As a graduate navigating the world of finance, it's essential to understand the relationships between banks and Non-Banking Financial Companies (NBFCs). Banks have traditionally been cautious when lending to NBFCs, and this approach is rooted in the unique risks associated with these types of loans. For instance, NBFCs often have less stringent regulatory requirements, which can increase the likelihood of default.

The cautious approach taken by banks is also influenced by the potential consequences of lending to NBFCs. If an NBFC were to default on a loan, the bank could face significant losses, which would impact its own financial stability. To mitigate this risk, banks often impose stricter lending criteria on NBFCs, such as higher interest rates or more substantial collateral requirements.

Some key factors that contribute to the cautious approach include:

- Risk weight reversals, which can affect the bank's capital requirements and profitability

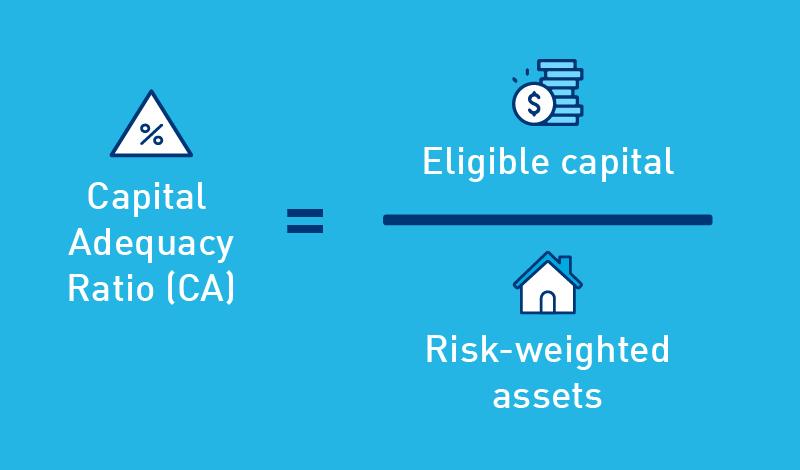

- Regulatory requirements, such as those related to capital adequacy and liquidity

- Historical default rates, which can inform the bank's lending decisions and risk assessments

By understanding these factors, graduates can better appreciate the complexities of bank lending and the importance of prudent risk management. This, in turn, can help individuals make more informed decisions about their own financial lives and careers in finance.

Banks must balance their desire to lend to NBFCs with the need to manage risk and maintain financial stability. This delicate balance is crucial in today's economic landscape, where access to credit is essential for growth and development. By exploring the cautious approach banks take when lending to NBFCs, we can gain a deeper understanding of the financial system and the ways in which risk is managed.

Understanding NBFCs and Their Role

Non-Banking Financial Companies, or NBFCs, are institutions that provide financial services without holding a bank license. They play a significant role in the financial sector by offering a range of services such as loans, credit cards, and insurance products. Examples of well-known NBFCs include Bajaj Finance, HDFC Ltd, and Mahindra & Mahindra Financial Services.

NBFCs have become increasingly important in recent years, especially for young adults who may not have access to traditional banking services. They offer consumer loans and credit products that can help individuals finance their education, purchase vehicles, or cover unexpected expenses. For instance, NBFCs like Lendingkart and Faircent provide personal loans and peer-to-peer lending options.

The impact of NBFCs on personal finance can be significant, as they provide access to credit for individuals who may not qualify for traditional bank loans. This can be especially helpful for young adults who are just starting to build their credit history. Some popular credit products offered by NBFCs include:

- Credit cards with rewards and cashback offers

- Personal loans with flexible repayment terms

- Education loans with low interest rates

The regulatory framework governing NBFCs is overseen by the Reserve Bank of India (RBI), which ensures that these institutions operate in a safe and sound manner. The RBI has established guidelines for NBFCs to follow, including minimum capital requirements, lending limits, and disclosure norms. These regulations help to protect consumers and maintain stability in the financial system.

In terms of operations and lending practices, NBFCs are required to follow strict guidelines to prevent risky lending and maintain asset quality. For example, NBFCs must verify the creditworthiness of borrowers and ensure that they have a stable income before approving loans. This helps to minimize the risk of default and ensures that borrowers are able to repay their loans.

To take advantage of NBFC services, young adults can research and compare different products and lenders to find the best options for their needs. It's also important to read and understand the terms and conditions of any loan or credit product before signing up. By being informed and responsible borrowers, individuals can use NBFCs to achieve their financial goals and build a strong credit history.

The Impact of Risk Weight Reversal on Lending

The concept of risk weight refers to the amount of capital that banks are required to hold against a particular type of loan. This weight is assigned based on the perceived risk of the loan, with higher-risk loans carrying a higher risk weight. As a result, banks must hold more capital against these loans, which can limit their ability to lend.

When the risk weight is reversed, it means that the perceived risk of a particular type of loan is decreased, allowing banks to hold less capital against these loans. This reversal can have a significant impact on banks' lending practices, particularly when it comes to lending to Non-Banking Financial Companies (NBFCs).

The reversal of risk weight can have several benefits for banks, including increased lending capacity and improved profitability. For NBFCs, the benefits include access to more funding options and lower borrowing costs. Some of the key benefits and drawbacks of this reversal for both banks and NBFCs include:

- Increased lending to NBFCs, which can lead to increased access to credit for borrowers

- Lower borrowing costs for NBFCs, which can be passed on to borrowers in the form of lower interest rates

- Potential for increased risk-taking by banks, which can lead to greater instability in the financial system

One of the potential drawbacks of the risk weight reversal is that it can lead to a decrease in the quality of loans made by banks. For example, if the risk weight on loans to NBFCs is decreased, banks may be more likely to lend to these companies without fully assessing their creditworthiness. This can lead to a higher likelihood of default, which can have negative implications for both banks and borrowers.

In the past, the reversal of risk weight has had a significant influence on lending decisions. For instance, during the 2008 financial crisis, many banks reversed their risk weights on mortgage-backed securities, which led to a surge in lending to the housing market. However, this ultimately contributed to the crisis, as many of these loans defaulted.

To navigate the implications of risk weight reversal, it's essential for borrowers to understand the potential benefits and drawbacks. For example, borrowers may be able to access credit at lower interest rates, but they should also be aware of the potential for increased risk-taking by banks. By understanding these factors, borrowers can make more informed decisions about their borrowing options.

The impact of risk weight reversal on lending practices can vary depending on the specific context and the institutions involved. For example, some banks may be more aggressive in their lending practices, while others may be more cautious. Similarly, some NBFCs may be more affected by the reversal than others, depending on their business models and funding needs.

Overall, the reversal of risk weight can have significant implications for both banks and NBFCs, as well as for borrowers. By understanding the potential benefits and drawbacks of this reversal, financial institutions and borrowers can make more informed decisions about their lending and borrowing options.

Navigating the Current Lending Landscape

As a young adult, navigating the current lending landscape can be overwhelming, especially with the numerous options available. It's essential to understand the different types of lenders, such as Non-Banking Financial Companies (NBFCs), which offer a range of loan products with varying interest rates and terms. To secure a loan from an NBFC, it's crucial to have a good credit history and a stable income.

When exploring alternative financing options, individuals and small businesses can consider peer-to-peer lending or crowdfunding. These platforms connect borrowers with investors, providing access to funds with more flexible terms. For instance, peer-to-peer lending platforms like Lending Club and Prosper offer personal loans with competitive interest rates, while crowdfunding platforms like Kickstarter and Indiegogo allow individuals to raise funds for specific projects.

The role of credit scores in determining loan eligibility and interest rates cannot be overstated. A good credit score can significantly improve one's chances of securing a loan with a favorable interest rate. To maintain a healthy credit score, it's essential to:

- Make timely payments on existing debts

- Keep credit utilization ratios low

- Monitor credit reports for errors or discrepancies

By following these tips, individuals can improve their creditworthiness and access better loan terms.

In addition to traditional lending options, alternative financing platforms are becoming increasingly popular. These platforms offer a range of benefits, including faster processing times and more flexible repayment terms. For example, invoice financing platforms like Fundbox and BlueVine provide small businesses with quick access to cash, while online lenders like SoFi and Upstart offer personal loans with competitive interest rates.

To make informed decisions when navigating the lending landscape, it's essential to research and compares different loan options. This includes considering factors such as interest rates, fees, and repayment terms. By taking the time to understand the different options available, individuals and small businesses can make smart financial decisions and achieve their goals.

Strategies for Managing Debt and Financial Health

Managing debt effectively is a crucial step towards achieving financial stability. To start, it's essential to create a budget that accounts for all your expenses, income, and debt payments. By tracking your spending, you can identify areas where you can cut back and allocate more funds towards debt repayment.

A key aspect of managing debt is debt consolidation, which involves combining multiple debts into a single loan with a lower interest rate and a longer repayment period. This strategy can simplify your payments and reduce the amount of interest you pay over time. For example, if you have multiple credit card debts with high interest rates, you can consolidate them into a personal loan with a lower interest rate.

Maintaining a healthy credit score is also vital for long-term financial stability. Your credit score determines the interest rates you'll qualify for on loans and credit cards, so it's essential to monitor it regularly. You can check your credit report for free once a year and dispute any errors that may be affecting your score.

To improve your financial health and reduce reliance on loans, consider starting a side hustle or exploring additional income streams. Some ideas include:

- Freelancing or consulting in a field you're skilled in

- Selling products online through e-commerce platforms

- Renting out a spare room on Airbnb or renting out your home on VRBO

- Participating in the gig economy through companies like Uber or Lyft

These side hustles can provide a much-needed boost to your income, allowing you to pay off debt faster and build up your savings.

In addition to debt consolidation and side hustles, it's essential to prioritize needs over wants when it comes to spending. Make a list of your essential expenses, such as rent, utilities, and food, and ensure you're covering those costs before spending on discretionary items. By being mindful of your spending habits and making conscious financial decisions, you can improve your financial health and achieve long-term stability.

Finally, remember that managing debt and achieving financial health is a marathon, not a sprint. It takes time, patience, and discipline, but with the right strategies and mindset, you can overcome debt and build a brighter financial future. By following these tips and staying committed to your goals, you can reduce your reliance on loans and achieve long-term financial stability.

Investing in a Cautious Lending Environment

In a cautious lending environment, it's essential to explore investment opportunities that are less affected by market fluctuations. Index funds or ETFs are excellent options, as they provide broad diversification and can be less volatile than individual stocks. For example, investing in a total stock market index fund can give you exposure to a wide range of companies, reducing your risk.

Diversification plays a crucial role in investment portfolios, as it helps to mitigate risk and increase potential returns. By spreading your investments across different asset classes, such as stocks, bonds, and real estate, you can reduce your reliance on any one particular investment. This can be especially important for young adults who are just starting to invest and may not have a lot of money to lose.

To get started with investing, you don't need a lot of money, and there are many ways to begin with minimal risk. You can start by investing small amounts of money each month, taking advantage of dollar-cost averaging to reduce the impact of market volatility. Some popular options for beginners include:

- Micro-investing apps that allow you to invest small amounts of money into a diversified portfolio

- Robo-advisors that provide automated investment management and diversification

- Online brokerage accounts that offer low-cost trading and minimal fees

When investing with small amounts of money, it's essential to keep costs low and be mindful of fees. Look for investment options with low expense ratios, and avoid accounts with high minimum balance requirements or excessive trading fees. By being mindful of these costs, you can help your money grow over time and achieve your long-term financial goals.

As a young adult, it's also important to take a long-term perspective when investing, rather than trying to time the market or make quick profits. By investing regularly and consistently, you can take advantage of compound interest and give your money the time it needs to grow. With patience and discipline, you can build a solid investment portfolio and achieve financial stability, even in a cautious lending environment.

Frequently Asked Questions (FAQ)

What are NBFCs and how do they differ from traditional banks?

Non-Banking Financial Companies, or NBFCs, play a vital role in the financial landscape by providing services similar to those offered by traditional banks. However, they operate under different regulations and do not possess a full banking license, which distinguishes them from their traditional counterparts. This key difference influences their operations and the types of services they can offer to customers.

NBFCs offer a range of financial services, including loans, credit facilities, and investment products, catering to diverse customer needs. They often specialize in specific areas, such as microfinance, housing finance, or gold loans, allowing them to focus on niche markets. By doing so, NBFCs can provide targeted solutions that might not be readily available through traditional banking channels.

The regulatory oversight of NBFCs differs significantly from that of traditional banks, with the former being primarily governed by the Reserve Bank of India (RBI) but under a different set of rules. This distinction affects the liquidity requirements, capital adequacy norms, and the types of financial products they can offer. For instance, NBFCs are not allowed to accept demand deposits, which restricts their ability to offer checking accounts like traditional banks do.

Some of the key features that distinguish NBFCs from traditional banks include:

- Limited product offerings due to regulatory restrictions

- Different capital requirements and liquidity norms

- Specialization in niche financial services or products

- Varying levels of regulatory oversight compared to traditional banks

Understanding these differences is crucial for individuals and businesses looking to engage with NBFCs for their financial needs, as it can impact the services available and the regulatory protections in place.

In practice, the difference between NBFCs and traditional banks can be seen in how they approach customer lending. NBFCs might have more flexible eligibility criteria or offer loans with unique features that are not typically found in traditional bank products. For example, an NBFC might offer a loan product specifically designed for small businesses or startups, which could include mentorship programs or business development support alongside the financial assistance.

How does the risk weight reversal affect my ability to get a loan from an NBFC?

When it comes to getting a loan from a Non-Banking Financial Company (NBFC), several factors come into play, including the risk weight reversal. This reversal may have a positive impact on your ability to secure a loan, as it can make banks more willing to lend to NBFCs. As a result, NBFCs may have more capital available to offer consumer loans, potentially increasing your chances of getting approved.

The risk weight reversal can be beneficial for individuals looking to borrow from NBFCs, as it can lead to more favorable lending terms. For instance, with more capital available, NBFCs may be able to offer lower interest rates or more flexible repayment options. This can be especially helpful for those who may not have been eligible for loans from traditional banks.

Some key benefits of the risk weight reversal for borrowers include:

- Increased access to credit, as NBFCs may be more willing to lend to a wider range of individuals

- Potentially lower interest rates, as NBFCs compete with banks to offer more attractive loan options

- More flexible repayment terms, such as longer loan tenures or lower monthly payments

To take advantage of these benefits, it's essential to research and compare loan options from different NBFCs, as well as traditional banks, to find the best fit for your financial needs. By doing so, you can make an informed decision and potentially secure a loan with more favorable terms.

What are some alternative financing options if I'm denied a loan from an NBFC?

If you're denied a loan from a non-banking financial company (NBFC), it's not the end of the road for your financing needs. Alternative options can provide the necessary funds, and it's essential to explore these choices. Peer-to-peer lending, for instance, allows you to borrow from individual investors, often with more flexible eligibility criteria.

These alternative financing options can be particularly useful for individuals with limited credit history or those who don't meet the traditional lending criteria. Crowdfunding is another option, where you can raise funds from a large number of people, typically through online platforms. This method can be used for various purposes, including personal finance products, business ventures, or specific projects.

Some of the alternative financing options you can consider include:

- Peer-to-peer lending: platforms like Lending Club and Prosper connect borrowers with individual investors

- Crowdfunding: websites like Kickstarter and Indiegogo allow you to raise funds from a large number of people

- Credit unions: member-owned cooperatives that offer more flexible interest rates and eligibility criteria for personal finance products

It's crucial to evaluate the terms and conditions of each alternative financing option carefully, considering factors like interest rates, repayment terms, and fees. By doing so, you can make an informed decision that suits your financial needs and goals.

When exploring alternative financing options, it's also essential to consider your credit score and history, as these can impact the interest rates and terms you're offered. For example, having a good credit score can help you qualify for better interest rates on peer-to-peer lending platforms or credit unions. By understanding your credit profile and shopping around for the best options, you can find the most suitable alternative financing solution for your needs.