As a student with poor credit, finding the best student loan options can be a daunting task. Many students struggle to secure loans due to their limited credit history or past financial mistakes. However, with the right guidance, it is possible to find affordable and suitable loan options.

When it comes to student loans, credit scores play a significant role in determining the interest rates and repayment terms. Students with poor credit may face higher interest rates or stricter repayment conditions, making it essential to explore all available options carefully. For instance, students can start by checking their credit report to identify areas for improvement.

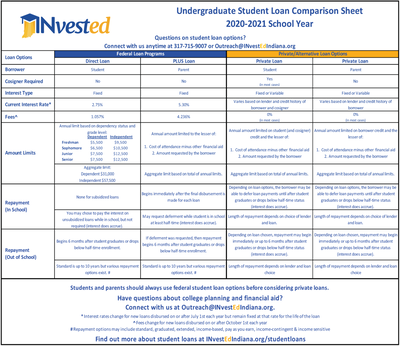

To get started, students can consider the following options:

- Federal student loans, which do not require a credit check

- Private student loans with co-signers, which can help reduce interest rates

- Alternative loan programs, such as income-driven repayment plans

These options can provide a more affordable and manageable way to finance education, even with poor credit.

By understanding the different types of student loans and their requirements, students can make informed decisions about their financial aid. This article will delve into the world of student loans, providing practical tips and examples to help students with poor credit find the best loan options for their needs. With the right knowledge and strategy, students can overcome their credit challenges and achieve their academic goals.

Understanding Poor Credit Student Loans

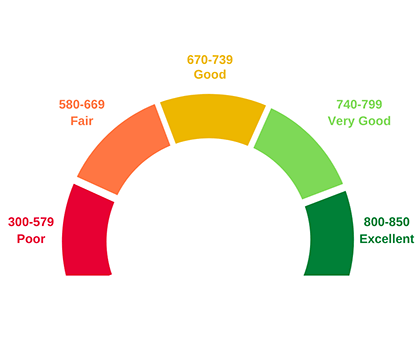

When it comes to student loans, having poor credit can significantly impact your eligibility and the terms of your loan. Poor credit refers to a low credit score, which is typically below 620, indicating a history of late payments, defaulted loans, or other negative credit behaviors. This can make it challenging to secure a loan with favorable interest rates and terms.

Credit scores play a crucial role in determining loan interest rates and terms, as they help lenders assess the risk of lending to you. A good credit score can lead to lower interest rates, lower fees, and more flexible repayment terms, while a poor credit score can result in higher interest rates, higher fees, and stricter repayment terms. For example, a student with a credit score of 750 may qualify for a loan with a 4% interest rate, while a student with a credit score of 500 may be offered a loan with a 10% interest rate.

Here are some examples of credit score ranges and their corresponding loan options:

- Credit score 750-850: eligible for federal student loans, private loans with low interest rates (4-6%), and flexible repayment terms

- Credit score 650-749: eligible for federal student loans, private loans with moderate interest rates (6-8%), and standard repayment terms

- Credit score 550-649: eligible for private loans with high interest rates (8-12%), strict repayment terms, and may require a co-signer

- Credit score below 550: may not be eligible for traditional loans, but may be eligible for alternative loans with very high interest rates (12-18%) and strict repayment terms

It's essential to note that credit scores are not the only factor considered in student loan eligibility, and some lenders may offer more flexible options for students with poor credit. By understanding how credit scores impact loan options, students can take steps to improve their credit scores and secure more favorable loan terms.

Top 5 Student Loans for Poor Credit

As a student with poor credit, finding the right loan option can be challenging. The first loan option to consider is the Ascent Student Loan, which offers competitive interest rates ranging from 3.22% to 14.75% and repayment terms of up to 15 years. This loan also features flexible payment plans, including a 9-month grace period after graduation.

The second loan option is the LendingPoint Student Loan, which provides benefits such as deferment or forbearance options for students experiencing financial hardship. For instance, students can defer payments for up to 12 months if they are experiencing economic hardship or are enrolled in school at least half-time. This loan option also offers interest rates between 5.99% and 19.99%.

Some key features of student loans for poor credit include:

- Flexible repayment terms

- Competitive interest rates

- Deferment or forbearance options

The third loan option is the Funding U Student Loan, which offers unique characteristics such as no cosigner required and no fees for origination, disbursement, or late payments. This loan option also features interest rates between 7.99% and 12.99% and repayment terms of up to 10 years.

The fourth loan option is the MPOWER Student Loan, which provides benefits such as career support and job placement assistance. This loan option also offers interest rates between 5.99% and 14.59% and repayment terms of up to 10 years. For example, students can take advantage of MPOWER's career support services to help them find a job after graduation and start repaying their loan.

The fifth loan option is the Stride Student Loan, which features a unique characteristic of allowing students to pay as little as $25 per month while in school. This loan option also offers interest rates between 5.99% and 14.99% and repayment terms of up to 15 years. It's essential for students to review and compare these loan options to find the one that best suits their financial needs and goals.

How to Apply for Student Loans with Poor Credit

To apply for student loans with poor credit, it's essential to understand the process and requirements. The first step is to check your credit score, which can be done for free on various websites such as Credit Karma or Credit Sesame. This will give you an idea of where you stand and what you need to work on.

When applying for student loans with poor credit, you'll need to gather required documents, including proof of income, tax returns, and identification. You may also need to provide documentation of your credit history, such as credit card statements or loan records. It's crucial to have all these documents ready to ensure a smooth application process.

Improving your credit score before applying for student loans can significantly increase your chances of approval. Here are some tips to help you improve your credit score:

- Pay your bills on time to demonstrate responsible credit behavior

- Keep credit card balances low to show lenders you can manage debt

- Avoid applying for multiple credit cards or loans in a short period

By following these tips, you can improve your credit score over time and become a more attractive borrower.

If you're struggling to get approved for a student loan due to poor credit, consider having a co-signer. A co-signer is someone with good credit who agrees to take on the responsibility of the loan if you're unable to make payments. This can be a parent, guardian, or another creditworthy individual. Having a co-signer can help you secure a student loan with a lower interest rate and more favorable terms.

Before applying for a student loan with a co-signer, make sure you both understand the terms and conditions of the loan. You'll need to provide documentation for both yourself and your co-signer, including identification, income verification, and credit history. It's also essential to discuss and agree on a repayment plan to ensure you're both on the same page.

In addition to federal student loans, you may also want to explore private student loan options. Some private lenders offer more flexible credit requirements, but be cautious of higher interest rates and fees. Be sure to research and compare different lenders to find the best option for your situation. By taking the time to understand your options and prepare your application, you can increase your chances of securing a student loan even with poor credit.

Managing Student Loan Debt with Poor Credit

Paying off student loans can be overwhelming, especially when dealing with poor credit. One effective strategy is to enroll in an income-driven repayment plan, which adjusts monthly payments based on income and family size. For example, the Income-Based Repayment (IBR) plan can help lower monthly payments, making it more manageable to pay off loans quickly.

To avoid defaulting on student loans, it's essential to understand deferment and forbearance options. Deferment allows temporary suspension of loan payments due to financial hardship, while forbearance temporarily reduces or suspends payments. Both options can help avoid default, but it's crucial to contact the loan servicer to discuss the best course of action.

When managing student loan debt, monitoring credit reports and scores is vital. This can be done by requesting a free credit report from the three major credit bureaus (Experian, TransUnion, and Equifax) and checking for errors or inaccuracies. By doing so, individuals can ensure their credit score is not negatively affected by their student loan debt.

Some key tips for managing student loan debt with poor credit include:

- Communicating with the loan servicer to discuss repayment options and temporary hardship programs

- Consolidating loans to simplify payments and potentially lower interest rates

- Making timely payments to avoid late fees and negative credit reporting

By following these tips and staying proactive, individuals can effectively manage their student loan debt and work towards improving their credit score over time.

It's also important to note that defaulting on student loans can have severe consequences, including damaged credit and wage garnishment. To avoid this, individuals should prioritize their loan payments and explore alternative repayment options, such as the Pay As You Earn (PAYE) plan or the Revised Pay As You Earn (REPAYE) plan. By taking control of their student loan debt, individuals can set themselves up for long-term financial success.

Alternatives to Student Loans for Poor Credit

When it comes to financing your education, having poor credit can be a significant obstacle. However, there are several alternatives to student loans that can help you achieve your academic goals. Scholarships and grants are excellent options, as they do not require a credit check and can be based on merit, need, or other factors.

Scholarships and grants for students with poor credit are available from various sources, including universities, private organizations, and government agencies. You can search for these opportunities on websites such as Fastweb or Scholarships.com, which offer a wide range of awards. Some examples of scholarships for students with poor credit include the Pell Grant and the Federal Supplemental Educational Opportunity Grant.

In addition to scholarships and grants, part-time jobs or side hustles can help fund your education expenses. Having a part-time job can not only provide you with a steady income but also give you valuable work experience and skills. Some popular part-time job options for students include:

- Tutoring or teaching assistant positions

- Freelance writing or graphic design work

- Part-time retail or food service jobs

Crowdfunding or community resources are another alternative to student loans for students with poor credit. You can use platforms like GoFundMe or Kickstarter to create a campaign and raise funds for your education expenses. Additionally, many communities have resources such as non-profit organizations or local businesses that offer financial assistance to students. For example, some churches or community centers may offer scholarships or grants to students in need.

To increase your chances of securing funding through crowdfunding or community resources, it's essential to have a clear plan and budget for your education expenses. You should also be prepared to provide documentation or information about your financial situation and academic goals. By exploring these alternatives to student loans, you can reduce your reliance on debt and achieve your academic goals despite having poor credit.

Frequently Asked Questions (FAQ)

Can I get a student loan with very poor credit?

Having poor credit can make it difficult to secure a student loan, but it's not impossible. Some lenders specialize in offering student loans to individuals with less-than-perfect credit, often with certain conditions. These conditions may include higher interest rates or requiring a co-signer with good credit to guarantee the loan.

When exploring student loan options with poor credit, it's essential to understand the terms and conditions. Lenders may offer variable interest rates, which can increase over time, or fixed interest rates, which remain the same throughout the loan period. For instance, a lender might offer a student loan with a 12% interest rate, which is higher than the average rate for students with good credit.

To increase your chances of getting approved for a student loan with poor credit, consider the following options:

- Apply with a co-signer who has good credit, such as a parent or guardian

- Look for lenders that offer bad credit student loans or no credit check student loans

- Check with your school's financial aid office for potential alternatives or recommendations

Keep in mind that these options may have higher interest rates or fees, so it's crucial to carefully review the loan agreement before signing.

If you're struggling to find a lender that offers student loans with poor credit, you may want to consider alternative options, such as federal student loans or income-driven repayment plans. These options often have more flexible eligibility requirements and may offer more favorable terms. Additionally, you can try to improve your credit score by making timely payments on existing debts and keeping credit utilization low, which can help you qualify for better loan terms in the future.

How can I improve my credit score to get better student loan options?

Paying bills on time is a crucial step in improving your credit score, as it demonstrates your ability to manage debt responsibly. By setting up automatic payments or reminders, you can ensure that you never miss a payment deadline. This simple habit can have a significant impact on your credit score over time.

Reducing debt is another essential factor in boosting your credit score, as it shows lenders that you can handle your financial obligations. To get started, make a list of your debts, including student loans, credit cards, and other financial obligations, and prioritize them based on interest rates and urgency. This will help you create a plan to pay off high-interest debts first and free up more money in your budget for savings and investments.

Monitoring your credit reports for errors or inaccuracies is also vital, as mistakes can negatively affect your credit score. You can request a free credit report from each of the three major credit reporting agencies (Experian, TransUnion, and Equifax) once a year, and review them carefully for any errors. Some common errors to look out for include:

- Inaccurate account information, such as incorrect balances or payment histories

- Accounts that do not belong to you, which could be a sign of identity theft

- Outdated information, such as closed accounts that are still listed as open

By checking your credit reports regularly and disputing any errors you find, you can help ensure that your credit score is accurate and reflects your true creditworthiness.

In addition to these strategies, there are several other ways to improve your credit score, such as keeping credit utilization low, avoiding new credit inquiries, and building a long credit history. By following these tips and staying committed to your financial goals, you can improve your credit score and qualify for better student loan options, which can save you money and reduce your financial stress in the long run. For example, you may be able to qualify for lower interest rates or more favorable repayment terms, which can make a big difference in your monthly payments and overall debt burden.

Are there any student loan forgiveness programs for borrowers with poor credit?

Having poor credit can make it challenging to manage student loan debt, but there are options available for borrowers. Some student loan forgiveness programs are available, but they often require specific criteria, such as working in public service or meeting income thresholds. These programs can be a lifeline for borrowers who are struggling to make ends meet.

To be eligible for student loan forgiveness programs, borrowers typically need to meet specific requirements, such as working in a certain field or making a certain number of payments. For example, the Public Service Loan Forgiveness (PSLF) program is available to borrowers who work in public service, including jobs in government, non-profit, or education. This program can be a great option for borrowers who are committed to working in these fields.

Some popular student loan forgiveness programs include:

- Public Service Loan Forgiveness (PSLF)

- Teacher Loan Forgiveness

- Income-Driven Repayment (IDR) forgiveness

These programs can help borrowers manage their debt and potentially have some or all of their loans forgiven. Borrowers should research these programs carefully to determine which ones they may be eligible for and to understand the requirements and application process.

In addition to student loan forgiveness programs, borrowers with poor credit may also want to consider income-driven repayment plans, which can help lower monthly payments and make debt more manageable. These plans can be a good option for borrowers who are struggling to make payments, as they can help reduce the risk of default and provide a more affordable repayment schedule. By exploring these options and creating a plan to manage debt, borrowers can take control of their finances and work towards a more stable financial future.