Getting your finances in order can be a daunting task, but with a clear plan and daily commitment, you can achieve financial stability and success. Our 31-day challenge is designed to help you transform your financial life with actionable daily tasks and strategies. By dedicating just a few minutes each day to your finances, you can develop healthy habits and make progress towards your goals.

The challenge is divided into daily tasks that cover a range of topics, from budgeting and saving to investing and managing debt. Each day, you'll receive a new task to complete, such as tracking your expenses or researching ways to reduce your bills. For example, on day one, you might start by gathering all of your financial documents, including bank statements and credit card bills, to get a clear picture of your current financial situation.

To give you an idea of what to expect, here are some of the topics we'll cover during the challenge:

- Creating a budget that works for you

- Building an emergency fund to cover unexpected expenses

- Paying off high-interest debt and managing credit card balances

- Investing in your future, whether through a retirement account or other investments

- Reducing expenses and finding ways to save money

By following along with the challenge and completing each daily task, you'll be well on your way to taking control of your finances and achieving your long-term goals. Whether you're just starting out or looking to get back on track, our 31-day challenge is the perfect way to make a positive impact on your financial life.

Understanding Your Financial Health

To get a better understanding of your financial health, start by tracking your income and expenses for a week. This will help you identify areas where you can cut back and make adjustments to achieve a more balanced budget. For example, you might be surprised to find that you're spending a significant amount on dining out or subscription services.

Taking the time to calculate your net worth is also essential, as it provides a clear picture of your overall financial situation. This can be done by subtracting your liabilities, such as student loans or credit card debt, from your assets, like savings or investments. By doing so, you'll be able to see where you stand and make informed decisions about your financial future.

Setting specific financial goals is crucial to improving your financial health. To do this, consider using the SMART goal framework, which involves making sure your objectives are:

- Specific: clearly defined and easy to understand

- Measurable: quantifiable, so you can track progress

- Achievable: realistic and attainable based on your resources

- Relevant: aligned with your values and priorities

- Time-bound: having a specific deadline or timeframe

This will help you stay focused and motivated as you work towards achieving financial stability and success.

By following these steps, you'll be well on your way to gaining a deeper understanding of your financial health and making positive changes to improve it. Remember, small adjustments can add up over time, so don't be discouraged if you don't see immediate results. With patience, persistence, and the right strategies, you can take control of your finances and build a brighter future.

Budgeting and Saving Strategies

Creating a budget is the first step towards taking control of your finances. To make the most of your money, it's essential to allocate your income wisely. Implementing the 50/30/20 rule is a great starting point, where 50% of your income goes towards necessities like rent, utilities, and groceries.

The 50/30/20 rule also allocates 30% for discretionary spending, such as entertainment, hobbies, and travel, and 20% for saving and debt repayment. This rule helps you strike a balance between enjoying your life now and securing your financial future. For example, if you earn $4,000 per month, you would allocate $2,000 towards necessities, $1,200 towards discretionary spending, and $800 towards saving and debt repayment.

To categorize and control your expenses, consider using the envelope system, where you divide your expenses into categories and allocate a specific amount for each category. You can use physical envelopes or digital tools to make it easier. Some popular categories include:

- housing and utilities

- food and groceries

- transportation

- entertainment and leisure

By using the envelope system, you can ensure that you're not overspending in any one category and make adjustments as needed.

Automating your savings is another effective way to build wealth over time. You can set up direct deposit or use mobile banking apps to transfer a fixed amount regularly into your savings or investment accounts. This way, you'll ensure that you're prioritizing your savings and debt repayment without having to think about it. Many banks and financial institutions also offer automated savings options, such as rounding up your purchases to the nearest dollar or transferring a fixed amount daily.

Managing Debt and Building Credit

When it comes to managing debt, it's essential to have a solid plan in place. Prioritizing high-interest debt, such as credit card balances, for aggressive payoff can save you a significant amount of money in interest charges over time. For instance, if you have a credit card balance of $2,000 with an interest rate of 20%, you could end up paying over $400 in interest alone if you only make the minimum payments.

To tackle high-interest debt, consider consolidating it into a lower-interest loan or balance transfer credit card. This can simplify your payments and reduce the amount of interest you owe. By consolidating your debt, you can free up more money in your budget to put towards your debt repayment.

Here are some tips to keep in mind when consolidating debt:

- Look for a loan or credit card with an interest rate significantly lower than your current debt

- Make sure you understand the terms and conditions of the new loan or credit card, including any fees or penalties

- Create a plan to pay off the consolidated debt as quickly as possible to avoid accumulating more interest

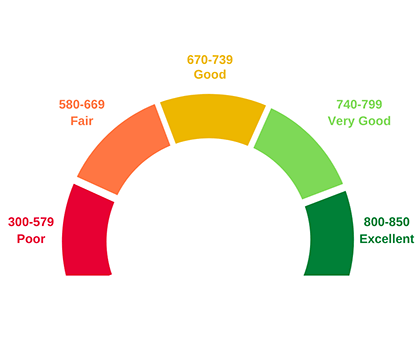

Monitoring your credit report and working on improving your credit score are also crucial steps in managing debt. You can request a free credit report from the three major credit reporting agencies once a year, which can help you identify areas for improvement. By paying your bills on time, reducing your debt, and avoiding new credit inquiries, you can work towards a healthier credit score.

Regularly reviewing your credit report can also help you catch any errors or inaccuracies that may be negatively affecting your credit score. You can dispute these errors and work with the credit reporting agency to resolve the issue. Additionally, making on-time payments and keeping credit utilization low can help you build a positive credit history over time.

Investing and Growing Your Wealth

Investing can seem daunting, but it's a crucial step in growing your wealth over time. For beginners, exploring low-cost index funds or ETFs is a great place to start, as they offer broad diversification and typically have lower fees compared to actively managed funds. By investing in index funds or ETFs, you can gain exposure to a wide range of assets, such as stocks or bonds, with minimal effort.

When it comes to investing for retirement, consider contributing to a tax-advantaged account, such as a Roth IRA. This type of account allows you to contribute after-tax dollars, which can then grow tax-free and be withdrawn tax-free in retirement. For example, if you contribute $5,000 to a Roth IRA each year, you can potentially accumulate a significant nest egg over the course of several decades.

To minimize risk and maximize returns, it's essential to learn about diversification and asset allocation. This involves spreading your investments across different asset classes, such as:

- Stocks, which offer potential for long-term growth

- Bonds, which provide relatively stable income and lower risk

- Real estate, which can offer a tangible asset and rental income

By allocating your investments across these different asset classes, you can reduce your exposure to any one particular market or sector, and increase the potential for long-term growth.

As you begin investing, it's also important to keep costs in mind and avoid unnecessary fees. Look for low-cost index funds or ETFs with expense ratios below 0.20%, and consider working with a financial advisor or using online investment platforms to streamline your investment process. By taking a thoughtful and informed approach to investing, you can set yourself up for long-term financial success and achieve your goals.

Side Hustles and Increasing Income

To get started with side hustles, it's essential to identify your skills and passions, as these can help you find a profitable opportunity. Consider what you're good at and what you enjoy doing in your free time, as this can give you an edge in the market. For instance, if you're skilled in writing, you could offer your services as a freelance writer or editor.

Exploring online opportunities can also be a great way to increase your income, with many platforms offering freelancing or selling products as viable options. Websites like Upwork, Fiverr, and Etsy provide a range of opportunities, from writing and design to crafting and selling handmade products. You can also use social media platforms like Instagram or Pinterest to showcase your products and reach a wider audience.

Some popular side hustles include:

- Freelance writing or editing, which can be done remotely and offers flexible hours

- Selling products online, such as through an e-commerce website or social media platforms

- Participating in the gig economy, through companies like Uber or TaskRabbit

These side hustles can help you earn extra money and increase your income, but it's crucial to set realistic income goals and track your progress. Start by setting achievable targets, such as earning an extra $100 per week, and use tools like spreadsheets or budgeting apps to monitor your progress.

Tracking your progress is vital to ensuring you're on the right path and making adjustments as needed. Regularly review your income and expenses to see where you can improve, and make changes to your side hustle strategy accordingly. By doing so, you'll be able to increase your income and achieve your financial goals over time.

Frequently Asked Questions (FAQ)

What is the best way to stick to the 31-day wealth challenge?

To successfully complete the 31-day wealth challenge, it's essential to establish a routine that works for you. Creating a schedule and setting reminders can help you stay on track and motivated throughout the challenge. By doing so, you'll be able to make consistent progress and develop healthy financial habits.

Sticking to your schedule can be as simple as setting a daily reminder on your phone or putting a note on your fridge. This will help you remember to complete your daily tasks, such as tracking your expenses or saving a certain amount of money. Consistency is key when it comes to building wealth, and a schedule can help you stay focused.

Some tips to help you stay on track include:

- Breaking down larger tasks into smaller, manageable chunks

- Creating a budget and tracking your progress

- Finding a accountability partner to support and motivate you

These strategies can help you overcome obstacles and stay committed to your financial goals. By prioritizing your tasks and staying organized, you'll be able to make the most of the 31-day wealth challenge.

As you progress through the challenge, be sure to review and adjust your schedule as needed. Life can be unpredictable, and unexpected expenses or setbacks may arise. By being flexible and adapting to changes, you can ensure that you stay on track and continue to make progress towards your financial goals.

How do I know which debt to pay off first?

When it comes to paying off debt, it can be overwhelming to decide where to start. A good rule of thumb is to prioritize high-interest debt, such as credit card balances, to save money on interest payments over time. By focusing on these debts first, you can make a significant impact on your overall debt burden.

To get started, take a close look at your debts and make a list of the balances, interest rates, and minimum monthly payments. This will help you understand which debts are costing you the most in interest. For example, if you have a credit card with a balance of $2,000 and an interest rate of 18%, you'll want to prioritize paying that off before a student loan with a balance of $10,000 and an interest rate of 4%.

Here are some steps to follow:

- Make a list of all your debts, including credit cards, loans, and mortgages

- Sort the list by interest rate, with the highest rate first

- Consider consolidating multiple debts into a single loan with a lower interest rate

By following these steps, you can create a plan to tackle your debt and start saving money on interest payments.

In addition to prioritizing high-interest debt, it's also important to make timely payments and pay more than the minimum payment whenever possible. This will help you pay off your debts faster and avoid accumulating more interest over time. For instance, if you have a credit card with a minimum payment of $50, try to pay $100 or more each month to make a bigger dent in the balance.

What are some easy ways to start investing with little money?

Getting started with investing can seem daunting, especially when you have limited funds. However, there are several ways to begin investing with little money, and it's easier than you think. Consider micro-investing apps or beginner-friendly brokerage accounts with low or no minimum balance requirements, which allow you to start investing with as little as $1.

Micro-investing apps are a great option for those new to investing, as they offer a user-friendly interface and often have low or no fees. These apps typically allow you to invest small amounts of money into a diversified portfolio, making it easy to get started. For example, apps like Acorns or Stash allow you to invest spare change or small amounts of money into a variety of assets.

Some popular beginner-friendly brokerage accounts with low or no minimum balance requirements include:

- Robinhood, which offers commission-free trading and no minimum balance requirements

- Fidelity, which has no account minimums or fees for many of its accounts

- Charles Schwab, which offers a range of accounts with low or no minimum balance requirements

These accounts make it easy to start investing with little money, and many of them also offer educational resources and tools to help you get started.

When choosing a micro-investing app or brokerage account, be sure to consider the fees associated with the account, as well as any investment options or tools that may be available. It's also a good idea to read reviews and do your research before opening an account, to ensure that you find the best fit for your needs and goals. By taking the time to explore your options and choose a reputable app or brokerage, you can start investing with confidence, even with limited funds.