As a young adult, managing finances can be overwhelming, especially when it comes to student loans. Low-interest student loans can be a game-changer, helping you save money on interest payments and focus on your education and career goals. By understanding the options available, you can make informed decisions about your financial future.

Paying off high-interest loans can be a significant burden, which is why low-interest student loans are essential for many students. For instance, a student with a $30,000 loan at 6% interest could save over $3,000 in interest payments over 10 years by switching to a 4% interest loan. This savings can be used for other essential expenses, such as textbooks, housing, or living expenses.

When exploring low-interest student loan options, consider the following key factors:

- Interest rates and repayment terms

- Fees associated with the loan

- Eligibility criteria and application process

By carefully evaluating these factors, you can find a low-interest student loan that suits your needs and helps you achieve financial stability. This, in turn, can reduce stress and allow you to focus on your studies and long-term goals.

Understanding Low-Interest Student Loans

When it comes to student loans, understanding the type of interest rate you're dealing with is crucial. Fixed interest rates remain the same over the life of the loan, while variable interest rates can fluctuate, potentially increasing your monthly payments. This difference can significantly impact your overall loan costs, making it essential to choose the right option.

Fixed interest rates offer predictability and stability, allowing you to plan your finances with confidence. On the other hand, variable interest rates may start lower but can rise over time, increasing your debt burden. For instance, a $30,000 loan with a fixed interest rate of 4% will always have the same monthly payment, whereas a variable rate loan may start at 3% but increase to 6% or more.

Federal student loans are generally considered a better option than private loans due to their numerous benefits. Some of the advantages of federal loans include:

- Income-driven repayment plans, which cap monthly payments at a percentage of your income

- Loan forgiveness options, such as Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness

- More flexible repayment terms and deferment options

These benefits can provide significant relief for students struggling to repay their loans.

In contrast, private student loans often lack these benefits and may have less favorable terms. Private loans may have higher interest rates, fewer repayment options, and stricter credit requirements. However, some private lenders may offer competitive interest rates and perks, such as cashback rewards or career support services.

Low-interest rates can save students thousands of dollars over the life of the loan. For example, a $20,000 loan with an interest rate of 3% will cost around $5,000 in interest over 10 years, while the same loan with an interest rate of 6% will cost around $7,000 in interest. By choosing a low-interest loan, students can reduce their debt burden and free up more money for other expenses, such as living costs or additional education.

Top Low-Interest Student Loan Options for 2025

When it comes to finding the best student loan options, interest rates play a significant role. For 2025, some of the top low-interest student loan lenders include SoFi, CommonBond, and Earnest, which offer competitive rates and flexible repayment terms. These lenders often provide variable and fixed interest rates, allowing borrowers to choose the option that works best for their financial situation.

In addition to interest rates, it's essential to review the terms and benefits of each lender. For example, SoFi offers career support and unemployment protection, while CommonBond provides academic assistance and a social impact focus. Earnest, on the other hand, offers a flexible repayment schedule and the option to skip one payment per year.

Some lenders offer unique benefits that can make a significant difference in a borrower's financial journey. These benefits may include:

- Career coaching and job placement assistance

- Academic support and tutoring services

- Repayment flexibility, such as income-driven repayment plans

- Forgiveness options for borrowers who work in certain fields, such as public service or non-profit

These benefits can help borrowers navigate their financial obligations and achieve long-term success.

Considering factors beyond just interest rates is crucial when choosing a student loan lender. Borrowers should also look at fees, repayment flexibility, and customer support. For instance, some lenders may charge origination fees or late payment fees, which can add up over time. By carefully evaluating these factors, borrowers can make informed decisions and find the best loan option for their needs.

To get started, borrowers can research and compare the interest rates and terms of different lenders. They can also read reviews and ask for recommendations from friends, family, or financial advisors. By taking the time to explore their options and consider multiple factors, borrowers can find a low-interest student loan that sets them up for financial success.

How to Qualify for Low-Interest Student Loans

When it comes to securing low-interest student loans, your credit score plays a significant role in determining the interest rate you'll qualify for. A good credit score can help you qualify for lower interest rates, which can save you thousands of dollars in interest payments over the life of the loan. For example, a credit score of 750 or higher can qualify you for interest rates as low as 4.5%, while a credit score of 650 or lower may result in interest rates of 7% or higher.

To build good credit, it's essential to make on-time payments, keep credit utilization low, and monitor your credit report for errors. You can also consider becoming an authorized user on a parent's credit card or taking out a small loan to establish a positive credit history. By building a good credit score, you can increase your chances of qualifying for low-interest student loans.

Applying with a cosigner, such as a parent or guardian, can also help you secure a lower interest rate. This is because the cosigner's credit score is taken into account when determining the interest rate, which can result in a lower rate if the cosigner has a good credit score. When applying with a cosigner, it's essential to consider the following:

- Choose a cosigner with a good credit score to increase your chances of qualifying for a low interest rate

- Understand the cosigner's responsibilities and obligations, including making payments if you're unable to

- Consider the potential impact on the cosigner's credit score if you're late or miss payments

Shopping around and comparing rates from different lenders is also crucial to finding the best deal. You can use online tools and websites to compare rates and terms from multiple lenders, including banks, credit unions, and online lenders. When comparing rates, consider the following factors:

- Interest rate: Look for the lowest interest rate available, considering both fixed and variable rates

- Fees: Consider any origination fees, late fees, or other charges associated with the loan

- Repayment terms: Choose a loan with flexible repayment terms, including deferment and forbearance options

By following these tips and considering your options carefully, you can increase your chances of qualifying for low-interest student loans and saving money on interest payments over the life of the loan. Remember to always review the terms and conditions of any loan before signing, and don't hesitate to ask questions or seek guidance if you're unsure about any aspect of the process.

Repayment Strategies for Low-Interest Student Loans

When it comes to managing low-interest student loans, one of the most effective strategies is to take advantage of income-driven repayment plans. Income-Based Repayment (IBR) and Pay As You Earn (PAYE) are two popular options that can help make monthly payments more affordable. For instance, IBR can cap your monthly payments at 10% or 15% of your discretionary income, depending on the type of loan you have.

These plans offer several benefits, including lower monthly payments and potential loan forgiveness after a certain period. To qualify, you'll need to meet specific income and family size requirements, so it's essential to review the eligibility criteria carefully. By doing so, you can ensure you're taking full advantage of the available benefits.

Refinancing or consolidating student loans can also be a viable option, but it's crucial to weigh the pros and cons before making a decision. Some key factors to consider include:

- Potential changes to interest rates, which could be higher or lower than your current rate

- Repayment terms, such as the loan duration and monthly payment amount

- Fees associated with refinancing or consolidating, which can add up quickly

For example, if you refinance a loan with a 4% interest rate to one with a 6% interest rate, you could end up paying more in interest over the life of the loan.

To pay off debt efficiently, creating a budget and prioritizing student loan payments is essential. Start by tracking your income and expenses to see where you can cut back on non-essential spending. Then, allocate as much as possible towards your student loans, focusing on the highest-interest loans first. You can also consider setting up automatic payments to ensure you never miss a payment.

By following these tips and exploring income-driven repayment plans, you can take control of your student loan debt and make progress towards financial freedom. Remember to regularly review your budget and repayment strategy to ensure you're on track to meet your goals. With patience, discipline, and the right approach, you can pay off your low-interest student loans and start building a stronger financial future.

Additional Tips for Managing Student Loan Debt

When it comes to managing student loan debt, one of the most important things to keep in mind is avoiding lifestyle inflation. As your income increases, it can be tempting to upgrade your lifestyle by spending more on luxuries, but this can hinder your debt repayment progress. Instead, consider allocating your extra funds towards your student loans to pay them off faster.

To allocate your income effectively, consider using the 50/30/20 rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment. This rule can help you prioritize your debt repayment and make sure you're making progress on your loans. For example, if you earn $4,000 per month, you would allocate $800 towards debt repayment.

In addition to allocating your income wisely, you can also take advantage of tax deductions and credits for student loan interest payments. To do this, you'll need to keep track of your interest payments throughout the year and claim them on your tax return. Some benefits of claiming these deductions include:

- Reducing your taxable income, which can lower your tax bill

- Increasing your refund, which can be put towards your loans

- Decreasing the amount of interest you owe over time

Another way to pay off your student loans faster is by using a side hustle or part-time job to increase your income. This can be as simple as freelancing, dog walking, or tutoring, and can provide a significant boost to your debt repayment efforts. For instance, if you earn an extra $500 per month from a side hustle, you can put that entire amount towards your loans, making a big dent in your balance over time.

By following these tips and staying committed to your debt repayment plan, you can pay off your student loans faster and start building a more stable financial future. Remember to stay disciplined, prioritize your debt repayment, and take advantage of any tax benefits or extra income opportunities that come your way. With time and effort, you can become debt-free and achieve your long-term financial goals.

Frequently Asked Questions (FAQ)

What is the current interest rate for federal student loans?

The interest rate for federal student loans is determined by the government and can change from year to year. For the current academic year, the interest rates for federal student loans have been set based on the May 10-year Treasury note auction. This means that borrowers can expect to pay a fixed interest rate for the life of their loan.

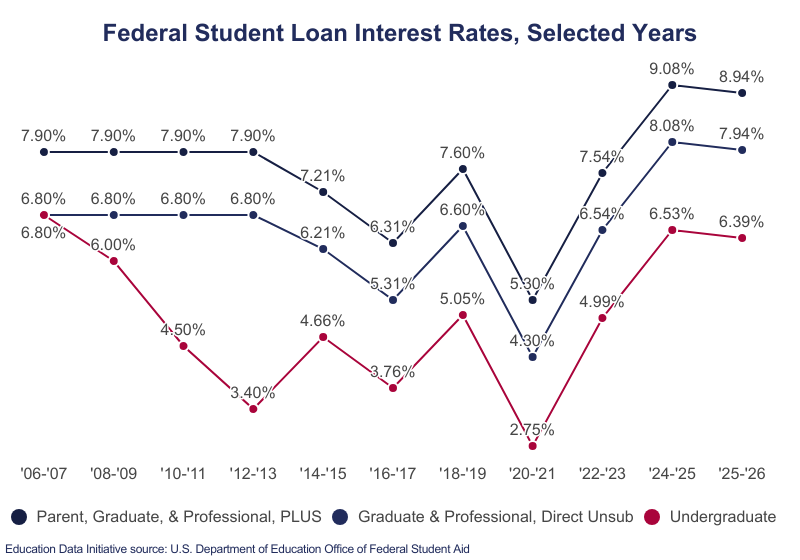

When it comes to federal student loans, there are several types of loans available, each with its own interest rate. The current interest rate for federal student loans varies depending on the type of loan and the borrower's credit score. For instance, Direct Subsidized and Unsubsidized Loans have the same interest rate, while PLUS Loans have a higher interest rate.

Here are some examples of the current interest rates for federal student loans:

- Direct Subsidized and Unsubsidized Loans: 4.99% for undergraduate students

- Direct Unsubsidized Loans: 6.54% for graduate students

- PLUS Loans: 7.54% for parents and graduate students

It's essential to note that these interest rates are subject to change, and borrowers should check the official government website for the most up-to-date information.

To give you a better idea of how interest rates work, let's consider an example. If you borrow $10,000 in Direct Subsidized Loans with an interest rate of 4.99%, you'll pay approximately $2,618 in interest over a 10-year repayment period. This highlights the importance of understanding the interest rate on your federal student loan and making timely payments to minimize the amount of interest you owe.

Can I refinance my student loans to get a lower interest rate?

Refinancing your student loans can be a great way to save money on interest and simplify your payments. By refinancing, you may be able to secure a lower interest rate, which can help reduce the overall cost of your loan. For example, if you have a $30,000 loan with an interest rate of 6%, refinancing to a rate of 4% could save you thousands of dollars in interest over the life of the loan.

When considering refinancing, it's essential to think about the potential impact on your repayment terms. Refinancing may change the length of your loan, the monthly payment amount, and the total interest paid. You'll want to carefully review the terms of your new loan to ensure it aligns with your financial goals and budget.

Here are some key factors to consider when refinancing your student loans:

- Interest rate: Will the new rate be lower than your current rate, and how much will you save in interest?

- Repayment term: Will the new loan have a shorter or longer repayment period, and how will that affect your monthly payments?

- Benefits: Will you lose any benefits, such as income-driven repayment or loan forgiveness, by refinancing your federal loans?

To get started with refinancing, you'll typically need to meet certain eligibility requirements, such as having a good credit score and a steady income. You can shop around and compare rates from different lenders to find the best option for your situation. Many lenders offer online tools and calculators to help you determine how much you could save by refinancing, making it easier to make an informed decision.

It's also important to note that refinancing may not be the best option for everyone, particularly if you have federal loans with beneficial repayment terms or forgiveness options. Before making a decision, take the time to weigh the pros and cons and consider your individual financial situation. By doing your research and carefully evaluating your options, you can make an informed decision about whether refinancing your student loans is right for you.

How do I know if I qualify for a low-interest student loan?

When considering a low-interest student loan, it's essential to understand the eligibility criteria. A good credit score is typically one of the primary requirements, as it demonstrates your ability to manage debt responsibly. For instance, a credit score of 700 or higher can significantly improve your chances of qualifying for a low-interest loan.

In addition to a good credit score, lenders often look for a stable income, as it indicates your capacity to repay the loan. A stable income can be from a full-time job, a part-time job, or even a freelance career, as long as it's consistent and reliable. This stability will help you make timely payments and avoid defaulting on the loan.

To give you a better idea, here are some key factors that lenders consider when evaluating your eligibility for a low-interest student loan:

- A good credit score, which can be achieved by making on-time payments and keeping credit utilization low

- A stable income, which can be demonstrated through pay stubs, tax returns, or other financial documents

- A low debt-to-income ratio, which shows that you're not overburdened with existing debt

If you're struggling to meet these criteria, you may want to consider applying with a creditworthy cosigner, such as a parent or guardian, to increase your chances of approval. This can be especially helpful if you're a student with limited credit history or a low income. By doing so, you can still access a low-interest student loan and start building your credit profile.