As a graduate student, financing your education can be a daunting task. With numerous loan options available, it's essential to choose the best one that suits your needs. To get started, consider your financial goals, current income, and debt obligations to determine how much you can afford to borrow.

When exploring graduate student loan options, several key factors come into play. These include interest rates, repayment terms, and fees associated with the loan. For instance, federal loans often have more favorable terms, such as income-driven repayment plans and forgiveness options, whereas private loans may offer more competitive interest rates for borrowers with good credit.

To make an informed decision, consider the following key factors:

- Interest rates and fees: Look for loans with low interest rates and minimal fees to minimize your overall debt.

- Repayment terms: Choose a loan with a repayment plan that aligns with your financial situation, such as income-driven repayment or deferment options.

- Eligibility criteria: Check the eligibility requirements for each loan, including credit score, income, and enrollment status.

By carefully evaluating these factors, you can find the best graduate student loan for your needs and set yourself up for long-term financial success.

In the following sections, we will delve into the specifics of each loan type, including federal and private options, to help you make a more informed decision. With the right loan, you can focus on your studies and achieve your academic goals without excessive financial burden.

Understanding Graduate Student Loans

As a graduate student, navigating the world of student loans can be overwhelming. Federal graduate student loans, such as the Direct Unsubsidized Loan and the Grad PLUS Loan, offer fixed interest rates and flexible repayment terms. For instance, the Direct Unsubsidized Loan has a fixed interest rate of around 6%, while the Grad PLUS Loan has a fixed interest rate of around 7%.

In contrast, private graduate student loans often have variable interest rates, which can range from 4% to 12%, and less flexible repayment terms. Private lenders may also offer more competitive interest rates, but it's essential to carefully review the terms and conditions before committing to a loan. Some private lenders, like Sallie Mae and Discover, offer variable interest rates starting at around 4%.

When considering graduate student loans, it's crucial to think about loan forgiveness options and income-driven repayment plans. These options can help make loan repayment more manageable, especially for students pursuing careers in public service or non-profit sectors. For example, the Public Service Loan Forgiveness (PSLF) program can forgive the remaining balance on a Direct Loan after 120 qualifying payments.

To compare loan offers from different lenders, consider the following factors:

- Interest rate: Is it fixed or variable, and what are the repayment terms?

- Fees: Are there any origination fees, late payment fees, or other charges?

- Repayment options: Are there income-driven repayment plans or loan forgiveness options available?

For instance, a lender like SoFi may offer a variable interest rate starting at 4%, with no origination fees and flexible repayment terms, while a lender like Wells Fargo may offer a fixed interest rate of 6%, with an origination fee of 2% and less flexible repayment terms.

Income-driven repayment plans, such as the Income-Based Repayment (IBR) plan and the Pay As You Earn (PAYE) plan, can also help make loan repayment more affordable. These plans cap monthly payments at a percentage of the borrower's discretionary income, making it easier to manage debt. By understanding the different types of graduate student loans and repayment options, borrowers can make informed decisions about their financial aid and create a more sustainable plan for loan repayment.

Top Federal Graduate Student Loans

As a graduate student, exploring federal loan options is a crucial step in funding your education. Direct Unsubsidized Loans are a popular choice, offering a fixed interest rate and flexible repayment terms. These loans are available to eligible graduate students, regardless of financial need, with borrowing limits of up to $20,500 per year.

To be eligible for Direct Unsubsidized Loans, students must be enrolled at least half-time in a graduate program, and must not have defaulted on previous federal loans. The loan amount is determined by the school, and students can use the funds to cover tuition, fees, and living expenses. For example, a graduate student pursuing a master's degree can use Direct Unsubsidized Loans to cover the cost of tuition, books, and housing.

Federal Perkins Loans are another option for graduate students, offering a low fixed interest rate and a nine-month grace period after graduation. The pros of Federal Perkins Loans include:

- Cancellation options for certain public service jobs, such as teaching or nursing

- No interest accrual during the grace period

- Repayment terms of up to 10 years

However, the cons include limited funding and a more complex application process.

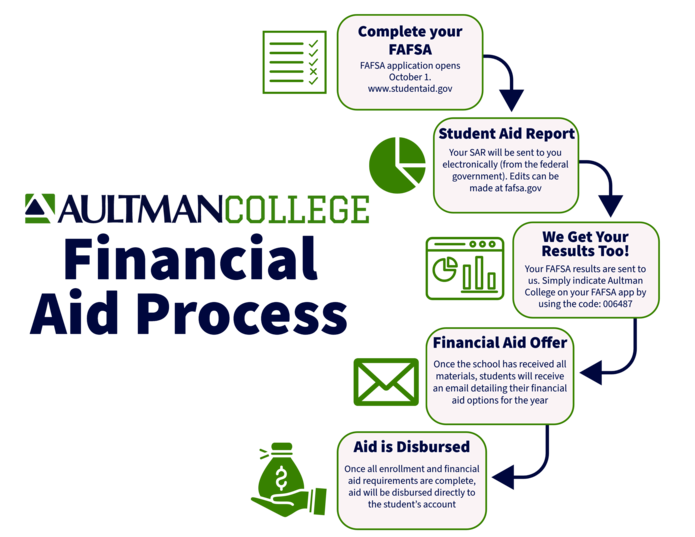

To apply for federal graduate student loans, students must complete the Free Application for Federal Student Aid (FAFSA). The FAFSA is available online, and students can submit their application as early as October 1st for the upcoming academic year. By applying through the FAFSA, students can determine their eligibility for federal loans, as well as other forms of financial aid, such as grants and work-study programs.

When completing the FAFSA, students will need to provide personal and financial information, including their Social Security number, tax returns, and bank statements. It's essential to review the application carefully, as errors or omissions can delay processing. For instance, students should ensure they list their school code correctly, as this will determine the types of aid they are eligible for.

Repayment terms for federal graduate student loans vary depending on the loan type and amount borrowed. For example, Direct Unsubsidized Loans have a standard repayment term of 10 years, while Federal Perkins Loans offer more flexible repayment options. Students should review their loan terms carefully and consider options such as income-driven repayment or loan forgiveness programs.

Best Private Graduate Student Loans

When exploring private graduate student loans, it's essential to compare the interest rates and repayment terms of popular lenders, such as Sallie Mae and Wells Fargo. These lenders often offer competitive rates, but it's crucial to review the terms carefully to ensure you're getting the best deal. For instance, Sallie Mae offers variable rates ranging from 2.12% to 12.87% APR, while Wells Fargo's rates range from 3.39% to 10.49% APR.

Considering credit score requirements and cosigner options is also vital when selecting a private lender. Most lenders require a good credit score, typically 650 or higher, to qualify for a loan. If you have a limited credit history, you may need a cosigner to secure a loan, which can be a parent, guardian, or creditworthy individual.

Some popular private lenders offer flexible repayment terms, including:

- Deferred payment options, allowing you to postpone payments while in school

- Income-driven repayment plans, which base your monthly payments on your income

- Forgiveness programs, which may forgive a portion of your loan balance after a certain period

These options can help make your loan more manageable, but be sure to review the terms and conditions carefully.

To negotiate with private lenders and secure better loan terms, consider the following tips:

- Check your credit report and dispute any errors to improve your credit score

- Compare rates and terms from multiple lenders to find the best offer

- Contact the lender directly to discuss potential discounts or promotions

By doing your research and being proactive, you can potentially save thousands of dollars in interest over the life of your loan.

Ultimately, finding the right private graduate student loan requires careful consideration of your financial situation, credit score, and repayment goals. By weighing your options and negotiating with lenders, you can secure a loan that helps you achieve your educational goals without breaking the bank. Be sure to review and understand all the terms and conditions before signing any loan agreement.

Repayment Strategies and Budgeting

When it comes to paying off graduate student loans, two popular repayment strategies are the snowball method and the avalanche method. The snowball method involves paying off loans with the smallest balances first, while making minimum payments on larger loans. This approach can provide a psychological boost as you quickly eliminate smaller debts and see progress.

The avalanche method, on the other hand, focuses on paying off loans with the highest interest rates first, which can save you more money in interest over time. To determine which method is best for you, consider your individual financial situation and goals. For example, if you have a loan with a very high interest rate, the avalanche method may be the better choice.

Creating a budget is essential for prioritizing loan repayment and making progress on your debt. Start by tracking your income and expenses to see where your money is going, and then make a plan to allocate a certain amount each month towards loan repayment. You can use the 50/30/20 rule as a guideline, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment.

To boost your income and put more towards loan repayment, consider taking on a side hustle or pursuing additional income streams. Some examples include:

- Freelance writing or editing

- Tutoring or teaching online

- Selling products through an online marketplace

- Ride-sharing or driving for a food delivery service

These types of side hustles can provide a flexible way to earn extra money and put it towards your loans.

In addition to side hustles, there are other income-boosting strategies that can help with loan repayment. For example, you could ask for a raise at your current job, pursue additional education or certifications to increase your earning potential, or consider taking on a part-time job. By prioritizing loan repayment and finding ways to increase your income, you can make steady progress on your debt and achieve financial stability.

Additional Resources and Tips

When it comes to funding your graduate education, there are many resources available to help. For scholarships and grants, you can start by checking out websites like Fastweb or Scholarships.com, which offer a wide range of opportunities to suit different fields of study and backgrounds. Additionally, many universities and colleges have their own scholarship programs, so be sure to check with your school's financial aid office.

Monitoring your credit reports and credit scores is crucial during loan repayment, as a good credit score can help you qualify for lower interest rates and better loan terms. You can request a free credit report from each of the three major credit reporting agencies (Experian, TransUnion, and Equifax) once a year, and review it carefully to ensure there are no errors or inaccuracies. This can help you avoid any potential issues or surprises during the loan repayment process.

To avoid common mistakes when applying for graduate student loans, consider the following tips:

- Start by researching and comparing different loan options to find the best fit for your needs and budget

- Make sure you understand all the terms and conditions of your loan, including interest rates, repayment terms, and any fees associated with the loan

- Apply for federal student loans before considering private loans, as they often have more favorable terms and repayment options

By following these tips and doing your research, you can make informed decisions about your graduate student loans and set yourself up for success.

It's also important to stay organized and keep track of your loan applications and deadlines. You can use a spreadsheet or a tool like a loan calculator to help you compare different loan options and stay on top of your finances. For example, you can use the Federal Student Aid website to explore different loan options and estimate your monthly payments.

Finally, don't be afraid to seek help if you need it - many universities and colleges have financial aid offices that can provide guidance and support throughout the loan application and repayment process. You can also reach out to a financial advisor or a credit counselor for personalized advice and guidance.

Frequently Asked Questions (FAQ)

What is the difference between a subsidized and unsubsidized graduate student loan?

As a graduate student, navigating the world of student loans can be overwhelming. One key distinction to understand is the difference between subsidized and unsubsidized loans. Subsidized loans are a more desirable option, as they offer a significant benefit: the government pays the interest on these loans while you are in school.

This means that subsidized loans can help minimize the amount you owe after graduation. For example, if you borrow $10,000 in subsidized loans, you won't accrue any interest on that amount until you've finished your degree. In contrast, unsubsidized loans require you to pay the interest, which can add up quickly.

Here are some key points to consider when deciding between subsidized and unsubsidized loans:

- Subsidized loans have the interest paid by the government while you are in school, which can save you money in the long run.

- Unsubsidized loans require you to pay the interest, either while you are in school or after you graduate.

- Both types of loans have limits on how much you can borrow, so it's essential to understand these limits and plan accordingly.

To make the most of subsidized loans, it's a good idea to prioritize borrowing these funds first. If you're eligible for subsidized loans, try to maximize this amount before turning to unsubsidized loans. By doing so, you can reduce the amount of interest you owe and make your loan payments more manageable after graduation.

In practical terms, this might mean borrowing the maximum subsidized amount each year, and then using unsubsidized loans to cover any remaining expenses. By understanding the differences between subsidized and unsubsidized loans, you can make informed decisions about your graduate school financing and set yourself up for long-term financial success.

Can I refinance my graduate student loans to get a better interest rate?

Refinancing your graduate student loans can be a great way to lower your interest rate and save money on your monthly payments. By refinancing, you essentially take out a new loan with a lower interest rate and use it to pay off your existing loans. This can be especially beneficial if you have high-interest loans or if you've improved your credit score since you first took out the loans.

When considering refinancing, it's essential to weigh the pros and cons. On the one hand, refinancing can help you lower your interest rate and reduce your monthly payments. On the other hand, it may affect your loan forgiveness options and repayment terms. For example, if you refinance a federal loan, you may no longer be eligible for income-driven repayment plans or public service loan forgiveness.

Here are some things to consider when deciding whether to refinance your graduate student loans:

- Check your credit score to see if you qualify for a lower interest rate

- Compare rates and terms from different lenders to find the best deal

- Consider the impact on your loan forgiveness options and repayment terms

It's also important to note that refinancing is not the same as consolidating your loans. Consolidation combines multiple loans into one loan with a single interest rate, while refinancing replaces your existing loans with a new loan that has a different interest rate and repayment terms.

If you're unsure about whether refinancing is right for you, it may be helpful to speak with a financial advisor or use a refinancing calculator to see how much you could save. You can also research different lenders and their refinancing options to find the best fit for your situation. By doing your research and carefully considering your options, you can make an informed decision about whether refinancing your graduate student loans is the right choice for you.

How do I know which graduate student loan is best for me?

When it comes to choosing a graduate student loan, it's essential to consider your individual circumstances and financial goals. This means thinking about your expected income after graduation, your debt-to-income ratio, and your overall financial situation. By taking a close look at these factors, you can make an informed decision about which loan is best for you.

Interest rates are a crucial factor to consider when selecting a graduate student loan. Loans with lower interest rates can save you money in the long run, so it's worth shopping around to find the best rates. For example, a loan with a 4% interest rate may be a better option than one with a 6% interest rate, depending on the other terms of the loan.

In addition to interest rates, repayment terms are also important to consider. Some loans may offer more flexible repayment options, such as income-driven repayment plans or deferment, which can be helpful if you're not sure what your income will be after graduation. Here are some factors to consider when evaluating repayment terms:

- Loan term length: How long do you have to repay the loan?

- Monthly payment amount: How much will you need to pay each month?

- Repayment plan options: Are there income-driven repayment plans or other flexible options available?

Loan forgiveness options are another factor to consider when choosing a graduate student loan. Some loans, such as those offered by the federal government, may offer forgiveness options after a certain number of years of qualifying payments. For instance, the Public Service Loan Forgiveness program forgives the remaining balance on a loan after 120 qualifying payments for borrowers who work in public service jobs. By considering these factors, you can choose a loan that aligns with your individual circumstances and financial goals.