As a young adult, navigating the world of student loans can be overwhelming, especially when it comes to understanding interest rates. It's essential to grasp the concept of interest rates, as it can significantly impact the overall cost of your loan. For instance, a higher interest rate can lead to paying more over the life of the loan, while a lower rate can save you thousands of dollars.

To manage your debt effectively, you need to consider the type of interest rate associated with your loan, such as fixed or variable rates. Fixed rates remain the same throughout the loan term, while variable rates can fluctuate, affecting your monthly payments. Understanding the difference between these two types of rates can help you make informed decisions about your loan repayment strategy.

Here are some key factors to consider when understanding student loan interest rates:

- Know the current interest rate on your loan

- Understand how interest accrues and is capitalized

- Consider the impact of compounding interest on your loan balance

By taking the time to learn about student loan interest rates, you can develop a solid plan to tackle your debt and set yourself up for long-term financial success. You can start by reviewing your loan documents, talking to your lender, or seeking advice from a financial advisor to get a better understanding of your specific situation.

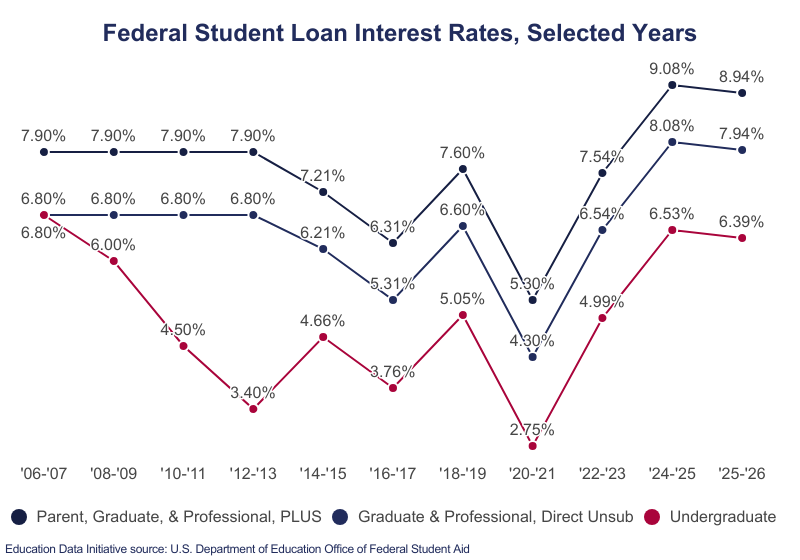

Understanding Federal Student Loan Interest Rates

The current federal student loan interest rates for 2025 range from 4.53% to 7.54%, depending on the type of loan and the borrower's degree level. For instance, undergraduate students can expect to pay an interest rate of 4.53% on Direct Subsidized and Unsubsidized Loans. This rate is slightly higher than the 2024 rate, which was 4.33%.

There are several types of federal student loans, each with its own interest rate. The main types of federal student loans include:

- Direct Subsidized Loans: These loans are available to undergraduate students who demonstrate financial need, and the interest is paid by the government while the student is in school.

- Direct Unsubsidized Loans: These loans are available to both undergraduate and graduate students, and the interest accrues while the student is in school.

The interest rates for these loans vary, with Direct Subsidized and Unsubsidized Loans having an interest rate of 4.53% for the 2025 academic year.

To check the interest rate on a federal student loan, borrowers can log in to their account on the Federal Student Aid website or contact their loan servicer directly. Borrowers can also review their loan documents or contact the Financial Aid office at their school for more information. For example, a borrower with a $10,000 Direct Unsubsidized Loan at an interest rate of 4.53% can expect to pay around $453 in interest over the course of a year, assuming the interest is not paid while the student is in school.

In comparison to previous years, federal student loan interest rates have fluctuated. The interest rates for the 2023 academic year were lower, ranging from 4.23% to 6.54%. Understanding how interest rates have changed over time can help borrowers make informed decisions about their loans and repayment options. By staying up-to-date on current interest rates and loan terms, borrowers can develop a personalized plan to manage their debt effectively.

Private Student Loan Interest Rates: What to Expect

When exploring private student loan options, understanding the interest rates is crucial. Private student loan interest rates can vary significantly among top lenders, with some offering fixed rates and others providing variable rates. For instance, lenders like Sallie Mae and Discover offer fixed rates, while others like College Ave and LendingClub provide variable rates.

The interest rates offered by private lenders depend on several factors, including credit score and loan term. A good credit score can help you qualify for lower interest rates, while a longer loan term may result in higher overall interest paid. For example, a borrower with a credit score of 750 may qualify for a 4.5% interest rate, while a borrower with a score of 650 may be offered a 7.5% rate.

Some key factors that influence private student loan interest rates include:

- Credit score: A good credit score can help you qualify for lower interest rates

- Loan term: Longer loan terms may result in higher overall interest paid

- Co-signer credit score: Having a co-signer with a good credit score can help you qualify for better rates

- Loan amount: Larger loan amounts may result in higher interest rates

To negotiate a better interest rate with a private lender, it's essential to shop around and compare rates from multiple lenders. You can also consider applying with a co-signer who has a good credit score, as this can help you qualify for more favorable rates.

Additionally, some lenders may offer interest rate discounts for certain criteria, such as enrolling in automatic payments or making on-time payments. For example, Discover offers a 0.25% interest rate reduction for borrowers who enroll in automatic payments. By understanding the factors that influence interest rates and shopping around for the best rates, you can make informed decisions about your private student loan options.

)

Strategies to Minimize Student Loan Interest

Income-driven repayment plans are a great way to minimize student loan interest, as they can lower your monthly payments and reduce the amount of interest that accrues over time. By capping your monthly payments at a certain percentage of your income, you can avoid paying more in interest than you need to. For example, if you have a high-interest loan but a low income, an income-driven plan can help you stay on top of your payments.

When it comes to refinancing student loans to a lower interest rate, there are both pros and cons to consider. On the plus side, refinancing can save you money in interest over the life of the loan, and may also give you more flexible repayment terms. However, refinancing may also mean giving up certain benefits, such as income-driven repayment or loan forgiveness options.

Here are some things to consider when deciding whether to refinance your student loans:

- Check your credit score to see if you qualify for a lower interest rate

- Compare rates and terms from different lenders to find the best deal

- Consider the fees associated with refinancing, and make sure you understand the repayment terms

Making extra payments can also help you pay off your principal balances faster, which can in turn reduce the amount of interest you accrue over time. By paying more than the minimum each month, you can chip away at the principal balance and save yourself money in interest. For instance, if you have a loan with a $10,000 balance and an interest rate of 6%, paying an extra $100 per month can save you over $1,000 in interest over the life of the loan.

To make the most of extra payments, try to focus on the loan with the highest interest rate first, and make sure to specify that any extra payments should be applied to the principal balance. You can also consider setting up automatic payments or using a budgeting app to help you stay on track and make consistent extra payments. By taking a proactive approach to your student loans, you can minimize interest accrual and pay off your debt faster.

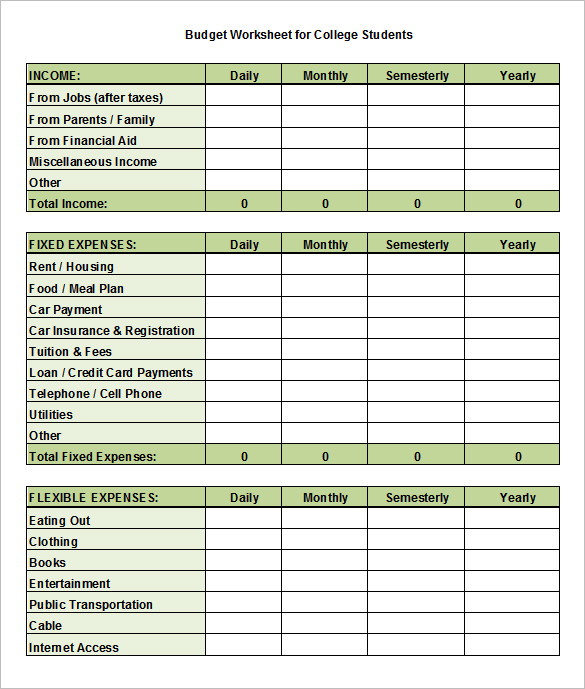

Budgeting for Student Loan Payments

When it comes to managing student loan debt, creating a budget is essential. To start, you'll want to calculate your total monthly income and expenses, including your student loan payments. This will give you a clear picture of where your money is going and help you identify areas where you can cut back.

The 50/30/20 rule is a great guideline to follow when allocating your income towards expenses, savings, and debt repayment. This rule suggests that 50% of your income should go towards necessary expenses like rent and utilities, 30% towards discretionary spending, and 20% towards saving and debt repayment. For example, if you earn $4,000 per month, you would allocate $2,000 towards necessary expenses, $1,200 towards discretionary spending, and $800 towards saving and debt repayment.

To prioritize your student loan payments, consider using the debt snowball or avalanche method. These methods involve ranking your debts in a specific order and focusing on paying off one debt at a time. The debt snowball method involves paying off debts with the smallest balances first, while the avalanche method involves paying off debts with the highest interest rates first. Here are some steps to follow:

- Make a list of all your student loans, including the balance, interest rate, and minimum payment for each loan

- Rank your loans in order of priority, using either the debt snowball or avalanche method

- Focus on paying off the loan with the highest priority, while making minimum payments on the other loans

By following these steps and using the 50/30/20 rule as a guideline, you can create a budget that accounts for your student loan payments and helps you manage your debt effectively. Remember to review and adjust your budget regularly to ensure you're on track to meeting your financial goals. For instance, you may need to adjust your budget if you receive a pay raise or if your loan interest rates change.

In addition to creating a budget and prioritizing your payments, consider taking advantage of income-driven repayment plans or loan forgiveness programs to help manage your student loan debt. These options can help lower your monthly payments or even forgive a portion of your loan balance, making it easier to stay on top of your debt. Be sure to research and explore these options to determine if they're right for you.

Long-Term Financial Planning with Student Loans

When it comes to managing student loans, it's easy to get caught up in the monthly payments and forget about the bigger picture. Building an emergency fund is crucial, as it provides a safety net in case of unexpected expenses or job loss. By setting aside even a small amount each month, you can avoid going further into debt when unexpected costs arise.

Creating a budget that accounts for both student loan payments and emergency fund contributions is essential. A general rule of thumb is to have 3-6 months' worth of living expenses saved in an easily accessible savings account. This fund can help you stay on track with your loan payments, even if you encounter financial setbacks.

Investing for retirement may seem like a distant goal, but it's essential to start early, even if you're still paying off student loans. Consider contributing to a Roth IRA, which allows you to contribute after-tax dollars and potentially withdraw the money tax-free in retirement. By starting to invest early, you can take advantage of compound interest and set yourself up for long-term financial success.

Some key ways to invest for retirement while paying off student loans include:

- Setting up automatic transfers from your checking account to your retirement account

- Taking advantage of employer matching contributions, if available

- Starting with a small, manageable contribution amount and increasing it over time

By making retirement investing a priority, you can create a more secure financial future.

Having a side hustle or additional income stream can be a game-changer when it comes to paying off student loans. By earning extra money, you can put more towards your loans each month, potentially saving yourself thousands of dollars in interest over the life of the loan. Consider freelancing, selling items online, or taking on a part-time job to boost your income and accelerate your debt payoff.

For example, if you can earn an extra $500 per month through a side hustle, you could put that money towards your student loans and potentially pay them off years ahead of schedule. This can also free up more money in your budget for other financial goals, such as saving for a down payment on a house or investing in a taxable brokerage account. By being proactive and taking control of your finances, you can set yourself up for long-term success and achieve your goals.

Frequently Asked Questions (FAQ)

How do federal student loan interest rates differ from private loan rates?

When it comes to financing your education, understanding the differences between federal and private student loan interest rates is crucial. Federal student loan interest rates are generally fixed, meaning they remain the same throughout the life of the loan. This can provide borrowers with a sense of stability and predictability in their monthly payments.

In contrast, private loan rates can be variable, which means they can fluctuate over time based on market conditions. This can make it more challenging for borrowers to anticipate their monthly payments, as their interest rate may increase or decrease. For example, a variable interest rate of 6% may increase to 8% or more if market conditions change.

The interest rates for federal student loans are also subsidized, which means the government pays the interest on the loan while the borrower is in school. Private loans, on the other hand, are not subsidized, and interest accrues from the moment the loan is disbursed. Here are some key differences between federal and private student loan interest rates:

- Federal student loan interest rates are typically lower than private loan rates

- Private loan rates depend on the borrower's creditworthiness, with better credit scores resulting in lower interest rates

- Federal student loans offer more flexible repayment options and forgiveness programs compared to private loans

To make an informed decision about which type of loan is best for you, it's essential to consider your financial situation and credit history. If you have a good credit score, you may be able to qualify for a lower interest rate with a private lender. However, if you're a student with limited credit history, a federal student loan may be a more affordable and stable option. By understanding the differences between federal and private student loan interest rates, you can make a more informed decision about how to finance your education.

Can I refinance my student loans to a lower interest rate?

Refinancing your student loans can be a great way to save money on interest payments over time. By refinancing to a lower interest rate, you can reduce your monthly payments and free up more money in your budget for other expenses. This can be especially helpful if you have high-interest private student loans or federal loans with variable rates.

To refinance your student loans, you'll typically need a good credit score and a stable income. Lenders use these factors to determine how likely you are to repay your loan, so having a solid credit history and a reliable income can help you qualify for better interest rates. For example, if you've graduated and landed a steady job, you may be able to refinance your loans to a lower rate.

Here are some things to consider when refinancing your student loans:

- Check your credit score to see if you qualify for better interest rates

- Research different lenders and compare their rates and terms

- Consider consolidating multiple loans into one loan with a lower interest rate

By taking the time to research and compare your options, you can find a refinancing plan that works for you and helps you save money on interest payments.

It's also important to note that refinancing federal student loans can have some drawbacks, such as losing access to income-driven repayment plans and forgiveness programs. However, if you have private student loans or are confident in your ability to repay your loans, refinancing can be a smart financial move. Be sure to weigh the pros and cons carefully before making a decision.

What are the consequences of not paying student loan interest?

Failing to pay student loan interest can have severe consequences on your financial health. Accrued interest can add up quickly, increasing the total amount you owe on your loan. For instance, if you have a $30,000 loan with a 6% interest rate, you could accrue over $1,800 in interest per year if left unpaid.

When you miss payments, you may also be charged late fees, which can range from 1% to 6% of the overdue amount. These fees can further increase your debt burden, making it even harder to pay off your loan. To avoid late fees, it's essential to set up automatic payments or reminders to ensure you never miss a payment.

The consequences of not paying student loan interest can also extend to your credit score. Negative impacts on credit scores can occur when lenders report missed payments to the credit bureaus. Here are some ways unpaid interest can affect your credit:

- Lower credit scores, making it harder to get approved for future loans or credit cards

- Higher interest rates on future loans, increasing your debt burden

- Difficulty getting approved for apartments or other forms of credit

To avoid these consequences, it's crucial to prioritize paying your student loan interest and making timely payments. By doing so, you can keep your debt under control and maintain a healthy credit score.