As a student, navigating the world of student loans can be overwhelming, especially when it comes to finding the best interest rates. With so many options available, it's essential to do your research and compare rates to ensure you're getting the best deal. By doing so, you can save thousands of dollars in interest payments over the life of your loan.

When searching for the best student loan interest rates, it's crucial to consider your individual financial situation and needs. For example, if you have a good credit score, you may be eligible for lower interest rates or more favorable repayment terms. On the other hand, if you're an international student or have a limited credit history, you may need to explore alternative options.

To get started, let's take a look at some key factors to consider when comparing student loan interest rates:

- Fixed vs. variable interest rates

- Repayment terms and flexibility

- Fees associated with the loan

- Credit score requirements and eligibility

By understanding these factors and doing your research, you can make an informed decision and find the best student loan interest rates for your needs in 2025. Whether you're a freshman or a graduate student, this article will provide you with the guidance and tools you need to navigate the complex world of student loans.

Understanding Student Loan Interest Rates

When it comes to student loans, understanding interest rates is crucial for managing your debt effectively. Interest rates are calculated as a percentage of the loan amount, and they can vary depending on the lender and the type of loan. For example, federal student loans typically have fixed interest rates, while private student loans may have variable interest rates.

The difference between fixed and variable rates lies in their stability over time. Fixed rates remain the same throughout the loan term, whereas variable rates can change periodically based on market conditions. This means that with a variable rate loan, your monthly payments could increase or decrease as the interest rate changes.

To illustrate the impact of interest rates on total loan repayment amounts, consider the following examples:

- A $10,000 loan with a 4% fixed interest rate will accrue $2,149 in interest over 10 years, resulting in a total repayment amount of $12,149.

- In contrast, the same loan with a 6% fixed interest rate will accrue $3,319 in interest over 10 years, resulting in a total repayment amount of $13,319.

Even small differences in interest rates can add up significantly over time, making it essential to choose a loan with a competitive interest rate.

For instance, a 1% difference in interest rate can result in hundreds or even thousands of dollars in savings over the life of the loan. To put this into perspective, a $20,000 loan with a 5% interest rate will accrue $5,288 in interest over 10 years, while the same loan with a 4% interest rate will accrue $3,949 in interest. By choosing the loan with the lower interest rate, you can save $1,339 in interest payments.

It's also important to note that interest rates can affect your monthly payments, as a higher interest rate will typically result in higher monthly payments. By understanding how interest rates work and making informed choices, you can take control of your student loan debt and make progress towards financial freedom.

Best Student Loan Interest Rates for 2025

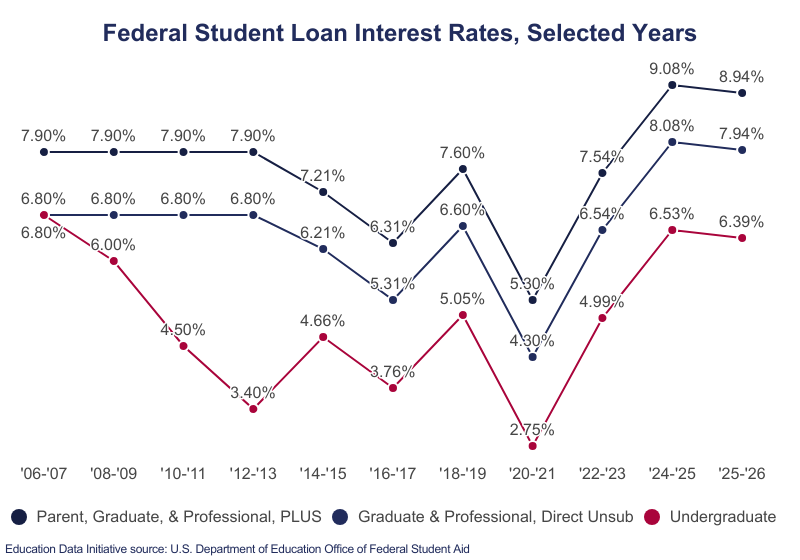

When it comes to finding the best student loan interest rates for 2025, it's essential to explore both federal and private loan options. Federal loans often offer more flexible repayment terms and forgiveness options, while private loans may provide more competitive interest rates. For example, the current federal undergraduate loan interest rate is around 4.53%, but private lenders may offer rates as low as 3.5%.

To get the best deal, it's crucial to compare rates among various lenders. Some top lenders offering competitive student loan interest rates for 2025 include:

- College Ave, with rates starting at 3.49%

- SoFi, offering rates as low as 3.5%

- Discover, with rates starting at 3.99%

These lenders often provide flexible repayment terms and may offer special promotions or discounts for good grades or autopay.

In addition to comparing interest rates, it's also important to consider any special promotions or discounts available. Some lenders offer rate reductions for students who make timely payments or maintain good grades. For instance, College Ave offers a 0.25% rate reduction for borrowers who make automatic payments. By taking advantage of these promotions, students can save even more money on their loans over time.

Private lenders may also offer variable interest rates, which can be lower than fixed rates but may increase over time. It's essential to carefully review the terms and conditions of any loan before signing, and to consider factors such as fees, repayment terms, and customer service. By doing your research and comparing rates among different lenders, you can find the best student loan interest rates for your needs and save money on your education expenses.

Some lenders also offer additional benefits, such as career support or loan forgiveness programs. For example, SoFi offers unemployment protection and career coaching to help borrowers navigate their careers. By considering these extra perks, students can find a lender that not only offers competitive interest rates but also provides support and resources to help them succeed.

Strategies for Managing Student Loan Debt

When it comes to managing student loan debt, one of the most effective strategies is to enroll in an income-driven repayment plan. These plans, such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE), cap your monthly payments at a percentage of your discretionary income, making them more affordable. For example, if you're a teacher or work in a non-profit, you may be eligible for loan forgiveness after a certain number of payments.

Income-driven repayment plans offer several benefits, including lower monthly payments and potential loan forgiveness. However, they may also increase the total amount you pay over the life of the loan due to accrual of interest. To get the most out of these plans, it's essential to understand the terms and conditions, as well as your own financial situation.

Another option for managing student loan debt is consolidating your loans. This involves combining multiple loans into a single loan with a fixed interest rate and monthly payment. The pros of consolidation include simplified payments and potentially lower interest rates, while the cons include losing benefits like loan forgiveness and potentially paying more in interest over the life of the loan.

Here are some key things to consider when deciding whether to consolidate your student loans:

- Check the interest rates on your current loans and compare them to the rate you'd get with a consolidation loan

- Consider the repayment terms and whether they align with your financial goals

- Look into any fees associated with consolidation, such as origination fees

To pay off your loans quickly, making extra payments is a great strategy. This can be as simple as paying a little more each month or making a lump sum payment when you get a tax refund or bonus. You can also consider using the snowball method, where you pay off your loans with the smallest balances first, or the avalanche method, where you pay off the loans with the highest interest rates first. By paying more than the minimum each month, you can save money on interest and become debt-free faster.

For instance, if you have a loan with a balance of $10,000 and an interest rate of 6%, paying an extra $100 per month can save you over $1,000 in interest over the life of the loan. By taking control of your student loan debt and making smart repayment decisions, you can free up more money in your budget for other goals, like saving for a down payment on a house or retirement.

Additional Tips for Saving Money on Student Loans

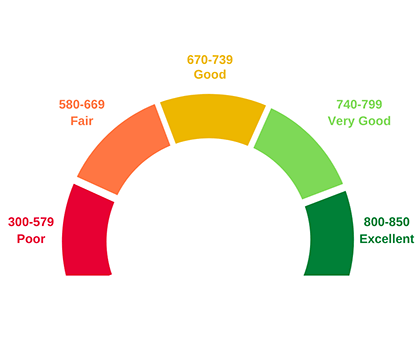

When it comes to saving money on student loans, your credit score plays a significant role in determining the interest rates you qualify for. A good credit score can help you secure lower interest rates, resulting in significant savings over the life of the loan. For instance, a credit score of 750 or higher can qualify you for interest rates that are 2-3% lower than those with a score of 600.

To improve your credit score and qualify for better rates, it's essential to understand what factors affect it. Your payment history, credit utilization, and credit age are just a few components that make up your credit score. By making timely payments, keeping credit card balances low, and avoiding new credit inquiries, you can improve your credit score over time.

Here are some practical tips to help you boost your credit score:

- Pay your bills on time, every time, to demonstrate responsible payment behavior

- Keep credit card balances below 30% of the credit limit to show lenders you can manage debt

- Monitor your credit report regularly to catch any errors or discrepancies

By following these tips, you can improve your credit score and increase your chances of qualifying for better interest rates on your student loans.

Refinancing your student loans can also be a great way to save money on interest rates. This involves taking out a new loan with a lower interest rate to pay off your existing loans, resulting in lower monthly payments and more money in your pocket. For example, if you have a $30,000 loan with an interest rate of 6%, refinancing to a 4% interest rate can save you over $1,000 in interest payments per year.

Before refinancing your student loans, it's crucial to carefully review the terms and conditions of the new loan. Consider factors such as the interest rate, repayment term, and fees associated with the loan. By doing your research and comparing rates from different lenders, you can find the best deal and make the most of refinancing your student loans.

Conclusion and Next Steps

As you've made it to the end of this article, you should now have a better understanding of how to navigate the complex world of student loans. To recap, we've covered the importance of borrowing wisely and making informed decisions about your financial aid. By doing so, you can set yourself up for long-term financial success and minimize debt after graduation.

When exploring student loan options, it's essential to compare rates, terms, and repayment plans from various lenders. This will help you find the best fit for your individual circumstances. For example, you may want to consider federal loans, private loans, or a combination of both, depending on your financial situation and goals.

Some key points to keep in mind as you move forward include:

- Interest rates and fees associated with each loan

- Repayment terms and flexible payment options

- Eligibility requirements and application processes

By carefully evaluating these factors, you can make an informed decision that works in your favor.

If you're looking for more information and support, there are many resources available to help you on your financial journey. You can visit the Federal Student Aid website for detailed guides and tools, or reach out to a financial advisor for personalized advice. Additionally, online forums and communities can provide valuable insights and connections with others who are going through similar experiences.

Ultimately, taking control of your student loans requires patience, persistence, and a willingness to learn and adapt. By staying informed and proactive, you can overcome financial challenges and achieve your goals, whether that means graduating debt-free or simply finding a manageable repayment plan. Remember to stay up-to-date with the latest news and developments in the world of student finance, and don't hesitate to seek help when you need it.

Frequently Asked Questions (FAQ)

How do I qualify for the best student loan interest rates?

To get the best student loan interest rates, it's essential to understand the factors that lenders consider when evaluating your application. A good credit score is a crucial aspect, as it demonstrates your ability to manage debt and make timely payments. For example, a credit score of 750 or higher can significantly improve your chances of qualifying for a lower interest rate.

When applying for a student loan, choosing the right repayment plan can also impact the interest rate you're offered. Lenders often provide more favorable terms to borrowers who opt for automatic payments or commit to a specific repayment schedule. This can help reduce the risk for the lender and result in a lower interest rate for you.

In some cases, having a co-signer with a good credit history can help you qualify for better student loan interest rates. This is especially true for students who are new to credit or have a limited credit history. Here are some tips to keep in mind:

- Check your credit report to ensure it's accurate and up-to-date

- Consider working with a co-signer who has a good credit score

- Compare rates and terms from multiple lenders to find the best option

By following these tips and understanding the factors that influence interest rates, you can increase your chances of qualifying for the best student loan interest rates and save money over the life of the loan.

Can I refinance my student loans to get a better interest rate?

Refinancing your student loans can be a great way to save money on interest and lower your monthly payments. By refinancing, you can potentially secure a lower interest rate, which can lead to significant savings over the life of your loan. For example, if you have a $30,000 loan with an interest rate of 6%, refinancing to a 4% interest rate could save you thousands of dollars in interest payments.

When considering refinancing, it's essential to understand the terms and potential risks involved. You'll need to review your current loan agreement and compare it to the new loan terms to ensure you're making a smart financial decision. This includes evaluating the new interest rate, repayment term, and any fees associated with the loan.

Here are some key factors to consider when refinancing your student loans:

- Check your credit score, as a good credit score can help you qualify for better interest rates

- Compare rates and terms from multiple lenders to find the best option for your situation

- Consider the repayment term, as a longer term may mean lower monthly payments but more interest paid overall

Before making a decision, it's crucial to weigh the potential benefits against the potential risks. For instance, if you refinance a federal student loan, you may lose access to certain benefits, such as income-driven repayment plans or loan forgiveness programs. On the other hand, refinancing a private student loan may not come with these risks, but you'll still need to carefully review the new loan terms to ensure you're getting a good deal.

To get started with refinancing, you can research and compare rates from various lenders, such as banks, credit unions, or online lenders. You can also use online tools and calculators to determine how much you could save by refinancing your student loans. By taking the time to understand your options and make an informed decision, you can potentially save money and simplify your finances.

Are there any student loan forgiveness programs available?

If you're struggling to pay off your student loans, you're not alone. Several student loan forgiveness programs can help alleviate the burden of debt, and it's essential to explore these options. Public Service Loan Forgiveness, for instance, is a popular program that can significantly reduce or eliminate student loan debt under specific conditions.

To qualify for Public Service Loan Forgiveness, you typically need to work full-time for a qualifying employer, such as a government agency or non-profit organization. You'll also need to make 120 qualifying payments under a qualifying repayment plan. For example, if you're a teacher or nurse working for a public hospital, you may be eligible for this program.

Some other notable student loan forgiveness programs include:

- Teacher Loan Forgiveness, which can forgive up to $17,500 of your Direct Loans or FFEL Loans

- Perkins Loan Cancellation, which can cancel up to 100% of your Perkins Loans if you work in a qualifying field

- Income-Driven Repayment (IDR) forgiveness, which can forgive any remaining balance after 20 or 25 years of qualifying payments

These programs can be a game-changer for graduates who are struggling to make ends meet, and it's crucial to research and understand the eligibility criteria for each program.

When exploring student loan forgiveness options, it's essential to review the terms and conditions carefully and consider seeking guidance from a financial advisor or your loan servicer. By understanding the available programs and their requirements, you can make informed decisions about your student loan debt and potentially save thousands of dollars in the long run.