As a graduate navigating the world of personal finance, it's essential to stay informed about the latest developments in the financial sector. The acquisition of non-performing microfinance institution (MFI) loans by asset reconstruction companies (ARCs) can have significant implications for your financial well-being. Understanding these implications can help you make informed decisions about your financial future.

When ARCs acquire non-performing MFI loans, it can impact the overall credit market and, in turn, affect your personal finance. For instance, if you have an outstanding loan from an MFI, the acquisition by an ARC may lead to changes in your loan terms or repayment schedule. It's crucial to review your loan agreement and communicate with your lender to understand any potential changes.

To better comprehend the effects of ARCs acquiring non-performing MFI loans on personal finance, consider the following key points:

- Changes in loan repayment terms, such as interest rates or tenure

- Potential impact on your credit score, especially if you have multiple outstanding loans

- Shifts in the overall credit market, which may influence interest rates and borrowing costs

By staying informed about these developments, you can take proactive steps to manage your finances effectively and make the most of your financial resources.

In the context of personal finance, it's also important to recognize that ARCs acquiring non-performing MFI loans can lead to increased scrutiny of borrowers' creditworthiness. As a result, it's essential to maintain a good credit history, make timely payments, and avoid defaulting on loans to ensure access to credit in the future. By adopting responsible financial habits, you can navigate the complexities of the financial sector with confidence.

What Are Non-Performing MFI Loans?

Non-performing loans refer to debts where the borrower has failed to make payments as agreed upon, causing a significant impact on both lenders and borrowers. This can lead to a loss of credit score for the borrower and a loss of revenue for the lender. For instance, if a borrower defaults on a loan, the lender may need to write off the loan as a bad debt, resulting in a financial loss.

The effects of non-performing loans can be far-reaching, affecting not only the individual borrower but also the overall financial health of institutions. When a large number of loans become non-performing, it can erode the confidence of investors and depositors, ultimately affecting the stability of the financial system. This is particularly concerning for Microfinance Institutions (MFIs), which provide financial services to low-income individuals and small businesses.

Microfinance Institutions play a vital role in promoting financial inclusion and providing access to credit for underserved populations. However, MFIs face unique challenges when dealing with non-performing loans, as their borrowers often have limited financial resources and may be more vulnerable to economic shocks. Some common challenges faced by MFIs include:

- High default rates due to borrower inability to repay loans

- Limited collateral or lack of credit history for borrowers

- High operational costs associated with loan recovery and collection

To mitigate the risks associated with non-performing loans, MFIs can implement strategies such as credit scoring, loan diversification, and borrower education. For example, MFIs can provide financial literacy training to borrowers to help them better manage their debt and make timely payments. By taking proactive steps to manage non-performing loans, MFIs can reduce their risk exposure and continue to provide essential financial services to their clients.

In addition to these strategies, MFIs can also leverage technology to improve loan recovery and collection. For instance, mobile payment systems can facilitate timely payments and reduce the risk of default. By embracing digital solutions and implementing effective risk management practices, MFIs can promote financial stability and support the economic growth of their clients. This, in turn, can have a positive impact on the overall financial health of individuals and institutions, contributing to a more stable and inclusive financial system.

How ARCs Acquire Non-Performing Loans

When it comes to managing debt, Asset Reconstruction Companies (ARCs) play a crucial role in acquiring non-performing loans. This process involves ARCs purchasing these loans from lenders, such as banks, at a discounted price. By doing so, lenders can free up their balance sheets and focus on core business activities.

The benefits of ARCs are numerous for both lenders and borrowers. For lenders, ARCs provide a way to recover a portion of their losses and avoid further provisioning for bad debts. For borrowers, ARCs offer a chance to restructure their debt and avoid legal action, which can be a more favorable outcome than dealing with the original lender.

Some of the key benefits of ARCs include:

- Improved cash flow for lenders through the sale of non-performing loans

- Reduced provisioning requirements for lenders, which can boost their profitability

- Flexibility for borrowers to restructure their debt and avoid legal consequences

In terms of the criteria used to determine the right price for acquiring non-performing loans, ARCs consider various factors, including the loan's outstanding balance, the borrower's credit history, and the value of any collateral attached to the loan.

To determine the right price, ARCs typically conduct a thorough due diligence process, which involves assessing the loan's recoverable value and the borrower's ability to repay. This process may include reviewing the borrower's financial statements, evaluating the loan's security, and assessing the overall market conditions. By considering these factors, ARCs can make informed decisions about the price they are willing to pay for a non-performing loan.

For example, if a borrower has a non-performing loan with an outstanding balance of $100,000, the ARC may offer to purchase the loan at a discounted price of $60,000, depending on the loan's recoverable value and the borrower's credit history. This can be a win-win situation for both the lender and the borrower, as the lender can recover a portion of their losses, and the borrower can avoid further legal action.

ARCs use various pricing models to determine the right price for acquiring non-performing loans, including the discounted cash flow method and the asset-based approach. These models take into account the loan's expected cash flows, the borrower's credit profile, and the value of any collateral attached to the loan. By using these models, ARCs can ensure that they are paying a fair price for the loan and maximizing their potential returns.

In conclusion, the process of ARCs acquiring non-performing loans is a complex one, involving careful consideration of various factors, including the loan's outstanding balance, the borrower's credit history, and the value of any collateral attached to the loan. By understanding how ARCs acquire non-performing loans, lenders and borrowers can better navigate the debt management process and achieve more favorable outcomes.

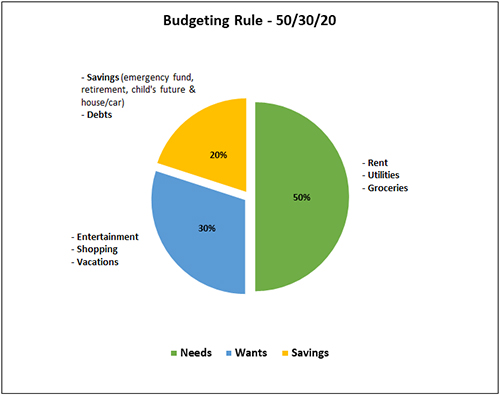

Impact on Personal Finance and Budgeting

When it comes to personal finance and budgeting, the acquisition of non-performing MFI loans by ARCs can have a significant impact on individuals. This is because such acquisitions can lead to changes in loan repayment terms, potentially affecting one's monthly expenses and financial planning. For instance, a person with a non-performing loan may face increased pressure to repay the loan, which can disrupt their budget and financial stability.

Managing debt is crucial in avoiding non-performing loan status, and there are several tips that can help individuals achieve this. Some of these tips include creating a budget and sticking to it, prioritizing debt repayment, and avoiding unnecessary expenses. By doing so, individuals can ensure that they are making timely loan repayments and avoiding the risk of default.

To avoid debt traps, it is essential to have a good understanding of one's financial health and budget. This can be achieved by:

- Tracking income and expenses to identify areas where costs can be cut

- Creating a budget that allocates sufficient funds for loan repayments

- Building an emergency fund to cover unexpected expenses

By following these steps, individuals can ensure that they are in control of their finances and are less likely to fall into debt traps.

In addition to managing debt, maintaining good financial health is also important in avoiding non-performing loan status. This can be achieved by monitoring credit scores, avoiding multiple loan applications, and making timely loan repayments. For example, a person with a good credit score may be able to negotiate better loan terms, reducing the risk of default and non-performing loan status.

Budgeting is a critical aspect of personal finance, and it plays a significant role in avoiding debt traps. By creating a budget and sticking to it, individuals can ensure that they are making timely loan repayments and avoiding unnecessary expenses. Moreover, budgeting can help individuals identify areas where costs can be cut, allowing them to allocate more funds towards loan repayments and build a safety net for unexpected expenses.

Ultimately, avoiding non-performing loan status requires a combination of good financial planning, budgeting, and debt management. By following the tips outlined above and maintaining good financial health, individuals can reduce the risk of default and ensure that they are in control of their finances. This, in turn, can help individuals achieve their long-term financial goals and avoid the stress and pressure associated with debt traps.

Investment and Side Hustle Opportunities

Investing in the microfinance sector can be a great way to diversify your portfolio while supporting small businesses and individuals in need. This sector provides financial services to low-income individuals or those who lack access to traditional banking services. By investing in microfinance, you can earn a return on your investment while making a positive impact on communities.

To get started, consider exploring online platforms that specialize in microfinance investments, such as peer-to-peer lending or crowdfunding. These platforms often provide a range of investment options with varying levels of risk and return. For example, you can invest in a portfolio of small business loans or provide funding for individual entrepreneurs.

In addition to investing, having a side hustle can be a great way to improve your financial health and avoid debt. Some popular side hustles include:

- Freelance writing or design work

- Selling products online through e-commerce platforms

- Ride-sharing or delivery work

These side hustles can provide a supplemental income stream, helping you pay off debt or build up your savings.

Understanding the acquisition of non-performing loans can also inform your investment decisions. Non-performing loans are debts that are in default or have a high risk of default, and investors can purchase these loans at a discount. By acquiring non-performing loans, investors can potentially earn a return by collecting on the debt or selling the loan to another investor. This requires careful analysis and due diligence, but can be a lucrative investment opportunity for those with experience.

When exploring investment opportunities, it's essential to do your research and consider your risk tolerance. Start by educating yourself on the different types of investments available, including microfinance and non-performing loans. You can also consult with a financial advisor or investment professional to get personalized advice and guidance. By taking a thoughtful and informed approach to investing, you can make progress towards your financial goals and build a more secure financial future.

Conclusion and Future Outlook

As we wrap up our discussion on ARCs acquiring non-performing MFI loans, it's essential to summarize the key points. ARCs, or Asset Reconstruction Companies, play a vital role in helping microfinance institutions manage their non-performing loans, which can have a significant impact on the overall financial health of these organizations. By acquiring these loans, ARCs can help MFIs recover some of their losses and focus on providing financial services to their customers.

The future implications of ARCs acquiring non-performing MFI loans are far-reaching, especially for personal finance and the microfinance sector. For young adults, it's crucial to understand how these developments can affect their financial decisions and stability. As the microfinance sector continues to evolve, it's likely that we'll see more innovative solutions and products emerge, which can help individuals manage their finances more effectively.

To manage their finances effectively, young adults can take several steps, including:

- Creating a budget and tracking expenses to understand where their money is going

- Building an emergency fund to cover unexpected expenses and avoid debt

- Investing in financial education and staying informed about personal finance topics

By following these tips, young adults can make informed decisions about their financial lives and achieve their long-term goals.

In terms of future outlook, the microfinance sector is expected to continue growing, with more emphasis on digitalization and financial inclusion. As ARCs continue to play a vital role in managing non-performing loans, we can expect to see more collaborations and partnerships between MFIs, ARCs, and other financial institutions. This can lead to more innovative products and services, such as mobile banking and digital payment systems, which can help individuals manage their finances more efficiently.

For young adults, the key takeaway is to stay informed and adapt to the changing financial landscape. By being proactive and taking control of their finances, they can navigate the complexities of the microfinance sector and achieve financial stability. Whether it's through budgeting, investing, or seeking financial advice, there are many resources available to help young adults make informed decisions about their financial lives.

Frequently Asked Questions (FAQ)

What are the benefits of ARCs acquiring non-performing loans for borrowers?

When borrowers struggle to repay their debts, they often face the risk of legal action and damage to their credit score. Asset Reconstruction Companies (ARCs) offer a way out of this situation by acquiring non-performing loans and providing borrowers with a chance to restructure their debt. This can be a lifeline for individuals and businesses that are overwhelmed by their financial obligations.

One of the main advantages of ARCs acquiring non-performing loans is that it allows borrowers to avoid the consequences of defaulting on their debts. By taking over the loan, the ARC can work with the borrower to create a new repayment plan that is more manageable and sustainable. This can help borrowers to get back on their feet and avoid the stress and uncertainty of legal action.

Some of the benefits of working with an ARC include:

- Flexibility in repayment plans, which can be tailored to the borrower's financial situation

- Reduced risk of legal action, which can damage credit scores and lead to further financial problems

- Opportunity to restructure debt and create a more sustainable financial future

For example, a borrower who is struggling to repay a large loan may be able to work with an ARC to reduce their monthly payments and extend the repayment period. This can make it easier for the borrower to manage their debt and avoid default.

By acquiring non-performing loans, ARCs can also help to free up capital for lenders, which can then be used to support new borrowing and economic growth. This can have a positive impact on the wider economy, as well as helping individual borrowers to get back on their feet. Overall, the acquisition of non-performing loans by ARCs can be a win-win situation for both borrowers and lenders.

How can individuals avoid having non-performing loans?

Maintaining a good credit score is essential to avoid having non-performing loans. A good credit score indicates to lenders that you are responsible with your finances and can repay loans on time. This can be achieved by making timely payments, keeping credit utilization low, and monitoring your credit report for errors.

Effective budgeting is also crucial in avoiding non-performing loans. By creating a budget and sticking to it, individuals can ensure they have enough funds to repay their loans. This includes prioritizing expenses, cutting back on unnecessary spending, and allocating a sufficient amount for loan repayments.

To avoid over-leveraging, individuals should be cautious when taking on debt. Some tips to keep in mind include:

- Only borrowing what you need, rather than the maximum amount offered

- Considering the total cost of the loan, including interest and fees

- Having a plan in place for repaying the loan, such as setting up automatic payments

By following these tips, individuals can reduce their risk of defaulting on loans and avoid the negative consequences that come with it.

Avoiding non-performing loans requires discipline and responsibility, but it is achievable with the right mindset and strategies. By prioritizing debt repayment, avoiding unnecessary debt, and maintaining a good credit score, individuals can ensure their financial stability and security. For example, setting up automatic payments and keeping track of expenses can help individuals stay on top of their loan repayments and avoid missing payments.

What role do MFIs play in financial inclusion and how does the acquisition of non-performing loans affect this role?

Microfinance institutions (MFIs) play a vital role in promoting financial inclusion by providing essential financial services to underserved populations, such as low-income individuals and small businesses. These services include microloans, savings accounts, and insurance products, which help individuals manage their finances and achieve economic stability. By offering these services, MFIs enable people to access credit and other financial tools that might not be available to them through traditional banking channels.

The acquisition of non-performing loans can significantly impact the ability of MFIs to continue offering their services. When MFIs acquire non-performing loans, they take on the risk of default, which can strain their resources and limit their capacity to lend to new customers. This can have a ripple effect on the entire community, as MFIs may need to reduce their lending activities or increase interest rates to mitigate their losses.

Some of the key ways that MFIs contribute to financial inclusion include:

- Providing microloans to small businesses and entrepreneurs, which helps to stimulate economic growth and job creation

- Offering savings accounts and other deposit products, which enable individuals to manage their finances and build wealth

- Delivering insurance products, such as health and life insurance, which helps to protect individuals against unexpected events and risks

These services are essential for promoting financial stability and reducing poverty, especially in developing countries where access to traditional banking services may be limited.

To mitigate the impact of non-performing loans, MFIs can implement various strategies, such as implementing robust credit scoring systems, providing financial education and training to their customers, and diversifying their loan portfolios. By taking these steps, MFIs can minimize their risk exposure and continue to provide essential financial services to underserved populations. This, in turn, can help to promote financial inclusion and reduce poverty, which is critical for achieving economic growth and stability.