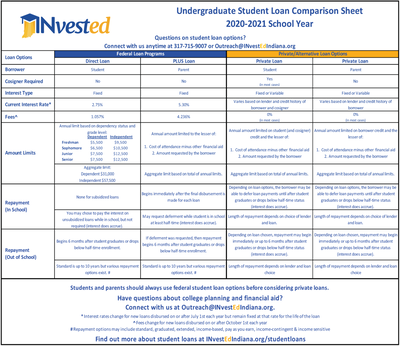

As a young adult, navigating the world of student loans can be overwhelming, especially when it comes to private student loans. Private student loans are an essential option for many students who require additional funding beyond federal loans to cover education expenses. For instance, students pursuing higher education or vocational training may find private student loans helpful in bridging the financial gap.

Private student loans are offered by banks, credit unions, and other financial institutions, and they often have varying interest rates and repayment terms. It's crucial for young adults to understand the terms and conditions of private student loans before applying, as they can significantly impact their financial future. By doing so, students can make informed decisions about their borrowing options and create a personalized plan to manage their debt.

When considering private student loans, there are several key factors to keep in mind, including:

- Interest rates and fees associated with the loan

- Repayment terms and options

- Eligibility criteria and required credit score

- Maximum borrowing limits and loan amounts

By carefully evaluating these factors, young adults can determine whether private student loans are the right choice for their educational and financial goals. Additionally, students should also explore other funding options, such as scholarships and grants, to minimize their reliance on loans.

Understanding Private Student Loans

When it comes to financing your education, you may have heard of private student loans as an alternative to federal loans. Private student loans are offered by banks, credit unions, and other lenders, and they differ from federal loans in terms of interest rates and repayment terms. For instance, private student loan interest rates can be variable or fixed, and repayment terms may be more flexible than those of federal loans.

One of the key benefits of private student loans is that they can be used to cover additional educational expenses, such as living expenses, books, and equipment. Private student loans can also offer flexible repayment options, allowing you to choose a repayment plan that suits your financial situation. This can be particularly helpful if you're having trouble making payments on your federal loans.

In general, private student loans can be a good option for students who have already maxed out their federal loan options or need additional funding for their education. Some benefits of private student loans include:

- Covering additional educational expenses, such as study abroad programs or summer classes

- Offering flexible repayment options, such as deferred payments or income-driven repayment plans

- Allowing you to borrow up to the full cost of attendance, minus any other financial aid you're receiving

It's worth noting that private student loan interest rates can be higher than those of federal loans, so it's essential to carefully review the terms and conditions before borrowing.

Your credit score plays a significant role in determining your eligibility for private student loans, as well as the interest rate you'll qualify for. A good credit score can help you qualify for a lower interest rate, which can save you money over the life of the loan. For example, if you have a credit score of 750 or higher, you may qualify for a private student loan with an interest rate of 4.5%, compared to a rate of 7.5% if you have a credit score of 600.

To improve your chances of getting approved for a private student loan with a competitive interest rate, it's a good idea to:

- Check your credit report for errors and dispute any inaccuracies

- Make on-time payments on your existing debts to demonstrate responsible credit behavior

- Consider applying with a creditworthy cosigner, such as a parent or guardian

By understanding how private student loans work and how your credit score affects your eligibility, you can make informed decisions about how to finance your education.

Top Private Student Loan Lenders for 2025

When it comes to funding your education, private student loans can be a viable option. Reviewing and comparing the top private student loan lenders is essential to find the best fit for your financial situation. This includes considering interest rates, fees, and repayment terms to ensure you're getting a fair deal.

Private student loan lenders offer a range of benefits, including competitive interest rates and flexible repayment plans. Some lenders also provide unique benefits, such as cosigner release options or career support services, which can be a major advantage for students. For example, lenders like SoFi and CommonBond offer career support services to help students navigate their professional paths.

To help you get started, here are some top private student loan lenders to consider:

- SoFi: Offers competitive interest rates and career support services

- CommonBond: Provides cosigner release options and a range of repayment plans

- Discover: Offers no fees and a rewards program for good grades

These lenders cater to a range of students, including those with poor or no credit history. For instance, Discover offers private student loans to students with no credit history, as long as they have a creditworthy cosigner.

Students with poor or no credit history can also consider lenders that specialize in non-traditional credit evaluation methods. For example, lenders like LendingPoint and Funding U use alternative credit scoring models to evaluate creditworthiness. This can be a good option for students who may not have an established credit history.

In addition to considering interest rates and fees, it's essential to review the repayment terms and options offered by each lender. Some lenders offer income-driven repayment plans or deferment options, which can provide flexibility and peace of mind. By doing your research and comparing lenders, you can find a private student loan that meets your needs and helps you achieve your educational goals.

How to Choose the Best Private Student Loan

When exploring private student loan options, it's essential to consider several key factors to ensure you're making an informed decision. Interest rates, fees, and repayment terms are crucial elements to evaluate, as they can significantly impact the overall cost of the loan. For instance, a loan with a lower interest rate may save you thousands of dollars in interest payments over the life of the loan.

To make a smart choice, it's vital to read and understand the loan agreement before signing. This document outlines the terms and conditions of the loan, including the interest rate, fees, and repayment schedule. Take the time to review the agreement carefully, and don't hesitate to ask questions if you're unsure about any aspect of the loan.

When comparing loan offers from different lenders, consider the following factors:

- Interest rates: Fixed or variable, and how they may change over time

- Fees: Origination fees, late payment fees, and other charges

- Repayment terms: Length of the repayment period, minimum payment amounts, and any flexibility in repayment schedules

By evaluating these factors, you can make a more informed decision and choose the loan that best fits your needs and financial situation.

Negotiating with lenders can also be an effective way to secure a better deal. If you have a good credit score or a co-signer with a strong credit history, you may be able to negotiate a lower interest rate or more favorable repayment terms. Additionally, some lenders may offer discounts or incentives for borrowers who make timely payments or pay their loans off early. Be sure to ask about these options when comparing loan offers and discussing the terms of your loan.

Ultimately, choosing the best private student loan requires careful consideration and research. By taking the time to evaluate your options, read and understand the loan agreement, and negotiate with lenders, you can make a smart decision and set yourself up for long-term financial success. Remember to stay organized, ask questions, and seek guidance if needed to ensure you're making the most of your private student loan.

Managing Private Student Loan Debt

When dealing with private student loan debt, it's essential to have a solid plan in place. Income-driven repayment plans can be a good option, as they allow you to make monthly payments based on your income and family size. For example, some private lenders offer plans that cap your monthly payments at a certain percentage of your income.

To manage your private student loan debt effectively, consider exploring loan forgiveness options. These options can help reduce the amount you owe, but they often come with specific requirements, such as working in a particular field or making a certain number of payments. Be sure to research and understand the terms and conditions of any loan forgiveness program.

Consolidating private student loans can be a viable option, but it's crucial to weigh the pros and cons. On the one hand, consolidation can simplify your payments and potentially lower your interest rate. On the other hand, you may lose certain benefits, such as interest rate discounts or loan forgiveness options.

Some key points to consider when deciding whether to consolidate your private student loans include:

- Interest rates: Will consolidating your loans result in a lower interest rate, or will it increase your overall cost?

- Fees: Are there any fees associated with consolidating your loans, and how will they impact your overall debt?

- Repayment terms: Will consolidating your loans result in a longer or shorter repayment period, and how will that affect your monthly payments?

Refinancing your private student loans is another option to consider. Refinancing can help you secure a lower interest rate, which can save you money over the life of the loan. However, refinancing may not always be the best option, especially if you have a low credit score or unstable income. When refinancing, be sure to shop around and compare rates from multiple lenders to find the best deal.

Creating a budget is a critical step in managing your private student loan debt. Start by tracking your income and expenses to see where your money is going. Then, prioritize your debt repayment by focusing on high-interest loans first. You can also consider using the snowball method, which involves paying off smaller loans first to build momentum and confidence.

To prioritize your debt repayment, consider the following tips:

- Make a list of all your debts, including the balance, interest rate, and minimum payment for each loan

- Identify the loans with the highest interest rates and prioritize those first

- Consider using a debt repayment app or spreadsheet to track your progress and stay organized

By following these strategies and tips, you can take control of your private student loan debt and create a plan for repayment. Remember to stay informed, shop around for the best rates, and prioritize your debt repayment to achieve financial freedom.

Alternatives to Private Student Loans

When it comes to funding your education, private student loans are not the only option. Exploring alternative funding options can help you avoid debt and make the most of your financial resources. For instance, scholarships and grants can provide a significant amount of money to cover tuition fees and living expenses.

Scholarships, grants, and work-study programs are excellent alternatives to private student loans. These options can be merit-based or need-based, and they often come with fewer strings attached. By researching and applying for these programs, you can reduce your reliance on private loans and minimize your debt burden.

Some examples of alternative funding options include:

- Federal Pell Grants, which provide need-based funding to undergraduate students

- Merit-based scholarships, which reward academic achievement and talent

- Work-study programs, which offer part-time jobs to help students cover living expenses

These options can be a great way to fund your education without taking on excessive debt.

Using personal savings or assistance from family and friends is another option to consider. This approach can help you avoid debt and interest payments, but it may also deplete your savings or put a strain on your relationships. It's essential to weigh the benefits and drawbacks of using personal savings or assistance from loved ones and make an informed decision.

In recent years, side hustles and entrepreneurship have emerged as a means to fund education expenses. By starting a part-time business or freelancing, you can earn money to cover tuition fees and living expenses. For example, you can offer tutoring services, pet-sitting, or social media management to clients in your area.

Some popular side hustles for students include:

- Online surveys and market research

- Selling products online through e-commerce platforms

- Offering services as a freelancer, such as writing or graphic design

These side hustles can help you earn a steady income and reduce your reliance on private student loans. By exploring alternative funding options and being creative with your finances, you can make the most of your educational experience and set yourself up for long-term financial success.

Frequently Asked Questions (FAQ)

What are the eligibility requirements for private student loans?

When it comes to private student loans, lenders consider several factors to determine eligibility. Credit score is a key factor, as it indicates an individual's creditworthiness and ability to repay the loan. A good credit score can increase the chances of approval and may also lead to more favorable interest rates.

Income is another important factor, as lenders want to ensure that borrowers have a stable source of income to repay the loan. This is particularly important for private student loans, as they often require repayment to begin immediately. For example, a student with a part-time job or a parent co-signer with a steady income may be more likely to be approved.

Enrollment status is also a crucial factor, as private student loans are typically only available to students who are enrolled at least half-time in a degree-granting program. To be eligible, students should check with their school's financial aid office to confirm their enrollment status. Here are some general eligibility requirements:

- Be a U.S. citizen or permanent resident

- Be enrolled at least half-time in a degree-granting program

- Have a good credit score, or a creditworthy co-signer

- Meet the lender's income requirements

In addition to these requirements, lenders may also consider other factors, such as the borrower's debt-to-income ratio and employment history. It's essential for students to review the lender's eligibility criteria before applying for a private student loan. By understanding the eligibility requirements, students can increase their chances of approval and find a loan that meets their needs.

Can I refinance my private student loans?

Refinancing private student loans can be a viable option for those looking to lower their interest rates or monthly payments. This process involves replacing an existing loan with a new one, typically with a lower interest rate or more favorable terms. By doing so, borrowers can potentially save money on interest over the life of the loan.

To refinance private student loans, you'll need to meet the lender's eligibility criteria, which often includes a good credit score and a stable income. Lenders may also consider factors such as your debt-to-income ratio and credit history when determining your creditworthiness. For example, a borrower with a credit score of 750 or higher may qualify for more competitive interest rates.

The refinancing options available to you will depend on the lender and their specific requirements. Some lenders may offer more flexible repayment terms or lower interest rates than others. Here are some key factors to consider when exploring refinancing options:

- Interest rates: Look for lenders offering lower interest rates than your current loan

- Repayment terms: Consider lenders with flexible repayment plans or longer loan terms

- Fees: Check for any origination fees or prepayment penalties associated with the new loan

When shopping for a refinancing lender, it's essential to compare rates and terms from multiple providers. You can use online tools or consult with a financial advisor to help you navigate the process. Additionally, be sure to review the fine print and ask questions before signing any new loan agreement.

By refinancing your private student loans, you can potentially simplify your finances and save money in the long run. However, it's crucial to carefully evaluate your options and choose a lender that meets your needs and financial situation. With the right lender and loan terms, you can take control of your debt and work towards a more stable financial future.

How do I apply for a private student loan?

To get started with applying for a private student loan, it's essential to research and choose a reputable lender. Applications are usually submitted online or through the lender's website, making it a convenient and straightforward process. Most lenders provide a simple and secure online application portal where you can fill out the required information.

Before submitting your application, make sure you have all the necessary documents and information readily available. This typically includes personal and financial details, such as your social security number, income, and credit score. You may also need to provide information about your school, including the cost of attendance and your expected graduation date.

Here are some key steps to follow when applying for a private student loan:

- Check your credit score and history to determine your eligibility and potential interest rate

- Gather all required documents and information before starting the application process

- Compare rates and terms from different lenders to find the best option for your needs

By following these steps and carefully reviewing the application process, you can increase your chances of getting approved for a private student loan. It's also a good idea to have a co-signer, such as a parent or guardian, if you have limited credit history.