As a young adult, navigating the world of student loans can be overwhelming, especially with the numerous options available. To make informed decisions, it's essential to understand the different types of loans and their interest rates. For instance, federal loans often have more favorable interest rates compared to private loans.

When searching for low-interest student loans, it's crucial to consider factors such as repayment terms, fees, and borrower benefits. Some lenders offer perks like interest rate discounts or flexible repayment plans, which can make a significant difference in the long run. By doing your research and comparing different lenders, you can find the best fit for your financial situation.

Here are some key factors to look for in a low-interest student loan:

- Competitive interest rates

- Flexible repayment terms

- Low or no fees

- Borrower benefits, such as interest rate discounts or forbearance options

By evaluating these factors, you can make an informed decision and find a loan that aligns with your financial goals and needs. In this article, we'll delve into the best low-interest student loans available in 2025, providing you with the information you need to make smart financial choices.

Paying for education is a significant investment, and finding the right loan can help you achieve your academic and career goals without breaking the bank. With the right loan, you can focus on your studies and future career, rather than worrying about debt. By comparing and reviewing the best low-interest student loans, you can take the first step towards securing your financial future.

Understanding Low-Interest Student Loans

Low-interest student loans are a type of financial aid designed to help students cover the costs of higher education with more manageable repayment terms. These loans typically offer lower interest rates compared to other types of loans, which can significantly reduce the overall debt burden for students. By opting for low-interest student loans, students can allocate more of their monthly payments towards the principal amount, rather than just covering interest charges.

When it comes to student loans, there are two primary options: federal and private loans. Federal student loans are offered by the government and usually have lower interest rates and more flexible repayment terms. Private student loans, on the other hand, are offered by banks and other financial institutions, and may have higher interest rates and stricter repayment terms.

Some key differences between federal and private student loans include:

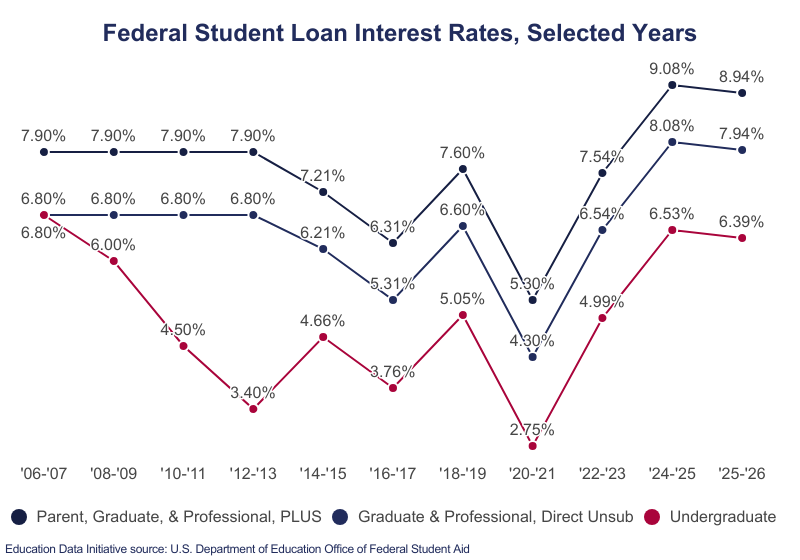

- Interest rates: Federal loans often have lower interest rates, ranging from 3.73% to 6.28%, while private loans can have interest rates ranging from 6% to 14% or more.

- Repayment terms: Federal loans offer more flexible repayment plans, including income-driven repayment and loan forgiveness options, while private loans may have stricter repayment terms.

- Loan limits: Federal loans have annual and aggregate loan limits, while private loans may have higher loan limits, but often require a co-signer.

To illustrate the impact of low-interest rates on monthly payments and total repayment amounts, consider the following example: a student borrows $30,000 at an interest rate of 4% versus 8%. With a 10-year repayment term, the monthly payment at 4% interest would be approximately $304, while the monthly payment at 8% interest would be around $344. Over the life of the loan, the student would pay a total of $36,413 at 4% interest, compared to $41,355 at 8% interest. This highlights the significant savings that can be achieved with low-interest student loans.

In practice, students can take advantage of low-interest student loans by exploring federal loan options, such as the Direct Subsidized and Unsubsidized Loans, and considering private loans with competitive interest rates and repayment terms. By doing their research and choosing the right loan options, students can set themselves up for long-term financial success and reduce their overall debt burden.

Top Low-Interest Student Loan Providers of 2025

When it comes to financing your education, finding a student loan with a low interest rate is crucial. The top low-interest student loan providers of 2025 offer competitive rates, flexible repayment options, and unique features that set them apart. Some of the notable providers include those that offer rates as low as 3.5% APR, making it easier for students to manage their debt.

The eligibility criteria for these providers vary, but most require a good credit score, a co-signer, or a steady income. For example, some providers offer loans to students with a minimum credit score of 650, while others require a co-signer with a good credit history. It's essential to review the eligibility criteria before applying to ensure you meet the requirements.

Here are some of the top low-interest student loan providers:

- College Ave: Offers low interest rates and flexible repayment options, including a 0.25% autopay discount

- Discover Student Loans: Provides low interest rates and no fees, with a rewards program for good grades

- Sallie Mae: Offers competitive interest rates and a range of repayment options, including a 0.25% autopay discount

Each provider has its unique features and benefits, such as flexible repayment options or forgiveness programs, which can help students manage their debt more effectively.

In addition to interest rates, it's essential to consider other factors, such as fees and customer service, when choosing a student loan provider. Some providers charge origination fees or late payment fees, which can add up over time. For instance, a provider that charges a 2% origination fee may not be the best option, even if it offers a low interest rate.

When evaluating providers, it's also crucial to consider the application process and the level of support offered. Some providers offer online applications and mobile apps, making it easy to manage your loan on the go. Others provide dedicated customer support, which can be helpful when you have questions or concerns about your loan. By considering these factors, you can make an informed decision and choose a provider that meets your needs.

How to Apply for Low-Interest Student Loans

To get started with the application process, it's essential to understand the difference between federal and private student loans. Federal loans typically offer more favorable terms and are often the best option for students. The first step is to fill out the Free Application for Federal Student Aid (FAFSA), which can be completed online or by mail.

Required documents for federal loans include tax returns, social security numbers, and proof of citizenship. Private lenders may also require these documents, as well as proof of income and credit history. It's crucial to review the required documents and deadlines carefully to ensure a smooth application process.

When applying for private loans, having a good credit score can significantly improve your chances of approval and help you qualify for lower interest rates. For example, a credit score of 700 or higher can lead to more favorable loan terms. To optimize your loan application, consider the following tips:

- Check your credit report for errors and work on improving your credit score

- Apply with a co-signer, such as a parent or guardian, to increase your chances of approval

- Compare rates and terms from multiple lenders to find the best option

Before accepting a loan offer, it's vital to review and understand the loan terms, including the interest rate, repayment period, and any fees associated with the loan. This will help you make an informed decision and avoid any potential pitfalls. For instance, a loan with a lower interest rate may seem appealing, but if it has a shorter repayment period, it could lead to higher monthly payments.

In addition to reviewing loan terms, it's also important to consider the repayment options and forgiveness programs available. Some loans may offer income-driven repayment plans or public service loan forgiveness, which can be beneficial for students pursuing careers in certain fields. By carefully evaluating these options and understanding the loan terms, you can make a more informed decision and set yourself up for long-term financial success.

Managing and Repaying Low-Interest Student Loans

When it comes to managing student loan debt, creating a budget is essential. Start by tracking your income and expenses to understand where your money is going, and then allocate a realistic amount towards your loan repayment. Consider using the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment.

Income-driven repayment plans can also be a helpful tool in managing student loan debt. These plans allow you to pay a percentage of your discretionary income towards your loans, rather than a fixed amount. For example, the Income-Based Repayment (IBR) plan caps your monthly payments at 10% or 15% of your discretionary income, depending on the type of loan you have.

Another option to consider is loan consolidation, which involves combining multiple loans into one loan with a single interest rate and repayment term. This can simplify your repayment process and potentially lower your monthly payments. However, it's essential to weigh the pros and cons before consolidating your loans, as it may not always be the best option. Some things to consider include:

- Interest rates: Will consolidating your loans result in a lower interest rate, or will it increase your overall interest paid over time?

- Repayment terms: Will consolidating your loans extend your repayment term, and if so, will it save you money in the long run?

- Benefits: Will consolidating your loans result in the loss of any benefits, such as forgiveness options or interest subsidies?

Refinancing student loans to a lower interest rate or extending repayment terms can also be a viable option. This can be especially helpful if you have a high-interest loan and can qualify for a lower interest rate with a different lender. For instance, if you have a loan with a 6% interest rate and can refinance it to a 4% interest rate, you could save a significant amount of money over the life of the loan. However, it's crucial to carefully review the terms and conditions of any refinancing offer to ensure it aligns with your financial goals.

If you're facing repayment difficulties, it's essential to communicate with your lender as soon as possible. They may be able to offer temporary hardship programs, such as deferment or forbearance, which can provide relief during difficult times. You can also seek assistance from non-profit credit counseling agencies or financial advisors who specialize in student loan debt. Additionally, some lenders offer assistance programs, such as:

- Loan deferment: Temporarily suspending loan payments due to financial hardship

- Loan forbearance: Temporarily reducing or suspending loan payments due to financial hardship

- Income-driven repayment plans: Adjusting your monthly payments based on your income and family size

Ultimately, managing and repaying low-interest student loans requires a combination of budgeting, strategic planning, and effective communication with lenders. By understanding your options and seeking assistance when needed, you can take control of your debt and work towards a more stable financial future. Remember to regularly review your loan terms and adjust your repayment strategy as needed to ensure you're on track to meet your financial goals.

Conclusion and Next Steps

As you finish reading this article, take a moment to reflect on the key takeaways. Finding the best low-interest student loans requires careful planning and research, and it's essential to consider factors such as interest rates, repayment terms, and fees. By doing your due diligence, you can save thousands of dollars in interest payments over the life of the loan.

To get started, make a list of your priorities, such as:

- Interest rate and repayment terms

- Fees associated with the loan

- Customer service and support

Having a clear understanding of what you're looking for will help you navigate the loan search process and make an informed decision.

If you're looking for additional guidance and support, don't hesitate to reach out to your school's financial aid office or online forums, where you can connect with other students and experts who have gone through the process. These resources can provide valuable insights and help you avoid common pitfalls, such as applying for loans with high interest rates or unfavorable repayment terms.

Now that you're equipped with the knowledge and tools to find the best low-interest student loans, it's time to take the next step. Start by researching and comparing different loan options, and don't be afraid to ask questions or seek advice from financial aid experts. By taking control of your loan search and application process, you can set yourself up for long-term financial success and make your educational goals a reality.

Frequently Asked Questions (FAQ)

What are the current interest rates for federal student loans in 2025?

To find the most up-to-date information on federal student loan interest rates, it's essential to visit the official Federal Student Aid website. This website provides a comprehensive overview of the current interest rates for different types of federal student loans. By checking the website regularly, you can stay informed about any changes to interest rates that may affect your loan repayments.

The Federal Student Aid website is a valuable resource for students and borrowers, offering a wealth of information on federal student loans, including interest rates, repayment options, and forgiveness programs. For example, you can use the website to compare interest rates for different loan types, such as Direct Subsidized Loans and Direct Unsubsidized Loans. This can help you make informed decisions about your loan options and repayment strategies.

Here are some steps to follow when checking the current interest rates for federal student loans:

- Visit the Federal Student Aid website and navigate to the section on interest rates

- Review the current interest rates for different types of federal student loans, including undergraduate and graduate loans

- Use the website's tools and resources to compare interest rates and estimate your monthly loan payments

By following these steps, you can stay up-to-date on the current interest rates for federal student loans and make informed decisions about your loan options and repayment strategies. Additionally, you can use online calculators and tools to estimate your loan payments and plan your budget accordingly.

Can I refinance my existing student loans to a lower interest rate?

Refinancing your existing student loans to a lower interest rate can be a great way to save money and simplify your finances. This process involves replacing your current loan with a new one that has a lower interest rate, potentially saving you thousands of dollars in interest payments over the life of the loan. By refinancing, you can also choose a new repayment term that works better for your budget.

When it comes to refinancing, both federal and private student loans are eligible, but they may have specific requirements and criteria. For example, some lenders may require a good credit score or a certain income level to qualify for refinancing. Additionally, you may need to have a steady income and a history of on-time payments to be eligible.

To get started with refinancing, you'll want to research and compare rates from different lenders. Some popular options include banks, credit unions, and online lenders, which may offer a range of interest rates and repayment terms. You can use online tools to compare rates and find the best option for your situation.

Here are some things to consider when refinancing your student loans:

- Check your credit score and history to determine if you're eligible for refinancing

- Compare interest rates and repayment terms from multiple lenders

- Consider working with a credit union or non-profit lender for potentially lower rates

- Read reviews and ask for referrals from friends or family members who have refinanced their loans

It's also important to note that refinancing federal student loans may cause you to lose certain benefits, such as income-driven repayment plans or loan forgiveness options. However, if you can qualify for a significantly lower interest rate, refinancing may still be a good option for you. Be sure to weigh the pros and cons carefully before making a decision.

Ultimately, refinancing your student loans to a lower interest rate can be a smart financial move, but it's essential to approach the process with caution and carefully consider your options. By doing your research and choosing the right lender, you can save money and take control of your student loan debt.

How do I know which low-interest student loan provider is best for me?

When it comes to finding a low-interest student loan provider, the options can be overwhelming. To make an informed decision, consider your individual financial situation, including your income, expenses, and debt obligations. This will help you determine how much you can afford to borrow and repay each month.

Your credit score also plays a significant role in determining the best provider for you, as it affects the interest rates you'll be offered. For example, if you have a good credit score, you may be eligible for lower interest rates and more favorable repayment terms. On the other hand, a poor credit score may limit your options and result in higher interest rates.

To compare and research different providers, start by making a list of your priorities, such as:

- Interest rates and fees

- Repayment terms and flexibility

- Customer service and support

- Eligibility criteria and requirements

This will help you evaluate each provider based on your specific needs and circumstances.

It's also essential to read reviews and testimonials from other borrowers to get a sense of their experiences with different providers. You can check out websites like NerdWallet or Credit Karma to find reviews and compare rates. Additionally, consider reaching out to friends, family, or a financial advisor for personalized advice and guidance.

Ultimately, the best low-interest student loan provider for you will depend on your unique financial situation and loan needs. By doing your research, comparing options, and prioritizing your needs, you can make an informed decision and find a provider that works for you. Remember to always carefully review the terms and conditions of any loan before signing, and don't hesitate to ask questions if you're unsure about anything.