As a young adult, managing finances can be overwhelming, especially when you're just starting out. You may not have a side hustle or a lot of disposable income, but that doesn't mean you can't start building wealth. By adopting a few simple habits and strategies, you can set yourself up for long-term financial success.

Creating a silent wealth formula is all about making intentional decisions with your money, even if it's just a small amount. For example, starting a savings plan with just $10 a week can add up over time and help you build a safety net. This can be as simple as setting up an automatic transfer from your checking account to your savings account.

To get started, consider the following key principles:

- Live below your means by tracking your expenses and creating a budget

- Invest in yourself through education and personal development

- Take advantage of tax-advantaged accounts, such as a Roth IRA or 401(k)

By following these principles, you can create a solid foundation for your financial future and start building wealth without needing a side hustle.

Building wealth is a marathon, not a sprint, and it's essential to be patient and disciplined in your approach. By making a few small changes to your daily habits and financial decisions, you can set yourself up for long-term success and create a brighter financial future.

Understanding the Wealth Formula

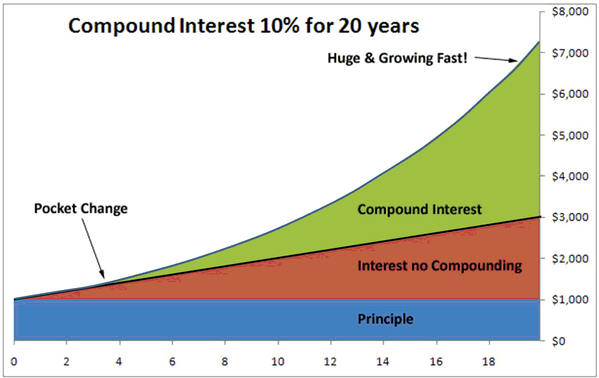

The wealth formula is a straightforward concept that involves consistent saving and strategic investing over time. By adopting this approach, individuals can set themselves up for long-term financial success. It's essential to understand that this formula requires patience and a long-term perspective to see significant results.

Starting early is key, even with small amounts, as it allows you to leverage the power of compound interest. For example, if you begin saving $100 per month at the age of 25, you'll have a significant nest egg by the time you retire. This is because your money will have decades to grow and compound, resulting in a substantial amount of wealth.

To make the most of the wealth formula, consider the following tips:

- Set clear financial goals, such as saving for a down payment on a house or retirement

- Develop a budget that accounts for regular saving and investing

- Take advantage of tax-advantaged accounts, such as 401(k) or IRA, to optimize your investments

By following these tips and maintaining a long-term perspective, you can harness the power of the wealth formula and achieve financial stability.

It's also important to remember that the wealth formula is not a get-rich-quick scheme, but rather a tried-and-true approach to building wealth over time. By being consistent and patient, you can reap significant rewards and secure a brighter financial future. As you start your journey, keep in mind that every small step counts, and even modest investments can add up to make a significant difference in the long run.

Budgeting for Wealth

To achieve financial stability and build wealth, it's essential to have a solid budget in place. Creating a budget that allocates at least 20% of your income towards savings and investments is a great starting point. This will help you prioritize your financial goals and make conscious decisions about how you spend your money.

When it comes to budgeting, it's crucial to prioritize your needs over your wants to ensure you have sufficient funds for the wealth formula. This means making a clear distinction between essential expenses, such as rent and utilities, and discretionary spending, like dining out or entertainment. By doing so, you'll be able to allocate your resources more effectively.

The 50/30/20 rule is a useful guideline for budget allocation, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment. This rule can be adjusted based on individual circumstances, but it provides a good starting point for creating a balanced budget. For example, if you earn $4,000 per month, you would allocate $2,000 towards necessary expenses, $1,200 towards discretionary spending, and $800 towards saving and debt repayment.

Some key budgeting categories to consider include:

- Housing and utilities

- Transportation and food

- Insurance and minimum debt payments

- Entertainment and hobbies

- Savings and investments

By allocating your income into these categories and prioritizing your needs over your wants, you'll be well on your way to creating a budget that supports your long-term financial goals.

To make the most of your budget, it's also important to regularly review and adjust your spending habits. This can be done by tracking your expenses, identifying areas for improvement, and making adjustments as needed. By taking a proactive approach to budgeting and prioritizing your financial goals, you'll be able to create a wealth-building plan that works for you.

Investing for Growth

As a beginner investor, it's essential to start with low-risk investment options that can help you grow your wealth over time. Index funds or ETFs are excellent choices, as they provide broad diversification and tend to be less volatile than individual stocks. For example, you can invest in a total stock market index fund, which tracks the overall performance of the stock market.

When it comes to investing, it's crucial to have a clear understanding of your financial goals and risk tolerance. Consider consulting a financial advisor who can provide personalized investment advice tailored to your needs. They can help you create a customized investment plan, taking into account your income, expenses, and long-term objectives.

To minimize risk and maximize returns, diversification is key. This means spreading your investments across different asset classes, such as:

- Stocks: individual stocks, index funds, or ETFs

- Bonds: government or corporate bonds, which provide regular income

- Real estate: investment properties or real estate investment trusts (REITs)

By diversifying your investments, you can reduce your exposure to any one particular asset class and increase the potential for long-term growth.

As you begin your investment journey, remember that patience and discipline are vital. It's essential to have a long-term perspective and avoid making impulsive decisions based on short-term market fluctuations. By following a well-thought-out investment strategy and staying informed, you can increase your chances of achieving your financial goals and securing a brighter financial future.

Avoiding Debt for Financial Health

When it comes to achieving financial health, avoiding debt is crucial. High-interest debt, in particular, can have a significant impact on long-term financial goals, such as saving for a down payment on a house or retirement. For example, if you have a credit card balance of $2,000 with an interest rate of 18%, you could end up paying over $300 in interest alone over the course of a year.

To avoid this situation, it's essential to focus on paying off high-interest loans and credit cards as soon as possible. This can be done by creating a budget and prioritizing debt repayment. Consider the snowball method, where you pay off smaller debts first to build momentum, or the avalanche method, where you tackle high-interest debts first to save the most money in interest.

Some practical tips for paying off high-interest debt include:

- Consolidating debt into a lower-interest loan or credit card

- Making more than the minimum payment each month

- Using the 50/30/20 rule to allocate income towards debt repayment, savings, and essential expenses

By following these tips, you can pay off high-interest debt quickly and efficiently, freeing up more money in your budget for savings and investments.

Building an emergency fund is also vital for preventing debt during unexpected expenses, such as car repairs or medical bills. Aim to save 3-6 months' worth of living expenses in a easily accessible savings account. This fund will provide a cushion in case of unexpected expenses, allowing you to avoid going into debt and stay on track with your financial goals. By combining debt repayment with emergency savings, you can achieve long-term financial stability and security.

Monitoring Progress and Staying Motivated

To achieve financial success, it's essential to regularly review your budget and investment progress. This can be done by scheduling monthly or quarterly check-ins to assess your spending habits, savings, and investment returns. By doing so, you can identify areas that need improvement and make adjustments as needed to stay on track.

Monitoring progress also helps you celebrate small milestones, which is crucial to staying motivated and encouraged. For instance, treating yourself to a nice dinner or a weekend getaway after reaching a savings goal can be a great way to acknowledge your hard work. This positive reinforcement can help you stay focused on your long-term financial objectives.

Some ways to track progress include:

- Using budgeting apps like Mint or Personal Capital to monitor expenses and income

- Setting up automatic investment transfers to ensure consistent investing

- Creating a spreadsheet to track savings and investment growth over time

By leveraging these tools, you can easily monitor your progress and make data-driven decisions to optimize your financial strategy.

Continuous education is also vital to achieving financial success. This can involve reading personal finance books, attending webinars, or following reputable finance blogs to stay up-to-date on the latest investing strategies and trends. By expanding your knowledge, you can refine your approach and make more informed decisions about your financial future.

Staying motivated and educated can also involve joining online communities or forums, where you can connect with like-minded individuals and learn from their experiences. This can provide a sense of accountability and support, helping you stay committed to your financial goals. By combining regular progress tracking, celebration of milestones, and ongoing education, you can set yourself up for long-term financial success.

Frequently Asked Questions (FAQ)

Do I need a side hustle to start building wealth?

Starting to build wealth can seem daunting, especially for recent graduates or those new to personal finance. However, it's essential to understand that creating a solid foundation is more important than rushing into a side hustle. By focusing on a well-structured budget and investment strategy, you can set yourself up for long-term financial success.

A solid budget allows you to track your income and expenses, making it easier to identify areas where you can cut back and allocate funds towards savings and investments. For instance, you can use the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment. This simple rule can help you prioritize your financial goals and make progress towards building wealth.

When it comes to investments, it's crucial to have a clear strategy in place. Consider the following:

- Start with a low-cost index fund or ETF to diversify your portfolio

- Take advantage of tax-advantaged accounts such as a Roth IRA or 401(k)

- Automate your investments to ensure consistent progress towards your goals

By following these steps, you can create a stable financial foundation that will serve as a launching pad for your wealth-building journey.

It's also important to remember that building wealth is a marathon, not a sprint. It's not about getting rich quickly, but rather about making consistent progress over time. By prioritizing your budget and investment strategy, you can silently build wealth without necessarily needing a side hustle. As your wealth grows, you can then consider exploring additional income streams to further accelerate your financial progress.

How long does it take to see significant results from the wealth formula?

When it comes to building wealth, patience is key. The wealth formula, which involves a combination of smart investing, saving, and budgeting, can take time to yield significant results. By sticking to your plan and consistently making progress, you can set yourself up for long-term financial success.

The amount of time it takes to see substantial results from the wealth formula can vary greatly from person to person. Factors such as starting income, debt, and investment returns all play a role in determining the pace of wealth accumulation. However, as a general rule, consistent effort over 5-10 years can lead to substantial wealth accumulation.

Some examples of how the wealth formula can play out in real life include:

- Starting a retirement account in your 20s and contributing to it regularly, with the goal of having a sizable nest egg by the time you reach your 50s

- Investing in a diversified portfolio of stocks and bonds, and reinvesting dividends to take advantage of compound interest

- Pay off high-interest debt, such as credit card balances, and using the money saved to invest in a tax-advantaged account

By following these strategies and staying committed to your financial plan, you can make steady progress towards your wealth-building goals.

It's also important to remember that building wealth is a marathon, not a sprint. There will be ups and downs along the way, and it's essential to stay focused on your long-term goals. With consistent effort and a well-thought-out plan, you can overcome obstacles and achieve significant results from the wealth formula over time. By celebrating small victories along the way and making adjustments as needed, you can stay motivated and on track to achieving your financial objectives.

What if I have high-interest debt, where do I start?

When dealing with high-interest debt, it's essential to take a step back and assess your financial situation. Start by gathering all your financial documents, including credit card statements, loan papers, and bills, to get a clear picture of your debt. This will help you understand the total amount you owe and the interest rates associated with each debt.

Prioritizing debt repayment is crucial, and building a budget that allocates funds towards debt and savings is the first step. A budget will help you track your income and expenses, making it easier to identify areas where you can cut back and allocate more funds towards debt repayment. For example, you can use the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment.

To create a debt repayment plan, consider the following steps:

- Make a list of all your debts, including the balance, interest rate, and minimum payment

- Sort your debts by interest rate, focusing on the ones with the highest rates first

- Pay the minimum on all debts except the one with the highest interest rate, which you'll pay as much as possible towards

By following these steps and sticking to your budget, you can make significant progress in paying off your high-interest debt and improving your financial health.

In addition to debt repayment, building an emergency fund is also crucial to avoid going further into debt when unexpected expenses arise. Aim to save 3-6 months' worth of living expenses in a easily accessible savings account, which will provide a cushion in case of financial emergencies. By prioritizing debt repayment and building a budget that allocates funds towards debt and savings, you'll be well on your way to achieving financial stability and security.