ripple effect on the overall quality of healthcare and legal services. This highlights the need for students, educators, and policymakers to work together to find solutions and create a more sustainable financial landscape for aspiring doctors and lawyers.

Ultimately, with careful planning, resourcefulness, and a bit of creativity, students pursuing medical or law degrees can mitigate the financial implications and set themselves up for success in their chosen careers. By prioritizing financial literacy and exploring available resources, they can build a strong foundation for a secure and prosperous future.

Strategies for Managing Student Loan Debt

As a student, managing debt can seem overwhelming, but with the right strategies, you can take control of your finances. One effective way to start is by exploring income-driven repayment plans, which can help lower your monthly payments based on your income and family size. For example, the Income-Based Repayment (IBR) plan can cap your monthly payments at 10% or 15% of your discretionary income.

Understanding your loan terms is also crucial, including interest rates and the impact of compound interest. It's essential to know that compound interest can significantly increase the amount you owe over time, so making timely payments is vital. By making extra payments or paying more than the minimum each month, you can reduce the amount of interest you owe and pay off your loan faster.

To make informed decisions about your student loans, it's helpful to consider loan forgiveness programs, such as the Public Service Loan Forgiveness (PSLF) program, which can forgive part or all of your loan balance after a certain number of qualifying payments. You can also look into budgeting strategies, such as the 50/30/20 rule, which allocates 50% of your income towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment.

Some useful resources to help you manage your student loans include:

- The National Foundation for Credit Counseling (NFCC), which provides financial counseling and education

- The Federal Student Aid website, which offers tools and resources to help you understand and manage your loans

- Online budgeting tools, such as Mint or You Need a Budget (YNAB), which can help you track your expenses and stay on top of your finances

By taking the time to understand your loan terms, exploring repayment options, and creating a budget, you can develop a solid plan for managing your student loan debt. It's also essential to prioritize financial literacy and planning, as this will serve as a foundation for making informed decisions about your financial future. By being proactive and seeking out resources, you can set yourself up for long-term financial success.

In addition to these strategies, it's crucial to regularly review and adjust your budget to ensure you're on track to meet your financial goals. This may involve making adjustments to your income-driven repayment plan or exploring other loan forgiveness options. By staying informed and taking control of your finances, you can reduce your debt burden and achieve financial stability.

Alternative Paths and Side Hustles

Exploring alternative educational paths can be a great way to reduce debt burdens for students interested in law or medicine. Online courses or vocational training can provide a more affordable route to gaining the necessary skills and knowledge. For instance, online courses like Coursera or edX offer a wide range of courses in law and medicine that can be completed at a fraction of the cost of traditional university programs.

In addition to alternative educational paths, side hustles or part-time jobs can also help students offset educational expenses and reduce their reliance on loans. Some popular side hustles for students include freelancing, tutoring, or working as a research assistant. These side hustles can not only provide a steady income but also help students gain valuable work experience and build their professional network.

To get started with a side hustle, students can consider the following options:

- Freelance writing or editing for academic or professional clients

- Tutoring or teaching English as a second language online

- Working as a part-time research assistant or data analyst for a university or company

These side hustles can be done on a part-time basis, allowing students to balance their work and study commitments.

Balancing the pursuit of higher education with the need to manage debt and maintain financial health requires careful planning and time management. Students can start by creating a budget and tracking their expenses to identify areas where they can cut back on unnecessary spending. By prioritizing their spending and making smart financial decisions, students can reduce their reliance on loans and achieve their educational goals without sacrificing their financial well-being.

Ultimately, pursuing higher education requires a significant investment of time, money, and effort. However, by exploring alternative educational paths and side hustles, students can reduce their debt burden and achieve their goals without breaking the bank. With the right mindset and strategy, students can take control of their finances and set themselves up for long-term success.

Conclusion and Next Steps

As we wrap up our discussion on the recent changes in student loans, it's essential to recap the key points that affect students, particularly those pursuing law or medical degrees. The changes in interest rates and repayment terms can significantly impact the overall cost of borrowing, making it crucial for students to understand these implications. For instance, students can expect to pay more over the life of their loan due to increased interest rates.

To navigate these changes effectively, students should stay informed about updates in student loan policies and seek out resources and advice to manage their debt. This can include consulting financial advisors, exploring budgeting tools, or utilizing online resources that provide personalized guidance on managing student loan debt. By being proactive, students can make informed decisions about their financial aid options and develop a plan to tackle their debt.

Some key steps students can take to manage their debt include:

- Creating a budget that accounts for loan repayments and interest accrual

- Exploring income-driven repayment plans that can help lower monthly payments

- Considering loan forgiveness programs or refinancing options

By taking these steps, students can regain control of their financial futures and make progress towards becoming debt-free.

Students should prioritize their financial well-being and take advantage of the many tools and resources available to help them manage their debt. Whether it's consulting with a financial advisor or using online budgeting tools, there are many ways for students to take control of their finances and set themselves up for long-term success. By being proactive and informed, students can overcome the challenges posed by changing student loan policies and achieve their goals.

Frequently Asked Questions (FAQ)

How will the change in student loans affect my decision to become a doctor or lawyer?

Pursuing a career in medicine or law can be a significant investment, with student loan debt often being a major consideration. The recent changes in student loans may have a substantial impact on your decision to become a doctor or lawyer, as the cost of education continues to rise. It's essential to understand how these changes will affect your financial situation and plan accordingly.

For aspiring doctors and lawyers, the change in student loans could lead to higher debt burdens, making it crucial to carefully consider the financial implications of your decision. This includes exploring all available financial aid options, such as scholarships, grants, and income-driven repayment plans. By doing so, you can make an informed decision that aligns with your career goals and financial situation.

Some key factors to consider when evaluating the impact of student loan changes on your career choice include:

- Increased interest rates, which can result in higher monthly payments and a longer repayment period

- Changes in loan forgiveness programs, which may affect your ability to have part or all of your debt forgiven

- Alternative repayment options, such as income-driven repayment plans, which can help make your monthly payments more manageable

It's also important to research and understand the specific financial implications of your desired career path, such as the average debt load for doctors and lawyers, and the potential return on investment for your education.

To mitigate the potential financial burden of student loan debt, it's a good idea to create a personalized financial plan that takes into account your career goals, income potential, and debt obligations. This may involve working with a financial advisor or using online resources to develop a tailored plan. By being proactive and informed, you can make a more confident decision about pursuing a career in medicine or law, despite the changes in student loans.

Are there alternative educational paths that can lead to careers in law or medicine with less debt?

Pursuing a career in law or medicine can be a significant investment, often requiring substantial financial resources. However, there are alternative educational paths that can lead to these careers with less debt. For instance, online courses or part-time study options can provide flexibility and reduced tuition fees.

Online courses, in particular, have become increasingly popular, offering a range of programs and certifications in law and medicine. These courses can be completed at a lower cost and on a flexible schedule, making them an attractive option for those who cannot afford traditional university programs. Some examples of online courses include paralegal studies or medical billing and coding certifications.

Vocational training is another alternative path to consider, providing hands-on experience and specialized skills in a specific area of law or medicine. This type of training can be completed in a shorter amount of time and at a lower cost than traditional degree programs. Some examples of vocational training include:

- Emergency medical technician (EMT) training

- Legal assistant or paralegal training

- Medical laboratory technician training

These programs can lead to entry-level positions in law or medicine and provide a foundation for further education and career advancement.

Part-time study options are also available, allowing students to balance their academic pursuits with work or other responsibilities. This approach can help reduce debt burdens by enabling students to earn a steady income while completing their studies. Many universities and colleges offer part-time programs in law and medicine, including evening or weekend classes, online courses, or distance learning options. By exploring these alternative educational paths, individuals can pursue their career goals in law or medicine while minimizing their debt.

What strategies can I use to manage my student loan debt effectively?

To manage your student loan debt effectively, it's essential to start by understanding your loan terms. This includes knowing the type of loan you have, the interest rate, and the repayment period. For instance, federal loans often have more flexible repayment options compared to private loans.

Using budgeting tools is another crucial strategy for managing student loan debt. You can utilize online budgeting apps, such as Mint or You Need a Budget, to track your income and expenses, and allocate a specific amount for loan repayment each month. By doing so, you can ensure that you're making timely payments and avoiding late fees.

Exploring income-driven repayment plans can also help you manage your student loan debt. These plans allow you to make monthly payments based on your income and family size, rather than the standard repayment amount. For example, the Income-Based Repayment (IBR) plan and the Pay As You Earn (PAYE) plan are two popular options.

- The IBR plan typically requires you to pay 10% or 15% of your discretionary income towards your loans.

- The PAYE plan, on the other hand, requires you to pay 10% of your discretionary income, but it also forgives any remaining balance after 20 years.

Considering loan forgiveness programs is another effective strategy for managing student loan debt. These programs can help you eliminate some or all of your debt, depending on your profession and other factors. For example, the Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on your loans after 10 years of qualifying payments, if you work full-time in a public service job. By understanding the different loan forgiveness programs available, you can plan your career and loan repayment strategy accordingly.

Additionally, you can also take advantage of tax deductions and credits for student loan interest to reduce your taxable income. By staying informed and proactive, you can develop a personalized plan to tackle your student loan debt and achieve financial stability. It's also a good idea to consult with a financial advisor or a student loan expert to get personalized advice on managing your debt.