As a young adult, managing student loan debt can be overwhelming, but it's essential to start with the basics. Understanding student loan interest rates is crucial for creating a plan to pay off your debt effectively. By grasping how interest rates work, you can make informed decisions about your loans and avoid unnecessary financial burdens.

When it comes to student loans, interest rates can significantly impact the total amount you repay. For instance, a loan with a 4% interest rate will result in less interest paid over time compared to a loan with a 7% interest rate. To put this into perspective, consider a $30,000 loan with a 4% interest rate, which would result in approximately $5,000 in interest paid over 10 years.

Here are some key points to consider when understanding student loan interest rates:

- Fixed interest rates remain the same throughout the life of the loan

- Variable interest rates can change over time, often based on market conditions

- Federal student loans typically have fixed interest rates, while private loans may have variable rates

By understanding these concepts, you can begin to develop a strategy for managing your student loan debt and making progress towards financial freedom. Taking the time to learn about interest rates and how they affect your loans can save you money and reduce stress in the long run.

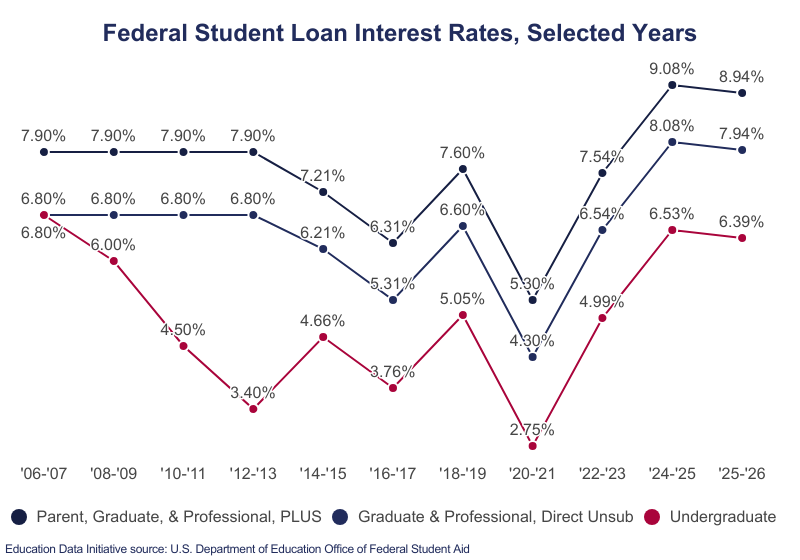

Federal Student Loan Interest Rates 2025

As a student, understanding federal student loan interest rates is crucial for managing your debt. The current federal student loan interest rates for undergraduate students are set at 4.53% for subsidized and unsubsidized loans, while graduate students face interest rates of 6.54% for unsubsidized loans. These rates apply to loans disbursed between July 1, 2024, and June 30, 2025.

When it comes to federal student loans, there are two main types: subsidized and unsubsidized.

- Subsidized loans are available to undergraduate students who demonstrate financial need, and the government pays the interest while the student is in school.

- Unsubsidized loans, on the other hand, are available to both undergraduate and graduate students, and the borrower is responsible for paying the interest from the time the loan is disbursed.

This difference can significantly impact the total amount borrowed and the monthly payments.

The federal student loan interest rates can substantially affect monthly payments. For instance, if you borrow $10,000 in unsubsidized loans at 4.53% interest, your monthly payment could be around $106 over a 10-year repayment period. However, if the interest rate were 6.54%, your monthly payment would increase to around $115. Understanding these rates and how they impact your payments can help you make informed decisions about your loans.

To give you a better idea, here are some examples of how federal student loan interest rates can affect monthly payments:

- A $20,000 loan at 4.53% interest could result in monthly payments of around $213 over 10 years.

- A $30,000 loan at 6.54% interest could result in monthly payments of around $344 over 10 years.

By considering these examples and understanding the current federal student loan interest rates, you can create a more effective plan for managing your debt and achieving financial stability.

Private Student Loan Interest Rates 2025

When exploring private student loan options, understanding the current interest rates is crucial. Private student loan interest rates vary among lenders, and comparing them can help you make an informed decision. For instance, lenders like Sallie Mae and Discover offer competitive interest rates, with some rates as low as 3.50% APR.

To make the most of private student loans, it's essential to weigh the pros and cons against federal student loan options. One significant advantage of private student loans is that they often offer more flexible repayment terms. However, federal student loans typically provide more borrower protections, such as income-driven repayment plans and loan forgiveness options.

Here are some key points to consider when choosing between private and federal student loans:

- Interest rates: Private student loans often have higher interest rates than federal student loans, but some lenders offer competitive rates with good credit.

- Repayment terms: Private student loans may offer more flexible repayment terms, including longer repayment periods and temporary hardship programs.

- Borrower protections: Federal student loans provide more robust borrower protections, including loan forgiveness and income-driven repayment options.

Shopping for private student loans with competitive rates requires some research and planning. Start by checking your credit score, as a good credit score can help you qualify for lower interest rates. You can also consider applying with a creditworthy cosigner to improve your chances of approval and secure a better interest rate.

Some popular lenders offering competitive private student loan interest rates include College Ave, SoFi, and Earnest. When comparing rates, be sure to review the terms and conditions, including any fees associated with the loan. By doing your research and comparing rates, you can find a private student loan that meets your needs and helps you achieve your educational goals.

To get the best possible interest rate, consider the following tips:

- Apply with a creditworthy cosigner to improve your chances of approval and secure a better interest rate.

- Check for any available discounts, such as autopay discounts or loyalty rewards.

- Review the loan terms and conditions carefully, including any fees associated with the loan.

By understanding private student loan interest rates and carefully evaluating your options, you can make an informed decision and find a loan that helps you achieve your educational goals without breaking the bank. Remember to always review the terms and conditions carefully and consider your repayment options before committing to a loan.

Strategies to Reduce Student Loan Interest Rates

Income-driven repayment plans can be a game-changer for students struggling to pay off their loans. These plans adjust monthly payments based on income and family size, making it more manageable to stay on top of debt. For example, the Income-Based Repayment (IBR) plan can lower monthly payments to 10% or 15% of discretionary income.

One of the main benefits of income-driven repayment plans is the potential to reduce the amount of interest paid over the life of the loan. By lowering monthly payments, borrowers can avoid defaulting on their loans and accruing additional interest charges. This can be especially helpful for students who are just starting their careers and may not have a high income.

Refinancing student loans is another option to consider for reducing interest rates. This involves taking out a new loan with a lower interest rate to pay off existing loans. The pros of refinancing include potentially saving thousands of dollars in interest over the life of the loan, as well as simplifying payments by consolidating multiple loans into one.

Some things to consider when refinancing include:

- Checking credit scores to ensure eligibility for better interest rates

- Comparing rates and terms from multiple lenders to find the best deal

- Understanding the repayment terms, including the length of the loan and any fees associated with refinancing

However, refinancing may not be the best option for everyone, as it can involve giving up certain benefits like income-driven repayment plans or loan forgiveness programs. It's essential to weigh the pros and cons carefully and consider individual financial circumstances before making a decision. Borrowers should also be aware that refinancing federal loans can result in losing access to federal benefits and protections.

Negotiating with lenders can also be an effective way to reduce interest rates. This may involve calling the lender to discuss options or providing documentation to support a request for a lower rate. Tips for negotiating with lenders include:

- Being proactive and reaching out to lenders before falling behind on payments

- Providing a clear explanation of financial hardship or changes in income

- Asking about available options, such as temporary hardship programs or interest rate reductions

By being informed and proactive, students can take control of their debt and work towards reducing their student loan interest rates. Whether through income-driven repayment plans, refinancing, or negotiating with lenders, there are options available to help manage debt and achieve financial stability.

Budgeting and Repayment Plans for Student Loans

Creating a budget that accounts for student loan payments is crucial for managing your finances effectively. To start, gather all your financial documents, including your student loan statements, pay stubs, and bank accounts. This will give you a clear picture of your income and expenses.

Begin by tracking your income and expenses to see where your money is going. Make a list of all your necessary expenses, such as rent, utilities, and groceries, and then allocate funds for discretionary spending. A good rule of thumb is to allocate 50-30-20: 50% for necessary expenses, 30% for discretionary spending, and 20% for saving and debt repayment.

When it comes to paying off student loans, there are two popular methods: the snowball method and the avalanche method. The snowball method involves paying off loans with the smallest balances first, while the avalanche method involves paying off loans with the highest interest rates first. For example, if you have two loans, one with a balance of $1,000 and an interest rate of 4%, and another with a balance of $10,000 and an interest rate of 6%, the avalanche method would prioritize the loan with the 6% interest rate.

To implement either method, consider the following steps:

- Make a list of all your student loans, including the balance, interest rate, and minimum payment for each loan

- Sort the loans by balance or interest rate, depending on the method you choose

- Prioritize the loan with the smallest balance or highest interest rate, and make extra payments towards that loan while still making the minimum payments on the other loans

There are many resources available to help you create a budget and repayment plan for your student loans. You can use online tools, such as student loan repayment calculators, to determine how much you need to pay each month to pay off your loans within a certain timeframe. Some popular resources include the Federal Student Aid website, which offers a range of tools and calculators, and websites like NerdWallet and Credit Karma, which provide personalized budgeting and repayment plans.

For example, you can use a student loan repayment calculator to determine how much you need to pay each month to pay off a $30,000 loan with an interest rate of 5% within 10 years. By plugging in the numbers, you can see that you would need to pay approximately $318 per month to pay off the loan within the desired timeframe. By using these tools and creating a budget that accounts for your student loan payments, you can take control of your finances and make progress towards becoming debt-free.

Conclusion and Next Steps

As we wrap up our discussion on student loan management, it's essential to summarize the key takeaways from our article. We've covered the importance of understanding your loan terms, creating a budget, and exploring repayment options. By implementing these strategies, you can take control of your student loan debt and make informed decisions about your financial future.

To further enhance your knowledge on student loan management, we recommend exploring additional resources such as the Federal Student Aid website, which offers a wealth of information on loan repayment plans and forgiveness programs. You can also visit our blog for more articles and tips on managing your debt, including examples of successful repayment strategies and testimonials from students who have overcome their debt.

Some additional resources to consider include:

- Federal Student Aid website

- National Foundation for Credit Counseling

- Student loan repayment calculators

These resources can provide you with the tools and guidance you need to make informed decisions about your student loan debt and develop a personalized repayment plan.

Now that you've learned more about managing your student loan debt, it's time to take action. Start by reviewing your loan documents, calculating your monthly payments, and exploring repayment options that work for you. By taking these steps, you can begin to pay off your debt and achieve financial stability. Visit our website for a free student loan repayment worksheet and start managing your debt today.

Frequently Asked Questions (FAQ)

How do federal student loan interest rates affect my monthly payments?

When it comes to federal student loans, understanding the interest rate is crucial. Federal student loan interest rates can significantly impact monthly payments, with higher rates resulting in more expensive monthly payments. For instance, a 1% increase in interest rate can add up to hundreds of dollars over the life of the loan.

To put this into perspective, let's consider an example. If you have a $30,000 federal student loan with a 4% interest rate, your monthly payment might be around $311. However, if the interest rate increases to 5%, your monthly payment could jump to $322. This may not seem like a lot, but it can add up over time.

Here are some key factors to consider when it comes to federal student loan interest rates and monthly payments:

- Interest rates can vary depending on the type of loan and the borrower's credit score

- Higher interest rates can lead to larger monthly payments and a longer repayment period

- Consolidating loans or refinancing to a lower interest rate can help reduce monthly payments

It's essential to review your loan terms and interest rate to determine the best course of action for managing your debt.

In general, it's a good idea to explore options for reducing your monthly payments, such as income-driven repayment plans or loan forgiveness programs. By understanding how federal student loan interest rates affect your monthly payments, you can make informed decisions about your financial situation and create a plan to pay off your debt efficiently. Additionally, you can use online tools and calculators to estimate your monthly payments and compare different interest rates and repayment scenarios.

Can I refinance my student loans to get a better interest rate?

When considering refinancing your student loans, it's essential to understand the process and its potential benefits. Refinancing involves replacing your existing loan with a new one, often with a lower interest rate, which can help you save money on interest payments over time. For instance, if you have a loan with a 6% interest rate, refinancing to a 4% interest rate can make a significant difference in your monthly payments.

To determine if refinancing is right for you, weigh the pros and cons of this decision. Some benefits of refinancing include lower monthly payments, reduced interest rates, and the possibility of combining multiple loans into one. However, it's crucial to consider the potential drawbacks, such as losing federal loan benefits or facing stricter repayment terms.

Here are some key factors to consider when deciding whether to refinance your student loans:

- Check your credit score, as a good credit score can help you qualify for better interest rates

- Research and compare rates from different lenders to find the best option for your situation

- Consider the repayment terms, including the loan duration and any potential fees

By carefully evaluating these factors, you can make an informed decision about whether refinancing your student loans is the right choice for you.

Refinancing can be a great way to simplify your finances and reduce your debt burden. For example, if you have multiple loans with different interest rates and repayment terms, refinancing can help you consolidate them into a single loan with a lower interest rate and a more manageable repayment schedule. This can make it easier to stay on top of your payments and avoid missing deadlines.

Before making a decision, it's also important to consider your financial goals and priorities. If you're struggling to make payments or want to pay off your loans quickly, refinancing might be a good option. On the other hand, if you're concerned about losing federal loan benefits or have a stable financial situation, you might want to explore other options, such as income-driven repayment plans or loan forgiveness programs.

What are some strategies for reducing student loan interest rates?

Reducing student loan interest rates can save you a significant amount of money over the life of your loan. One approach to consider is income-driven repayment plans, which can lower your monthly payments and, in some cases, reduce your interest rate. For example, the Income-Based Repayment (IBR) plan and the Pay As You Earn (PAYE) plan are two popular options that can help make your payments more manageable.

Another strategy for reducing student loan interest rates is refinancing, which involves taking out a new loan with a lower interest rate to pay off your existing loan. This can be a good option if you have a good credit score and can qualify for a lower interest rate. When refinancing, it's essential to carefully review the terms and conditions of the new loan to ensure it's a better deal than your current loan.

Some lenders may also be willing to negotiate with you to reduce your interest rate, especially if you've made consistent payments on time. You can try contacting your lender to see if they can offer any discounts or promotions that can help lower your interest rate. Here are some additional strategies to consider:

- Consolidating multiple loans into one loan with a lower interest rate

- Using a co-signer with good credit to qualify for a lower interest rate

- Making extra payments or paying more than the minimum payment each month to pay off the loan faster and reduce the amount of interest paid over time

It's crucial to do your research and explore all the options available to you before making any decisions. You can start by reviewing your loan documents, checking your credit score, and contacting your lender to discuss possible alternatives. By taking proactive steps to reduce your student loan interest rate, you can save money and make your debt more manageable.