As a graduate student, navigating the world of student loans can be overwhelming. With numerous options available, it's essential to find the best loan that fits your educational needs and financial situation. By understanding the different types of loans and their requirements, you can make an informed decision that will help you achieve your academic goals.

When searching for the best loans, consider factors such as interest rates, repayment terms, and borrower benefits. For example, federal loans often offer more flexible repayment options and lower interest rates compared to private loans. It's crucial to weigh these factors to determine which loan is the most suitable for your situation.

To get started, let's explore the key considerations for graduate students:

- Interest rates and fees associated with the loan

- Repayment terms and options for deferment or forbearance

- Eligibility requirements and application process

By examining these factors, you can narrow down your options and find a loan that aligns with your financial goals and educational aspirations.

In this article, we will delve into the world of graduate student loans, providing you with the necessary information to make an informed decision. Whether you're pursuing a master's degree or a doctoral program, our guide will help you find the best loan for your educational needs. With the right loan, you can focus on your studies and achieve your academic objectives without financial stress.

Understanding Graduate Student Loans

As a graduate student, navigating the world of student loans can be overwhelming. Federal graduate student loans, such as the Direct Unsubsidized Loan and the Graduate PLUS Loan, offer fixed interest rates and flexible repayment terms. For instance, the Direct Unsubsidized Loan has a fixed interest rate of around 6%, while the Graduate PLUS Loan has a fixed interest rate of around 7%.

In contrast, private graduate student loans often have variable interest rates, which can range from 4% to 12%, and less flexible repayment terms. Private lenders may also offer benefits like cosigner release or interest rate discounts, but these perks can vary widely between lenders. It's essential to carefully review the terms and conditions of each loan before making a decision.

When considering graduate student loans, it's crucial to think about loan forgiveness and discharge options. These options can help you manage your debt after graduation, especially if you pursue a career in a public service field. Some examples of loan forgiveness programs include:

- Public Service Loan Forgiveness (PSLF) for federal loans

- Teacher Loan Forgiveness for educators

- Perkins Loan Cancellation for certain public service jobs

To compare loan offers from different lenders, make a list of the key terms, including interest rate, repayment term, and fees. For example, you might compare the following:

- Interest rate: 6% fixed vs 8% variable

- Repayment term: 10 years vs 15 years

- Fees: 2% origination fee vs no fees

By carefully evaluating these factors and considering your individual financial situation, you can make an informed decision about which graduate student loan is right for you. Remember to also review the lender's customer service and repayment flexibility, as these can impact your overall borrowing experience.

Top Federal Graduate Student Loans

As a graduate student, navigating the world of federal student loans can be overwhelming. Direct Unsubsidized Loans are a popular option, offering numerous benefits, including a fixed interest rate and flexible repayment terms. For instance, these loans can be used to cover tuition, fees, and living expenses, making them a great resource for graduate students.

To be eligible for Direct Unsubsidized Loans, students must be enrolled at least half-time in a graduate program, have a valid Free Application for Federal Student Aid (FAFSA), and meet general eligibility requirements. The application process typically begins with completing the FAFSA, which helps determine the amount of loan funding a student is eligible for. This amount can vary depending on factors like the cost of attendance and other forms of financial aid.

In addition to Direct Unsubsidized Loans, Graduate PLUS Loans are another option for graduate students. The application process for these loans involves a credit check, which assesses an applicant's creditworthiness. To apply, students typically need to:

- Complete the FAFSA to determine eligibility

- Check their credit report for errors or negative marks

- Apply for the Graduate PLUS Loan through the Federal Student Aid website

A good credit score can increase the chances of approval and may lead to more favorable loan terms.

Consolidating federal graduate student loans can have several advantages, including simplified repayment and potentially lower monthly payments. By combining multiple loans into one, students can manage their debt more effectively and make timely payments. For example, consolidating loans can help students avoid missing payments, which can negatively impact their credit score and lead to additional fees.

When considering consolidation, it's essential to weigh the pros and cons, as it may affect the overall cost of the loan and the repayment term. Students should research and compare different consolidation options to determine the best approach for their individual circumstances. By doing so, they can make informed decisions about their financial aid and create a plan to manage their debt effectively.

Best Private Graduate Student Loans

When exploring private graduate student loans, it's essential to compare the interest rates and repayment terms of popular lenders. Sallie Mae and Discover are two well-known options, offering competitive rates and flexible repayment plans. For instance, Sallie Mae's graduate student loans have interest rates ranging from 4.25% to 11.79% APR, while Discover's rates range from 4.24% to 12.24% APR.

Considering lender fees is also crucial, as they can significantly impact the overall cost of the loan. Some lenders may charge origination fees, late payment fees, or other charges, so it's vital to review the terms carefully. Borrower benefits, such as forbearance and deferment options, can also be a deciding factor, as they provide temporary relief from loan payments during financial hardship.

To secure the best loan terms, it's essential to understand the key factors to consider when evaluating private lenders. Here are some key points to keep in mind:

- Interest rates: Look for lenders offering competitive, fixed or variable rates

- Repayment terms: Consider lenders with flexible repayment plans, including income-driven repayment options

- Fees: Be aware of any lender fees, including origination fees, late payment fees, and other charges

- Borrower benefits: Evaluate lenders offering benefits like forbearance, deferment, and loan forgiveness options

Negotiating with private lenders can also help secure better loan terms. One tip is to ask about potential discounts or promotions, such as a 0.25% interest rate reduction for automatic payments. Additionally, borrowers can try to negotiate a lower interest rate or more favorable repayment terms by providing proof of good credit or a stable income. By doing their research and being proactive, graduate students can find the best private student loan for their needs and set themselves up for long-term financial success.

Applying for Graduate Student Loans

To begin the process of securing graduate student loans, it's essential to fill out the Free Application for Federal Student Aid (FAFSA). This application will determine your eligibility for federal student loans, as well as other forms of financial aid. By visiting the official FAFSA website, you can create an account and start your application.

The FAFSA application process involves providing personal and financial information, including your social security number, tax returns, and bank statements. You'll also need to list the graduate schools you're interested in attending, as this information will be used to determine your eligibility for aid. It's crucial to complete the application accurately and submit it before the deadline to ensure you receive consideration for all available aid.

In addition to federal student loans, you may also want to consider applying for private graduate student loans. This process typically involves a credit check, which will help lenders determine your interest rate and loan terms. Some lenders may also require a co-signer, especially if you have limited credit history or a low credit score.

When applying for private graduate student loans, it's essential to review and understand the loan terms before accepting an offer. This includes:

- Interest rate: Is it fixed or variable, and how will it affect your monthly payments?

- Repayment terms: What are the repayment options, and are there any fees associated with early payment or late payment?

- Fees: Are there any origination fees, late fees, or other charges that will be added to your loan balance?

By carefully reviewing these terms, you can make an informed decision about which loan is best for your financial situation.

For example, let's say you're considering two private loan offers: one with a fixed interest rate of 6% and a 10-year repayment term, and another with a variable interest rate of 4% and a 5-year repayment term. By reviewing the loan terms, you can determine which option will save you the most money in interest payments over the life of the loan. By taking the time to understand your loan options and terms, you can make a smart financial decision and set yourself up for long-term success.

Managing Graduate Student Loan Debt

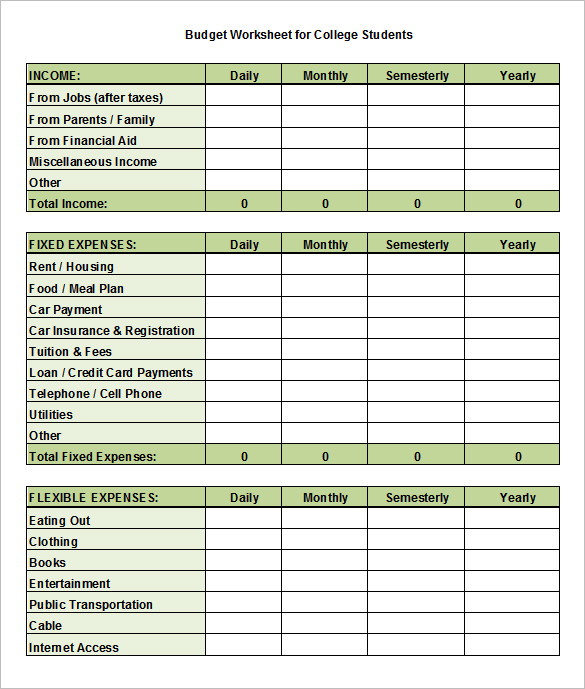

Creating a budget is the first step in managing graduate student loan debt. Start by tracking your income and expenses to understand where your money is going. You can use a budgeting app or spreadsheet to make this process easier and identify areas where you can cut back.

When it comes to repayment, consider income-driven repayment options, which can lower your monthly payments based on your income and family size. For example, the Income-Based Repayment (IBR) plan can cap your monthly payments at 10% or 15% of your discretionary income. This can be a big relief if you're struggling to make ends meet.

To explore your repayment options, you can:

- Visit the Federal Student Aid website to learn about different repayment plans and calculate your potential monthly payments

- Use online tools, such as the Student Loan Repayment Calculator, to compare different plans and find the best fit for your situation

- Consult with a financial advisor or student loan expert to get personalized advice

Refinancing or consolidating your graduate student loans can also be a viable option, but it's essential to weigh the benefits and drawbacks. Refinancing can help you get a lower interest rate, but you may lose federal benefits like income-driven repayment and loan forgiveness. Consolidating your loans can simplify your payments, but it may not always save you money.

The benefits of refinancing or consolidating include:

- Lower monthly payments or interest rates

- Simplified payments and fewer bills to keep track of

- Potentially lower total interest paid over the life of the loan

However, it's crucial to consider the potential drawbacks, such as losing federal benefits or ending up with a longer repayment period.

If you're struggling to manage your debt, don't hesitate to seek financial counseling or explore loan forgiveness programs. Many organizations, such as the National Foundation for Credit Counseling, offer free or low-cost counseling and resources. You can also look into loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), which can forgive part or all of your debt if you work in a qualifying field.

For more information on loan forgiveness programs and financial counseling, you can:

- Visit the Department of Education's website to learn about federal loan forgiveness programs

- Check with your employer or professional organization to see if they offer any loan repayment assistance or forgiveness benefits

- Reach out to a financial advisor or credit counselor for personalized guidance and support

Frequently Asked Questions (FAQ)

What is the difference between a subsidized and unsubsidized graduate student loan?

As a graduate student, navigating the world of student loans can be overwhelming. One key distinction to understand is the difference between subsidized and unsubsidized loans. Subsidized loans are a more desirable option, as they do not accrue interest while the student is in school, allowing borrowers to focus on their studies without worrying about growing debt.

In contrast, unsubsidized loans do accrue interest from the moment the loan is disbursed, which means that the total amount owed will increase over time. For example, if you borrow $10,000 in unsubsidized loans at a 6% interest rate, you could owe over $11,000 by the time you graduate, even if you don't make any payments while in school.

Here are some key points to consider when evaluating subsidized and unsubsidized loans:

- Subsidized loans are generally awarded based on financial need, while unsubsidized loans are available to all borrowers, regardless of need.

- The interest rate on subsidized and unsubsidized loans is typically the same, but the accrual of interest is what sets them apart.

- Borrowers can take steps to minimize the impact of unsubsidized loans, such as making interest-only payments while in school or considering income-driven repayment plans after graduation.

To make the most of your graduate student loans, it's essential to understand the terms and conditions of each type of loan. By doing your research and creating a smart borrowing strategy, you can set yourself up for long-term financial success and minimize the burden of debt after graduation. By prioritizing subsidized loans and making informed decisions about unsubsidized loans, you can take control of your financial future and achieve your goals.

Can I consolidate my graduate student loans?

Consolidating graduate student loans can be a great way to simplify your finances and make repayment more manageable. By combining multiple loans into one, you can reduce the number of payments you need to make each month, which can help you stay organized and avoid missed payments. This can be especially helpful if you have loans with different interest rates, repayment terms, or due dates.

When you consolidate your loans, you may be able to lower your monthly payments by extending the repayment period or switching to a more affordable repayment plan. For example, if you have a high-interest loan with a short repayment term, consolidating it with a lower-interest loan with a longer repayment term could reduce your monthly payments and make them more affordable. This can be a big relief if you're struggling to make ends meet.

Here are some benefits of consolidating your graduate student loans:

- Simplified repayment: One loan, one payment, one due date

- Lower monthly payments: By extending the repayment period or switching to a more affordable plan

- Potential interest rate savings: If you consolidate high-interest loans into a lower-interest loan

It's essential to consider your individual circumstances and loan terms before consolidating, as it may not be the best option for everyone. You should review your loan agreements and consult with a financial advisor if needed, to determine if consolidating your graduate student loans is the right choice for you.

To get started with consolidating your loans, you can contact your loan servicer or visit the official website of the US Department of Education to explore your options. You can also use online tools and calculators to compare different repayment plans and see which one works best for you. By taking the time to research and understand your options, you can make an informed decision and find a repayment strategy that fits your budget and financial goals.

How do I know which graduate student loan is best for me?

As a graduate student, navigating the world of student loans can be overwhelming. With numerous options available, it's essential to consider several key factors to make an informed decision. Interest rates, for instance, play a significant role in determining the overall cost of your loan, so it's crucial to look for loans with competitive rates.

When evaluating graduate student loans, repayment terms are another critical factor to consider. Look for loans that offer flexible repayment plans, such as income-driven repayment or deferment options, which can help you manage your debt more effectively. For example, some lenders may offer a six-month grace period after graduation, giving you time to find a job before starting repayments.

To choose the best loan for your needs, consider the borrower benefits offered by each lender. Some lenders may provide benefits like automatic payment discounts, interest rate reductions for good grades, or loan forgiveness programs. Here are some key borrower benefits to look out for:

- Autopay discounts, which can reduce your interest rate by 0.25%

- Interest rate reductions for making timely payments

- Loan forgiveness programs, which can cancel out some or all of your debt

In addition to these factors, it's also essential to research and compares different lenders to find the best fit for your situation. You can use online tools and resources, such as loan comparison websites or financial aid calculators, to help you make a more informed decision. By taking the time to evaluate your options carefully, you can find a graduate student loan that meets your needs and sets you up for long-term financial success.

Ultimately, choosing the right graduate student loan requires careful consideration of your individual circumstances and financial goals. By weighing factors like interest rates, repayment terms, and borrower benefits, you can make a smart decision that will help you achieve your academic and professional aspirations. Be sure to read the fine print and ask questions before committing to a loan, and don't hesitate to seek guidance from a financial aid advisor if you need help navigating the process.