As of September 2025, student loan rates are undergoing significant changes that will affect borrowers in various ways. These changes can be a bit overwhelming, especially for those who are already managing their debt. It's essential to understand the updates and how they will impact your financial situation.

The new student loan rates will influence the amount of interest borrowers pay over the life of their loan, which can add up quickly. For example, a borrower with a $30,000 loan at 4% interest will pay more in interest than someone with the same loan amount at 3% interest. This difference in interest rates can save or cost the borrower thousands of dollars.

Some key points to consider about the changes in student loan rates include:

- Increased interest rates may lead to higher monthly payments for borrowers

- Variable interest rates may fluctuate over time, affecting the total cost of the loan

- Borrowers may need to reassess their budget and repayment strategy to accommodate the new rates

By understanding these changes and their implications, borrowers can make informed decisions about their student loans and develop a plan to manage their debt effectively.

Borrowers should review their loan terms and consider options such as income-driven repayment plans or loan consolidation to minimize the impact of the new rates. Additionally, creating a budget and prioritizing debt repayment can help borrowers stay on track and achieve their financial goals.

Understanding the New Interest Rates

For the 2025-2026 academic year, new student loan interest rates have been announced, and it's essential to understand how they impact your borrowing costs. The new rates are slightly higher compared to the previous year, with undergraduate loans having an interest rate of 5.50% and graduate loans at 6.54%. This change can significantly affect your monthly loan payments, so it's crucial to review your loan terms.

The factors that contribute to these rate changes are largely driven by economic conditions and federal policies. Economic conditions, such as inflation and unemployment rates, play a significant role in determining interest rates. For instance, when the economy is growing, and inflation is rising, interest rates tend to increase to keep pace with the growth.

Some key factors that influence interest rate changes include:

- Federal Reserve monetary policies

- Inflation rates

- Unemployment rates

- Government debt and budget deficits

These factors can either increase or decrease interest rates, depending on the overall economic situation.

To illustrate how these rate changes can affect monthly loan payments, let's consider an example. Suppose you have a $30,000 student loan with a 10-year repayment term, and the interest rate increases from 4.53% to 5.50%. Your monthly payment could rise from $311 to $336, resulting in an additional $300 per year in interest payments. Understanding these changes can help you plan and adjust your budget accordingly.

It's essential to review your loan terms and consider the impact of these rate changes on your monthly payments. You can use online loan calculators to estimate your new monthly payments and explore options for reducing your borrowing costs, such as income-driven repayment plans or loan consolidation. By staying informed and taking proactive steps, you can manage your student loan debt effectively and achieve financial stability.

Strategies for Managing Your Debt

When it comes to managing debt, creating a budget is essential. This budget should account for increased loan payments due to higher interest rates, ensuring you're prepared for the extra financial burden. By doing so, you can avoid missed payments and potential damage to your credit score.

To make debt management more manageable, consider income-driven repayment plans. These plans adjust your monthly payments based on your income and family size, making it easier to stay on top of your loans. For example, if you're experiencing a period of financial hardship, an income-driven repayment plan can help reduce your monthly payments and prevent default.

Some popular income-driven repayment plans include:

- Income-Based Repayment (IBR) plan, which caps monthly payments at 10% or 15% of your discretionary income

- Pay As You Earn (PAYE) plan, which limits monthly payments to 10% of your discretionary income

- Revised Pay As You Earn (REPAYE) plan, which also caps monthly payments at 10% or 5% of your discretionary income, depending on the type of loan

These plans can be a lifesaver for borrowers struggling to make ends meet, and it's essential to explore your options to find the best fit for your financial situation.

In addition to income-driven repayment plans, taking on a side hustle or part-time job can be an excellent way to pay off your loans more efficiently. Consider freelancing, tutoring, or participating in the gig economy to increase your income and put more money towards your debt. For instance, you could use the extra money earned from a part-time job to make extra payments on your loans, reducing the principal balance and saving on interest over time.

By combining a solid budget, an income-driven repayment plan, and a side hustle or part-time job, you can create a powerful debt management strategy. Remember to review and adjust your budget regularly to ensure you're on track to meet your financial goals, and don't hesitate to seek help if you need guidance on managing your debt. With the right approach, you can overcome debt and achieve financial stability.

Investing for the Future While Paying Off Loans

Paying off high-interest debt, such as student loans, can be a significant financial burden for young adults. However, this does not mean that investing for the future should be put on hold. In fact, investing while paying off debt can be a great way to build wealth and secure your financial future.

When it comes to investing while paying off high-interest debt, there are potential benefits and risks to consider. On the one hand, investing can provide a potential long-term return on your money, which can help you build wealth over time. On the other hand, investing always carries some level of risk, and there is a chance that you could lose some or all of your investment.

To get started with investing while paying off debt, it's essential to explore low-risk investment strategies. Some examples of low-risk investments include:

- High-yield savings accounts, which provide a low but relatively safe return on your money

- Index funds or ETFs, which track a specific market index and tend to be less volatile than individual stocks

- Bonds, which provide a fixed return on your investment and are generally considered to be low-risk

These types of investments can be a good starting point for young adults with student loan debt, as they provide a relatively safe way to grow your money over time.

Building an emergency fund is also crucial when it comes to investing while paying off debt. This is because unexpected expenses can arise at any time, and having a cushion of savings can help you avoid going further into debt. Aim to save 3-6 months' worth of living expenses in an easily accessible savings account, and make sure to contribute to your emergency fund regularly.

In terms of practical tips, consider setting up a separate savings account specifically for your emergency fund, and set up automatic transfers from your checking account to make saving easier and less prone to being neglected. Additionally, try to avoid dipping into your emergency fund for non-essential expenses, and focus on using it only for true emergencies.

By following these tips and exploring low-risk investment strategies, you can make progress on paying off your debt while also building a more secure financial future. Remember to always prioritize your debt repayment and emergency fund savings, and don't be afraid to seek out professional advice if you're unsure about how to get started.

Navigating Loan Forgiveness and Consolidation

When it comes to managing student loans, many borrowers are unaware of the various options available to them. One such option is loan forgiveness, which can be a game-changer for those struggling to make payments. For instance, the Public Service Loan Forgiveness (PSLF) program is designed for borrowers working in public service, such as teachers, nurses, or government employees.

The PSLF program forgives the remaining balance on a borrower's loan after 120 qualifying payments. To be eligible, borrowers must be working full-time in a qualifying public service job and have a Direct Loan. Other types of loan forgiveness programs include Teacher Loan Forgiveness and Perkins Loan Cancellation.

Loan consolidation is another option for borrowers to simplify their payments. This process involves combining multiple loans into one loan with a single interest rate and payment due date. The benefits of consolidating loans include lower monthly payments and the potential to qualify for income-driven repayment plans.

Some key things to consider when consolidating loans include:

- Interest rates: Consolidating loans may result in a higher interest rate, which can increase the total cost of the loan over time.

- Loan terms: Borrowers may be able to extend their loan term, which can lower monthly payments but increase the total interest paid.

- Loss of benefits: Consolidating certain types of loans, such as Perkins Loans, may result in the loss of benefits like loan forgiveness or cancellation.

To stay organized and keep track of loan forgiveness and consolidation applications, borrowers can create a spreadsheet or use a loan tracking tool. It's also essential to keep records of all correspondence with loan servicers, including emails, letters, and phone calls. By staying on top of the process, borrowers can avoid potential pitfalls and ensure they're taking advantage of the benefits available to them.

For borrowers who are unsure about the best course of action, it's a good idea to consult with a financial advisor or student loan expert. They can help borrowers weigh the pros and cons of different options and create a personalized plan for managing their debt. By taking a proactive approach, borrowers can simplify their payments and make progress towards becoming debt-free.

Maintaining Financial Health

Monitoring your credit scores and reports is crucial, especially when managing student loan debt. By keeping a close eye on your credit, you can catch any errors or discrepancies that may be affecting your score. For instance, you can request a free credit report from the three major credit reporting agencies (Experian, TransUnion, and Equifax) once a year to review your credit history.

When it comes to managing your finances, it's essential to avoid lifestyle inflation, which occurs when you increase your spending as your income rises. To avoid this trap, prioritize your needs over your wants, and allocate your money accordingly. For example, instead of buying a new car, consider using public transportation or carpooling to save money.

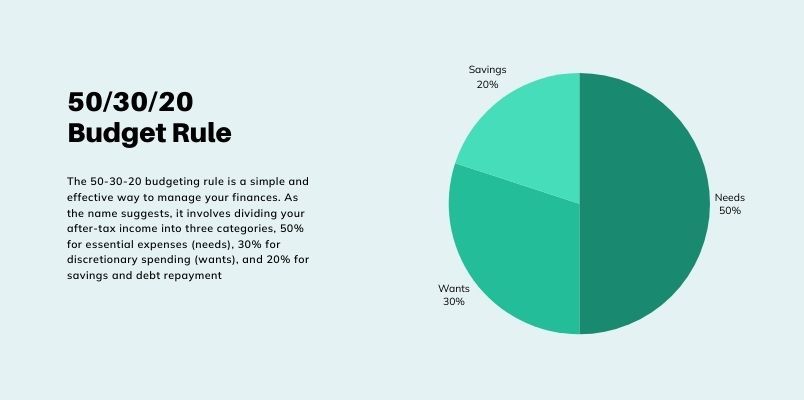

To prioritize your spending, make a list of your expenses using the 50/30/20 rule:

- 50% of your income goes towards necessary expenses like rent, utilities, and groceries

- 30% towards discretionary spending like entertainment and hobbies

- 20% towards saving and debt repayment

This simple rule can help you allocate your money effectively and avoid overspending.

Financial wellness is closely tied to overall well-being, as it can reduce stress and anxiety related to money matters. By taking control of your finances, you can achieve a sense of security and freedom, which can have a positive impact on your mental and physical health. For example, having a emergency fund in place can give you peace of mind and help you avoid going into debt when unexpected expenses arise.

In addition to monitoring your credit and prioritizing your spending, it's essential to cultivate healthy financial habits, such as saving regularly and avoiding high-interest debt. By doing so, you can achieve financial stability and improve your overall quality of life. Consider setting financial goals, like paying off student loans or building an emergency fund, and create a plan to achieve them.

Frequently Asked Questions (FAQ)

How do the new student loan interest rates affect my existing loans?

When it comes to understanding how new student loan interest rates affect your existing loans, it's essential to consider the type of loan you have and when it was issued. This is because some loans have fixed rates, which means the interest rate remains the same throughout the loan period, while others have variable rates that can change over time. For instance, if you have a federal student loan with a fixed rate, the new interest rates may not impact your existing loan.

The impact of new student loan interest rates on existing loans also depends on the lender and the specific loan terms. If you have a private student loan with a variable rate, the lender may adjust the interest rate based on market conditions, which could affect your monthly payments. It's crucial to review your loan documents and understand the terms to determine how the new interest rates may affect your loan.

To better understand the potential impact, let's look at the different types of loans:

- Federal student loans with fixed rates, such as Stafford Loans or PLUS Loans

- Private student loans with variable rates, such as those offered by banks or online lenders

- Consolidated loans, which combine multiple loans into one with a new interest rate

It's essential to note that if you have a loan with a variable rate, you may want to consider consolidating or refinancing to a fixed-rate loan to avoid potential rate increases.

If you're unsure about how the new student loan interest rates will affect your existing loans, it's a good idea to contact your lender or a financial advisor for personalized advice. They can help you review your loan terms and provide guidance on the best course of action to manage your debt effectively. Additionally, you can also check the official website of your lender or the Department of Education for the latest information on student loan interest rates and how they may impact your loans.

Can I refinance my student loans to get a better interest rate?

Refinancing your student loans can be a great way to save money on interest and lower your monthly payments. To determine if refinancing is right for you, it's essential to consider your current financial situation, including your credit score and income. A good credit score and stable income can help you qualify for better interest rates and terms.

When exploring refinancing options, it's crucial to research and compares rates from multiple lenders. Look for lenders that offer competitive interest rates, flexible repayment terms, and minimal fees. You can start by checking with online lenders, banks, and credit unions to see what options are available to you.

Here are some factors to consider when refinancing your student loans:

- Credit score: A good credit score can help you qualify for lower interest rates and better terms.

- Income: A stable income can help you qualify for refinancing and may also impact the interest rate you're offered.

- Loan terms: Consider the length of the loan, interest rate, and repayment terms to ensure they align with your financial goals.

For example, let's say you have a student loan with an interest rate of 6% and you refinance it to a loan with an interest rate of 4%. This could save you hundreds or even thousands of dollars in interest over the life of the loan. However, it's essential to carefully review the terms and conditions of the new loan to ensure it's a good fit for your financial situation.

Before making a decision, make sure to read reviews and ask questions to ensure you're working with a reputable lender. You can also use online tools and calculators to estimate your potential savings and determine if refinancing is right for you. By doing your research and carefully considering your options, you can make an informed decision and potentially save money on your student loans.

Are there any new loan forgiveness programs available for the 2025-2026 academic year?

As the 2025-2026 academic year approaches, many students and graduates are wondering if there are any new loan forgiveness programs available to help ease their debt burden. The Department of Education typically releases updates on new and existing programs, which can be a great resource for those looking to manage their student loans. It's essential to stay informed about these updates to make the most of the available options.

For the upcoming academic year, students can expect to see new programs and updates to existing ones, such as the Public Service Loan Forgiveness (PSLF) program. Details on these programs will be released by the Department of Education, and it's crucial to check their website regularly for the latest information. By staying up-to-date, students can plan their loan repayment strategy and potentially take advantage of new forgiveness opportunities.

Some examples of loan forgiveness programs that may be updated or expanded include:

- Teacher Loan Forgiveness program, which provides forgiveness options for teachers working in low-income schools

- Perkins Loan Cancellation program, which offers forgiveness for borrowers working in certain public service fields

- Income-Driven Repayment (IDR) plans, which can help borrowers manage their monthly payments and potentially qualify for forgiveness

These programs can be a significant help in reducing student loan debt, and understanding the eligibility criteria and application process can make all the difference. It's also a good idea to consult with a financial advisor or student loan expert to determine the best course of action for individual circumstances.

To stay ahead of the curve, students and graduates can sign up for email updates from the Department of Education or follow reputable financial aid websites to get the latest news on loan forgiveness programs. By being proactive and informed, individuals can make the most of the available options and work towards a more manageable debt load. As more information becomes available, it's essential to review and understand the eligibility criteria, application process, and any other requirements for the new and updated loan forgiveness programs.