As a young adult, managing your finances while pursuing higher education can be overwhelming, especially when it comes to student loans. With numerous options available, finding the best low-interest student loans can seem like a daunting task. By understanding the basics of student loans and exploring your options, you can make informed decisions about your financial future.

When searching for low-interest student loans, it's essential to consider factors such as interest rates, repayment terms, and fees. For instance, federal student loans often offer more favorable terms than private loans, with interest rates as low as 4.53% for the 2024-2025 academic year. Additionally, some lenders may offer discounts or rewards for good grades or automatic payments.

To get started, let's explore some key characteristics of low-interest student loans:

- Competitive interest rates that can help minimize your debt

- Flexible repayment terms that accommodate your financial situation

- Minimal fees that won't add to your overall debt burden

By considering these factors and doing your research, you can find a student loan that meets your needs and helps you achieve your academic goals without breaking the bank.

In this article, we'll delve into the world of low-interest student loans, providing you with practical tips and expert advice to help you make the best decision for your financial future. Whether you're a freshman or a graduate student, our guide will walk you through the process of finding and applying for the best low-interest student loans for 2025. With the right information and resources, you can take control of your finances and focus on what matters most – your education.

Understanding Low-Interest Student Loans

When it comes to financing your education, understanding the different types of student loans available is crucial. Federal and private student loans are the two main options, each with its own set of interest rates and benefits. Federal loans, for instance, typically offer more favorable terms, including lower interest rates and more flexible repayment plans.

To qualify for low-interest student loans, you'll need to meet certain requirements, such as credit score thresholds and income limits. Generally, a good credit score can help you secure better interest rates, while income thresholds may affect your eligibility for certain loan programs. For example, to qualify for a federal subsidized loan, you'll need to demonstrate financial need, which is determined by your family's income and other factors.

Some key benefits of federal loans include:

- Lower interest rates, which can save you thousands of dollars over the life of the loan

- More flexible repayment plans, including income-driven repayment options

- Forgiveness programs, such as Public Service Loan Forgiveness, which can help you discharge part or all of your loan balance

In contrast, private loans often come with higher interest rates and fewer benefits, but may still be a viable option if you've exhausted your federal loan eligibility.

If you're looking for low-interest student loan options, consider subsidized and unsubsidized federal loans, such as the Direct Subsidized Loan and the Direct Unsubsidized Loan. These loans offer competitive interest rates, currently ranging from 3.73% to 5.28%, and don't require a credit check. Additionally, some private lenders, like Discover and Sallie Mae, offer low-interest loan options with rates starting at around 4.5%.

To increase your chances of qualifying for low-interest student loans, it's essential to maintain a good credit score, typically above 650, and meet the income thresholds set by the lender or loan program. You can also consider applying for a co-signer, such as a parent or guardian, to help secure a better interest rate. By understanding the different types of student loans and their requirements, you can make informed decisions about your financial aid and set yourself up for long-term success.

Top Low-Interest Student Loan Providers

When it comes to funding your education, choosing the right student loan provider can make a significant difference in your financial journey. Popular providers like Sallie Mae and Discover offer competitive interest rates and flexible repayment terms. For instance, Sallie Mae offers variable interest rates as low as 2.50% and fixed interest rates as low as 4.50%, making it an attractive option for many students.

To make an informed decision, it's essential to review and compare the interest rates and terms of different providers. This includes considering factors such as origination fees, repayment options, and customer service. By doing your research, you can find a provider that aligns with your financial goals and needs.

Some of the key providers to consider include:

- Sallie Mae: Offers a range of repayment options, including deferred payment and interest-only payment plans

- Discover: Provides a cosigner release option after 36 months of consecutive on-time payments

- CommonBond: Offers a forbearance option for up to 24 months, allowing you to temporarily suspend payments

Each provider has its pros and cons, and it's crucial to weigh these factors before making a decision. For example, while Sallie Mae offers competitive interest rates, it may have stricter credit requirements.

In addition to interest rates and repayment options, it's also important to consider provider-specific benefits. For instance, some providers offer rewards programs or career support services to help you succeed in your field. By taking the time to research and compare different providers, you can find a student loan that meets your unique needs and sets you up for long-term financial success.

Repayment options are another critical aspect to consider when choosing a student loan provider. Look for providers that offer flexible repayment plans, such as income-driven repayment or graduated repayment. This can help you manage your debt and avoid defaulting on your loans. By choosing a provider with flexible repayment options, you can ensure a smoother transition into the workforce and a more stable financial future.

How to Apply for Low-Interest Student Loans

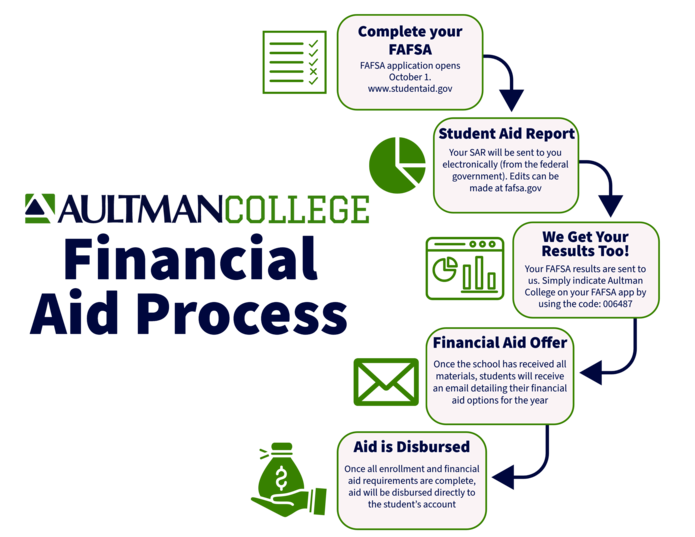

To get started with applying for low-interest student loans, it's essential to understand the process for federal student loans. The first step is to complete the Free Application for Federal Student Aid (FAFSA), which can be done online or by mail. This application will determine your eligibility for federal student loans, as well as other forms of financial aid.

The FAFSA requires you to provide personal and financial information, including your social security number, tax returns, and bank statements. You'll also need to list the schools you're interested in attending, as this information will be used to determine your eligibility for federal student loans. For example, if you're applying to multiple schools, you'll need to list each school's federal code on the FAFSA.

Once you've completed the FAFSA, you can begin exploring private student loan options. To apply for private student loans, you'll need to gather required documents, such as:

- Identification, like a driver's license or passport

- Proof of income, like pay stubs or tax returns

- Proof of enrollment, like an acceptance letter or transcript

These documents will be used to verify your identity and determine your eligibility for private student loans.

When comparing lender offers, it's crucial to review and understand the loan terms before signing. This includes the interest rate, repayment terms, and any fees associated with the loan. For instance, some lenders may offer a lower interest rate, but charge origination fees or have stricter repayment terms. Be sure to carefully review each lender's offer and ask questions if you're unsure about any aspect of the loan.

Before signing a loan agreement, make sure you understand the repayment terms, including the monthly payment amount, interest rate, and loan duration. It's also essential to review the loan's deferment and forbearance options, in case you need to temporarily suspend payments. By taking the time to carefully review and understand the loan terms, you can ensure you're making an informed decision and avoiding potential pitfalls.

Managing and Repaying Low-Interest Student Loans

When it comes to managing student loan debt, it's essential to understand the various strategies available to make repayment more manageable. Income-driven repayment plans, for instance, can help lower monthly payments based on income and family size. By exploring these options, borrowers can avoid financial strain and make progress on their loans.

One effective way to manage student loan debt is by taking advantage of income-driven repayment plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE). These plans can significantly reduce monthly payments, making it easier to stay on track with loan repayments. For example, a borrower with a $30,000 loan and an income of $40,000 may be eligible for a lower monthly payment through an income-driven plan.

In addition to income-driven plans, loan forgiveness programs can also provide relief for borrowers. These programs, such as Public Service Loan Forgiveness (PSLF), can forgive a portion or all of the loan balance after a certain number of qualifying payments. To be eligible, borrowers typically need to work in a specific field, such as education or healthcare, and make consistent payments.

To further reduce the burden of student loan debt, borrowers can take advantage of tax deductions and credits for student loan interest. The Student Loan Interest Deduction, for example, allows borrowers to deduct up to $2,500 in interest paid on qualified student loans. This can result in significant tax savings, especially for borrowers with high-interest loans.

Some key tax benefits for student loan borrowers include:

- Student Loan Interest Deduction: deduct up to $2,500 in interest paid on qualified student loans

- Lifetime Learning Credit: claim up to $2,000 in tax credits for education expenses

- American Opportunity Tax Credit: claim up to $2,500 in tax credits for education expenses

To avoid default and delinquency, it's crucial to set up automatic payments and communicate with lenders regularly. By doing so, borrowers can ensure timely payments and avoid late fees and penalties. Borrowers should also keep track of their loan balances, interest rates, and repayment terms to make informed decisions about their debt. By staying organized and proactive, borrowers can stay on top of their student loan debt and make progress towards financial freedom.

Lastly, borrowers should prioritize communication with their lenders to avoid any issues with repayment. This includes notifying lenders of changes in income, address, or employment status, as well as asking about available repayment options and assistance programs. By maintaining open communication and being proactive about loan repayment, borrowers can avoid default and delinquency and achieve long-term financial stability.

Alternatives to Traditional Student Loans

As a student, it's essential to explore alternative funding options to cover education expenses. Scholarships, grants, and work-study programs are excellent alternatives to traditional student loans, offering a more affordable and sustainable way to finance your education. For instance, the Federal Pell Grant is a need-based grant that can provide up to $6,495 for the 2022-2023 award year.

When searching for scholarships, consider using online platforms like Fastweb or Scholarships.com to find opportunities that match your profile. You can also check with your college or university to see if they offer any institutional scholarships or grants. Additionally, many organizations and companies offer scholarships to students who meet specific criteria, such as academic achievement or community service.

Income share agreements (ISAs) are another alternative to traditional student loans, where you agree to pay a percentage of your income after graduation in exchange for funding. The benefits of ISAs include flexible repayment terms and no accrued interest, but the drawbacks include potentially high repayment rates and limited provider options. Crowdfunding for education expenses is also an emerging trend, where you can use platforms like GoFundMe or Kickstarter to raise money from friends, family, and community members.

Some popular crowdfunding platforms for education expenses include:

- GoFundMe: A popular platform for personal fundraising campaigns

- Kickstarter: A platform focused on creative projects, but can also be used for education expenses

- Indiegogo: A platform that offers a range of fundraising options, including education expenses

These platforms often have fees associated with them, so be sure to research and understand the terms before launching a campaign.

Emerging trends in student loan financing include the use of blockchain technology and artificial intelligence to create more efficient and personalized lending platforms. For example, some companies are using blockchain to create transparent and secure lending networks, while others are using AI to offer personalized loan recommendations and financial guidance. As these innovations continue to evolve, it's essential to stay informed and explore the options that best fit your financial needs and goals.

Frequently Asked Questions (FAQ)

What is the difference between a subsidized and unsubsidized student loan?

As a student, navigating the world of student loans can be overwhelming, but understanding the basics is crucial for making informed decisions. One key distinction to grasp is the difference between subsidized and unsubsidized student loans. Subsidized loans are generally more desirable, as they offer more favorable terms for borrowers.

Subsidized loans do not accrue interest while the borrower is in school, whereas unsubsidized loans do. This means that with subsidized loans, the borrower will not have to pay interest on the loan until after they graduate or drop below half-time enrollment. For example, if you borrow $5,000 in subsidized loans as a freshman, you won't have to worry about interest accumulating on that amount until you finish school.

Here are some key characteristics of subsidized and unsubsidized loans:

- Subsidized loans are need-based, meaning you must demonstrate financial need to qualify.

- Unsubsidized loans are not need-based, and anyone can qualify, regardless of financial situation.

- Subsidized loans have lower interest rates compared to unsubsidized loans.

When it comes to managing your student loan debt, it's essential to prioritize subsidized loans, as they offer more benefits and flexibility. By understanding the differences between these two types of loans, you can make more informed decisions about your financial aid and create a plan for repayment that works for you.

To get the most out of your student loans, consider the following tips:

- Always prioritize subsidized loans over unsubsidized loans when given the option.

- Make interest payments on unsubsidized loans while in school to avoid capitalization.

- Explore income-driven repayment plans to manage your loan payments after graduation.

By being proactive and taking control of your student loan situation, you can set yourself up for long-term financial success and minimize the burden of debt.

Can I refinance my student loans to get a lower interest rate?

Refinancing your student loans can be a great way to save money on interest payments over time. By refinancing, you may be able to secure a lower interest rate, which can help reduce your monthly payments and free up more money in your budget. For example, if you currently have a loan with an interest rate of 6%, refinancing to a rate of 4% could save you hundreds of dollars per year.

To qualify for a lower interest rate when refinancing, you will typically need to have a good credit score and a steady income. Lenders use your credit score to determine how likely you are to repay your loan, so having a good score can help you qualify for better interest rates. A good credit score is generally considered to be 700 or higher, although this can vary depending on the lender.

Here are some tips to keep in mind when refinancing your student loans:

- Check your credit report to make sure it is accurate and up-to-date, as errors on your report can lower your credit score

- Pay down other debts to improve your debt-to-income ratio, which can also help improve your credit score

- Shop around and compare rates from multiple lenders to find the best deal for your situation

By following these tips and refinancing your student loans, you may be able to secure a lower interest rate and save money on your payments. It's also important to consider the terms of your new loan, including the repayment period and any fees, to make sure you're getting a good deal.

Are there any tax benefits for paying interest on student loans?

Paying interest on student loans can be a significant expense, but there is some good news. You may be eligible for a tax deduction on the interest paid on your student loans, up to a certain amount. This can help reduce your taxable income and lower your overall tax liability.

The tax deduction for student loan interest is available for both federal and private student loans, as long as the loan was used to pay for education expenses. To qualify, you must have paid interest on a qualified student loan during the tax year, and your income must be below certain thresholds. For example, if you paid $1,000 in interest on your student loan last year, you may be able to deduct that amount from your taxable income.

Here are the key details to keep in mind:

- The maximum deduction is $2,500 per year, or the actual amount of interest paid, whichever is less.

- The deduction is subject to income limits, which vary based on filing status and income level.

- You can claim the deduction even if you don't itemize your deductions on your tax return.

To claim the deduction, you'll need to complete Form 1098-E, which your lender should provide to you by January 31st of each year. You can then report the deduction on your tax return, using the amount shown on the form. It's a good idea to consult with a tax professional or financial advisor to ensure you're eligible and to get help with the process.