As a young adult, managing finances can be challenging, and staying updated on the latest financial news is crucial. InCred Finance's acquisition of TruCap's gold loans business is a significant development that can impact your financial decisions. This acquisition can affect the way you think about gold loans and their role in your overall financial strategy.

The implications of this acquisition are far-reaching, and understanding them can help you make informed decisions about your financial future. For instance, the acquisition may lead to more competitive interest rates and better loan terms, making gold loans a more attractive option for young adults. This, in turn, can help you achieve your financial goals, such as paying for education or covering unexpected expenses.

Some key aspects to consider when evaluating the impact of this acquisition on your finances include:

- Changes in interest rates and loan terms

- Expansion of gold loan services to new areas

- Introduction of new loan products and services

By staying informed about these developments, you can make the most of the opportunities presented by InCred Finance's acquisition of TruCap's gold loans business and create a more secure financial future for yourself.

To navigate this new financial landscape, it's essential to assess your financial goals and priorities. Consider your short-term and long-term objectives, such as saving for a big purchase or building an emergency fund. By doing so, you can determine how the acquisition of TruCap's gold loans business by InCred Finance can help you achieve your goals and make the most of the available financial options.

Understanding Gold Loans

Gold loans are a type of secured loan where you can pledge your gold jewelry or coins as collateral to receive a loan amount. The loan amount is typically a percentage of the gold's value, and the interest rates vary depending on the lender and the loan term. For example, if you pledge gold worth $1,000, you may receive a loan of $800 with an interest rate of 10% per annum.

The repayment terms for gold loans can range from a few months to a few years, and you can repay the loan in installments or as a lump sum. It's essential to check the interest rates and repayment terms before taking a gold loan, as they can vary significantly between lenders. You should also consider the processing fees, which can range from 1% to 3% of the loan amount.

The benefits of gold loans include quick access to cash, minimal documentation, and no credit score checks. Here are some advantages of gold loans:

- Easy to qualify, even with a poor credit score

- Fast processing and disbursal of loan amount

- No restrictions on end-use of the loan amount

However, there are also risks associated with gold loans, such as the risk of losing your gold if you default on the loan.

For young adults, gold loans can be a convenient option for short-term financial needs or emergencies, such as paying for unexpected medical expenses or funding a wedding. Gold loans can provide quick access to cash, but it's crucial to borrow responsibly and repay the loan on time to avoid accumulating debt. You should also consider alternative options, such as personal loans or credit cards, before taking a gold loan.

To use gold loans effectively, you should only borrow what you need and repay the loan as soon as possible to minimize interest charges. You should also keep track of your repayment schedule and make timely payments to avoid defaulting on the loan. Additionally, you should consider the following tips:

- Check the gold valuation process to ensure you're getting a fair deal

- Compare interest rates and fees from different lenders

- Read the loan agreement carefully before signing

By being aware of the benefits and risks associated with gold loans, you can make informed decisions and use gold loans to meet your short-term financial needs.

Impact on Personal Finance

The recent acquisition of TruCap is likely to have a significant impact on the gold loan market. As a result, interest rates for borrowers may fluctuate, potentially becoming more competitive or increasing to balance out the new ownership structure. For instance, if the acquiring company has a different risk assessment model, it may lead to changes in the interest rates offered to borrowers.

Individuals with existing gold loans from TruCap may experience changes in their loan terms or repayment schedules. It is essential for these borrowers to review their loan agreements and understand any new terms or conditions that may apply. They should also be prepared to adapt to potential changes in interest rates or repayment terms, which could affect their monthly payments.

To navigate these changes, gold loan borrowers can take a few proactive steps:

- Review and understand the new loan terms and conditions

- Compare interest rates from different lenders to ensure they are getting the best deal

- Consider consolidating their debt or exploring alternative loan options if necessary

By being informed and prepared, young adults can make the most of the changing gold loan market and avoid any potential pitfalls.

As a young adult, it is crucial to stay up-to-date with the latest developments in the gold loan market and understand how they may impact your personal finance. This includes monitoring interest rates, loan terms, and any changes to the lending landscape. By doing so, you can make informed decisions about your financial situation and avoid any potential risks associated with gold loans.

In the event of changes to the gold loan market, young adults can take practical steps to protect their financial well-being. For example, they can create a budget and prioritize their debt repayments, or explore alternative investment options that are less volatile than gold. By being proactive and adaptable, young adults can navigate the changing gold loan market with confidence and make the most of the available financial opportunities.

Alternatives to Gold Loans

When it comes to short-term loan options, young adults often consider gold loans due to their relatively easy accessibility. However, there are other alternatives available that may offer more flexibility and competitive interest rates. For instance, personal loans and credit cards can be viable options for those in need of quick funds.

Personal loans, in particular, offer an attractive alternative to gold loans, with some lenders providing interest rates as low as 10-12% per annum. These loans can be repaid over a fixed tenure, ranging from a few months to several years, making them a more flexible option. Additionally, personal loans do not require collateral, unlike gold loans, which can be a significant advantage for borrowers.

Here are some key points to consider when evaluating alternatives to gold loans:

- Interest rates: Personal loans and credit cards often have higher interest rates compared to gold loans, but they offer more flexibility in terms of repayment tenure and loan amount.

- Flexibility: Credit cards, for example, offer a revolving credit line, allowing borrowers to withdraw and repay funds as needed, whereas personal loans provide a one-time disbursal of funds.

- Collateral: Gold loans require borrowers to pledge their gold jewelry or coins as collateral, whereas personal loans and credit cards are typically unsecured, eliminating the risk of losing valuable assets.

To choose the most suitable option, it's essential to assess your individual financial circumstances, including your income, expenses, and credit score. For example, if you have a good credit score, you may be eligible for a lower interest rate on a personal loan or credit card, making it a more attractive option. On the other hand, if you have a low credit score, a gold loan may be a more accessible option, despite the requirement for collateral.

Ultimately, it's crucial to weigh the pros and cons of each alternative and consider factors such as interest rates, fees, and repayment terms before making a decision. By doing so, you can make an informed choice that suits your financial needs and helps you achieve your goals. It's also important to remember that borrowing should be done responsibly, and it's essential to have a repayment plan in place to avoid debt traps and financial difficulties.

Budgeting with Debt

When dealing with debt, having a solid budget in place is crucial for getting back on track financially. This is especially true for debts like gold loans, which can have high interest rates and strict repayment terms. By creating a budget that accounts for loan repayments and interest, you can avoid missing payments and reduce the risk of accumulating more debt.

To create a budget that works for you, start by tracking your income and expenses to see where your money is going. Make a list of all your debts, including the balance, interest rate, and minimum payment for each one. This will help you understand how much you need to allocate for debt repayment each month.

Here are some tips for managing debt through budgeting:

- Prioritize your debts, focusing on the ones with the highest interest rates or the smallest balances first

- Consider consolidating multiple debts into a single loan with a lower interest rate

- Make sure to include a buffer in your budget for unexpected expenses, so you don't have to go further into debt when unexpected costs arise

Managing multiple debts can be overwhelming, but with a clear plan, you can stay on top of your payments and make progress towards becoming debt-free. For example, you can use the snowball method, where you pay off smaller debts first to build momentum, or the avalanche method, where you focus on the debts with the highest interest rates. Either way, the key is to stay consistent and make adjustments to your budget as needed.

In addition to prioritizing your debts, it's also important to consider the interest rates and fees associated with each loan. For gold loans, this may include interest rates, processing fees, and late payment charges. By understanding these costs, you can make informed decisions about how to allocate your budget and minimize the amount of interest you pay over time.

Financial Health and Planning

Building a stable financial foundation is crucial for young adults, and it starts with understanding the importance of emergency funds. Having a cushion of savings can help avoid the need for gold loans or other short-term debt, which often come with high interest rates and fees. For instance, setting aside 3-6 months' worth of living expenses in an easily accessible savings account can provide peace of mind and financial security.

Investing in financial education is also key to making better money management decisions. By learning about personal finance, investing, and money management, young adults can develop healthy financial habits and avoid costly mistakes. This can be as simple as reading personal finance books, attending webinars, or taking online courses to improve financial literacy.

Some essential topics to focus on when it comes to financial education include budgeting, saving, and investing. Young adults can start by:

- Creating a budget that accounts for all income and expenses

- Setting financial goals, such as saving for a down payment on a house or paying off student loans

- Exploring low-cost investment options, such as index funds or ETFs

By investing time and effort into financial education, young adults can make informed decisions and achieve long-term financial stability.

To get started, young adults can utilize online resources, such as budgeting apps, financial planning tools, and educational websites. For example, websites like NerdWallet, The Balance, and Investopedia offer a wealth of information on personal finance, investing, and money management. Additionally, taking advantage of employer-matched retirement accounts, such as 401(k) or IRA, can help young adults plan for the future and build a secure financial foundation.

Ultimately, developing good financial habits and planning for the future requires patience, discipline, and a willingness to learn. By prioritizing financial education and building an emergency fund, young adults can set themselves up for long-term financial success and avoid the need for costly short-term debt. With the right resources and tools, anyone can take control of their financial health and make informed decisions about their money.

Frequently Asked Questions (FAQ)

What happens to my existing TruCap gold loan after the acquisition?

If you're a TruCap gold loan customer, you might be wondering what the acquisition by InCred Finance means for your existing loan. The good news is that the terms of your loan should remain unchanged, so you can continue making payments as usual. However, it's always a good idea to review any communications from InCred Finance for updates on your loan.

To ensure a smooth transition, keep an eye on your email and postal mail for notifications from InCred Finance. They may send you updates on their systems, procedures, or contact information, so be sure to read these carefully. You can also log in to your online account or mobile app to check for any updates or changes.

Here are some key things to look out for:

- Changes to payment due dates or amounts

- Updates to interest rates or fees

- New contact information for customer support

By staying informed and reviewing any communications from InCred Finance, you can ensure that your loan continues to work for you without any disruptions. If you have any questions or concerns, don't hesitate to reach out to InCred Finance's customer support team for assistance.

Are gold loans a good option for short-term financial needs?

When it comes to covering short-term financial needs, many individuals consider various loan options. Gold loans, in particular, have gained popularity due to their relatively easy accessibility and minimal documentation requirements. By using gold as collateral, borrowers can quickly access the funds they need to address unexpected expenses or financial emergencies.

Gold loans can be a viable option for short-term needs, but it's essential to understand the interest rates and repayment terms before borrowing. Interest rates on gold loans can vary depending on the lender, loan amount, and loan tenure, so it's crucial to compare rates and terms from different lenders. For instance, some lenders may offer interest rates as low as 9%, while others may charge up to 24% or more.

To make an informed decision, consider the following factors:

- Interest rate: Look for lenders offering competitive interest rates to minimize your borrowing costs.

- Repayment terms: Choose a lender with flexible repayment options, such as monthly installments or bullet payments.

- Fees and charges: Check for any additional fees, such as processing fees, valuation fees, or late payment penalties.

By carefully evaluating these factors, you can determine whether a gold loan is suitable for your short-term financial needs and make a more informed borrowing decision.

Before taking out a gold loan, it's also important to assess your financial situation and ensure you can repay the loan within the specified tenure. Create a budget and prioritize your expenses to avoid defaulting on the loan, which can result in the lender seizing your gold collateral. By being mindful of your financial capabilities and the loan terms, you can use gold loans as a convenient and relatively affordable option for short-term financial needs.

How can I avoid needing a gold loan or other short-term debt?

Creating a safety net is essential to avoid relying on short-term debt solutions like gold loans. By setting aside a portion of your income each month, you can build an emergency fund to cover unexpected expenses. This fund will help you stay afloat during financial downturns, reducing the need for quick fixes.

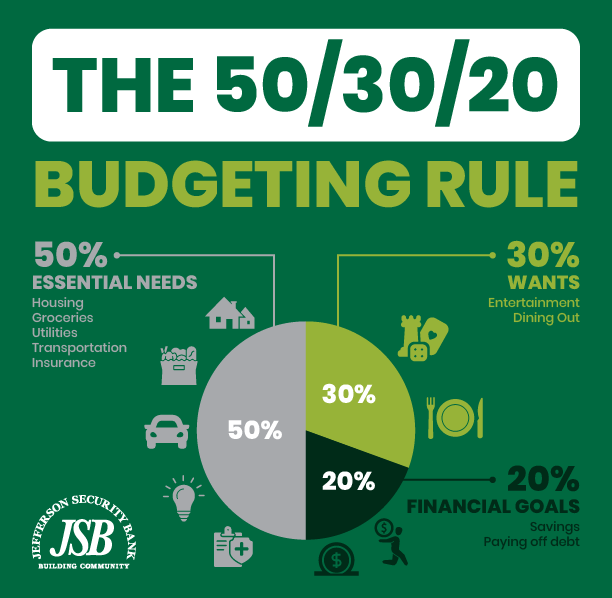

Maintaining a balanced budget is also crucial in minimizing the need for short-term loans. To achieve this, you should track your income and expenses, making sure that you're not overspending in any particular category. You can use the 50/30/20 rule as a guideline, allocating 50% of your income towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment.

Some practical ways to build your emergency fund include:

- Setting up automatic transfers from your checking account to your savings account

- Cutting back on non-essential expenses, such as dining out or subscription services

- Taking advantage of tax-advantaged savings options, like a high-yield savings account

By implementing these strategies, you can gradually build a cushion to fall back on when unexpected expenses arise.

In addition to building an emergency fund, it's essential to prioritize needs over wants and make conscious financial decisions. For example, instead of taking out a loan to finance a luxury item, consider saving up for it or exploring more affordable alternatives. By being mindful of your spending habits and making smart financial choices, you can reduce your reliance on short-term debt and achieve long-term financial stability.