When it comes to personal loans, having a clear understanding of how they are reviewed and rated is essential. Business Insider's methodology for reviewing personal loans is a great place to start, as it provides a comprehensive evaluation of various loan options. By grasping this methodology, individuals can make more informed financial decisions that suit their needs.

To get started, it's helpful to familiarize yourself with the key factors that Business Insider considers when reviewing personal loans. These factors typically include interest rates, fees, loan terms, and borrower requirements. Understanding these factors can help you compare different loan options and choose the one that best aligns with your financial goals.

Some of the key aspects of Business Insider's methodology include:

- Interest rate calculations, including APR and monthly payments

- Fees associated with the loan, such as origination fees and late payment fees

- Loan terms, including repayment periods and minimum credit score requirements

By considering these factors, you can gain a better understanding of what to expect from a personal loan and make a more informed decision about which loan to choose.

For example, if you're looking for a loan with a low interest rate, you may want to prioritize lenders that offer competitive APRs. On the other hand, if you're concerned about fees, you may want to opt for a lender that charges minimal or no fees. By taking the time to understand Business Insider's methodology and considering your own financial needs, you can find a personal loan that meets your requirements and helps you achieve your financial goals.

What is Business Insider's Personal Loan Review Methodology?

When it comes to evaluating personal loan providers, Business Insider uses a comprehensive review methodology. This approach considers several key factors, including interest rates and fees, to give borrowers a clear picture of what to expect. By examining these criteria, borrowers can make more informed decisions about their personal loan options.

The criteria used by Business Insider include:

- Interest rates and terms

- Fees associated with the loan

- Repayment flexibility and options

- Customer service and support

- Transparency and disclosure of loan terms

These factors help borrowers understand the total cost of the loan and what they can expect from the lender.

Transparency and disclosure are essential components of Business Insider's personal loan review methodology. Borrowers need to know exactly what they're getting into, including any potential fees or charges. For example, some lenders may charge origination fees or late payment fees, which can add up quickly if not properly disclosed.

By using Business Insider's methodology, borrowers can compare different personal loan providers and make informed decisions about which one is best for their needs. For instance, a borrower may prioritize a lender with lower interest rates, while another may value a lender with more flexible repayment terms. By considering these factors, borrowers can choose a personal loan that aligns with their financial goals and situation.

Business Insider's review methodology also helps borrowers avoid potential pitfalls, such as hidden fees or unclear loan terms. By providing detailed information about each lender, Business Insider enables borrowers to make educated decisions and avoid costly mistakes. This approach can save borrowers money and reduce financial stress in the long run.

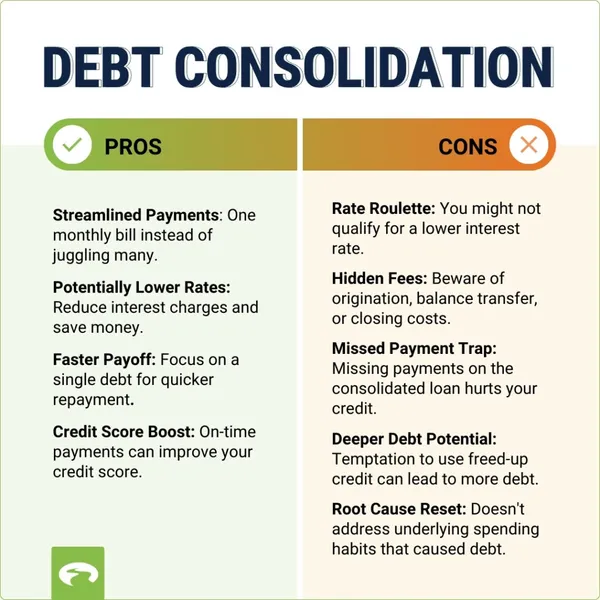

How to Use Personal Loan Reviews for Debt Consolidation

When considering debt consolidation, personal loans can be a viable option. By consolidating multiple debts into one loan, you can simplify your payments and potentially lower your interest rates. For instance, if you have multiple credit cards with high interest rates, you can consolidate them into a single personal loan with a lower interest rate, saving you money in the long run.

To choose the best personal loan for debt consolidation, it's essential to consider factors like credit score and loan terms. A good credit score can help you qualify for a lower interest rate, while loan terms will determine how long you have to repay the loan. You should also look for loans with flexible repayment terms and no prepayment penalties.

Here are some key factors to consider when selecting a personal loan for debt consolidation:

- Interest rates: Look for loans with lower interest rates to save money on interest payments

- Loan terms: Choose a loan term that fits your budget and repayment goals

- Fees: Be aware of any origination fees, late payment fees, or other charges associated with the loan

After consolidating your debt with a personal loan, it's crucial to manage your debt effectively to avoid falling into the same trap. Create a budget that accounts for your loan payments and stick to it. You can also set up automatic payments to ensure you never miss a payment. Additionally, consider cutting back on unnecessary expenses and using the 50/30/20 rule to allocate your income towards necessities, savings, and debt repayment.

To make the most of your personal loan, you should also prioritize debt repayment and avoid taking on new debt. Consider using the debt snowball method, where you pay off debts with the smallest balances first, or the debt avalanche method, where you pay off debts with the highest interest rates first. By following these tips and staying committed to your debt repayment plan, you can effectively manage your debt and achieve financial stability.

Comparing Personal Loan Providers for Financial Health

When it comes to comparing personal loan providers, there are several key factors to consider. Interest rates, fees, and repayment terms are crucial in determining the overall cost of the loan. For instance, a loan with a lower interest rate may seem appealing, but if it comes with high fees, it may not be the best option in the long run.

To get a comprehensive view of a personal loan provider, it's essential to read reviews and check ratings from reputable sources, such as the Better Business Bureau. This helps borrowers understand the lender's reputation, customer service, and overall satisfaction ratings. By doing so, borrowers can make informed decisions and avoid potential pitfalls.

Some of the key factors to consider when comparing personal loan providers include:

- Interest rates and APR

- Fees, such as origination fees and late payment fees

- Repayment terms, including the loan tenure and monthly payment amount

- Eligibility criteria, such as credit score and income requirements

- Customer service and support

By evaluating these factors, borrowers can find a personal loan that meets their financial needs and goals.

Comparing personal loan providers can help borrowers achieve financial health and stability in several ways. For example, by choosing a loan with a lower interest rate, borrowers can save money on interest payments over the life of the loan. Additionally, opting for a loan with flexible repayment terms can help borrowers manage their cash flow and avoid defaulting on payments.

In practice, comparing personal loan providers can be as simple as using online comparison tools or visiting the websites of different lenders. By doing their research and evaluating their options, borrowers can make informed decisions and find a personal loan that helps them achieve financial stability and peace of mind. This, in turn, can help borrowers build a stronger financial foundation and achieve their long-term financial goals.

Maximizing Budgeting with Personal Loan Reviews

When it comes to budgeting and financial planning, personal loan reviews can play a significant role in helping you create a budget and track expenses. By reviewing your personal loan options, you can get a better understanding of your financial situation and make informed decisions about your money. This can help you identify areas where you can cut back on unnecessary expenses and allocate your funds more efficiently.

To use personal loan reviews effectively, start by gathering all your financial documents, including your income statements, expense records, and debt obligations. Next, review your personal loan options and compare the interest rates, fees, and repayment terms to determine which one best suits your needs. You can then use this information to create a budget that accounts for your loan payments and other expenses.

Creating a budget is essential to maximizing your finances, and personal loan reviews can help you prioritize your needs over your wants. When making a budget, consider the 50/30/20 rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment. By prioritizing your needs, you can ensure that you're allocating your funds effectively and making the most of your personal loan.

Here are some tips for using personal loan reviews to identify areas for cost-cutting and savings:

- Review your expense records to identify areas where you can cut back on unnecessary expenses, such as dining out or subscription services.

- Compare your income and expenses to determine if there are any areas where you can reduce your spending and allocate more funds towards savings or debt repayment.

- Consider consolidating your debt into a single personal loan with a lower interest rate and more favorable repayment terms.

When considering a personal loan, it's essential to prioritize your needs over your wants to ensure that you're using the loan for essential expenses, such as paying off high-interest debt or covering unexpected expenses. For example, if you need to cover a medical emergency or car repair, a personal loan can provide the necessary funds to help you get back on your feet. By prioritizing your needs and using personal loan reviews to inform your budgeting decisions, you can make the most of your loan and achieve your financial goals.

By following these tips and using personal loan reviews to inform your budgeting decisions, you can create a more effective budget and achieve your financial goals. Remember to regularly review your budget and adjust as needed to ensure that you're staying on track and making the most of your personal loan. With the right budgeting strategy and personal loan, you can take control of your finances and achieve financial stability.

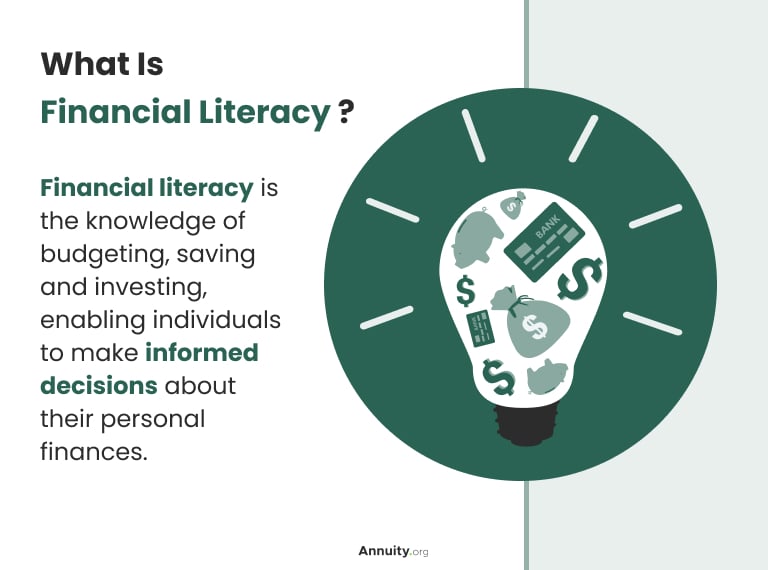

Investing in Financial Literacy with Personal Loan Knowledge

Investing in financial literacy is a crucial step in making informed decisions about personal loans and debt. By understanding the basics of personal finance, individuals can avoid common pitfalls and make smart choices that benefit their financial well-being. This knowledge can help borrowers navigate complex loan terms and conditions, avoiding costly mistakes.

Financial literacy is essential for managing debt effectively, and there are numerous resources available to help individuals learn and improve their skills. Online courses, such as those offered by Coursera and Udemy, provide comprehensive lessons on personal finance and debt management. Additionally, budgeting apps like Mint and You Need a Budget (YNAB) offer practical tools for tracking expenses and creating a budget.

Some key resources for learning about personal finance and debt management include:

- Online courses and tutorials on personal finance and debt management

- Budgeting apps and spreadsheet templates for tracking expenses

- Financial counseling services and non-profit credit counseling agencies

These resources can help individuals develop a deeper understanding of personal finance and make informed decisions about their financial lives.

Investing in financial literacy can lead to long-term financial health and stability by helping individuals avoid debt traps and make smart investment decisions. For example, understanding the difference between a fixed-rate and variable-rate loan can help borrowers choose the best option for their needs. By prioritizing financial education, individuals can create a stable financial foundation and achieve their long-term goals, such as buying a home or retiring comfortably.

Practical tips for investing in financial literacy include setting aside time each week to learn about personal finance, using budgeting apps to track expenses, and seeking guidance from financial advisors or counselors. By taking these steps, individuals can develop the knowledge and skills needed to navigate the complex world of personal finance and make informed decisions about their financial lives.

Frequently Asked Questions (FAQ)

What are the key factors to consider when choosing a personal loan provider?

When selecting a personal loan provider, it's essential to consider several key factors that can significantly impact your financial situation. Interest rates, for instance, can vary greatly between lenders, with some offering more competitive rates than others. For example, a lender may offer a rate of 6% APR, while another may charge 18% APR, resulting in significantly different monthly payments.

In addition to interest rates, fees associated with the loan should also be carefully evaluated. These can include origination fees, late payment fees, and prepayment penalties, which can add up quickly. Borrowers should review the loan agreement to understand all the fees involved and factor them into their decision.

Repayment terms are another crucial factor to consider, as they can affect your monthly cash flow and overall debt repayment strategy. Some lenders may offer more flexible repayment terms, such as longer loan periods or the option to make bi-weekly payments. It's essential to choose a repayment term that aligns with your financial goals and budget.

To choose the right personal loan provider, borrowers should consider the following factors:

- Interest rates and APR

- Fees, including origination and late payment fees

- Repayment terms, such as loan period and payment frequency

- Credit score requirements and how they impact interest rates

By carefully evaluating these factors, borrowers can make an informed decision and select a personal loan provider that meets their financial needs and goals. This can help them avoid costly mistakes and ensure a smoother debt repayment process.

Credit score requirements are also an essential consideration, as they can impact the interest rate offered and the borrower's ability to qualify for the loan. Generally, borrowers with higher credit scores are eligible for more favorable interest rates and terms. Therefore, it's crucial to check your credit score before applying for a personal loan and to choose a lender that offers competitive rates for your credit profile.

How can I use personal loan reviews to improve my financial health?

When considering a personal loan, it's essential to read reviews from other borrowers to get a sense of the lender's reputation and loan terms. Personal loan reviews can provide valuable insights into the application process, interest rates, and repayment terms, helping you make an informed decision. By reading reviews, you can avoid lenders with hidden fees or poor customer service.

To improve your financial health, personal loan reviews can help you identify areas for cost-cutting. For example, if you're currently paying high interest on a credit card, a personal loan with a lower interest rate could help you save money. By consolidating your debt into a single loan with a lower interest rate, you can free up more money in your budget for savings and investments.

Here are some ways personal loan reviews can help you create a budget that achieves financial stability:

- Compare interest rates and fees from different lenders to find the best deal

- Learn about repayment terms and options, such as flexible payment plans or autopay discounts

- Discover any additional features or benefits, such as credit score tracking or financial education resources

By considering these factors, you can create a budget that takes into account your loan payments and helps you achieve long-term financial stability.

Personal loan reviews can also provide tips and advice from other borrowers who have been in similar financial situations. For instance, you might learn about strategies for paying off your loan quickly, such as making extra payments or using a debt snowball method. By following these tips and creating a realistic budget, you can improve your financial health and achieve your long-term goals.

What are the benefits of consolidating debt with a personal loan?

Consolidating debt with a personal loan can be a game-changer for individuals struggling to manage multiple debts. By combining debts into one loan, you can simplify your payments and reduce the stress of keeping track of multiple due dates. This approach can also help you avoid missing payments, which can negatively impact your credit score.

One of the primary advantages of consolidating debt with a personal loan is the potential to reduce interest rates. If you have high-interest debts, such as credit card balances, consolidating them into a personal loan with a lower interest rate can save you money on interest charges over time. For example, if you have a credit card with an interest rate of 20% and you consolidate it into a personal loan with an interest rate of 10%, you can save 10% on interest charges.

Here are some benefits of consolidating debt with a personal loan:

- Simplify your payments by combining multiple debts into one loan with a single monthly payment

- Reduce interest rates by consolidating high-interest debts into a lower-interest personal loan

- Provide a clear path to becoming debt-free by creating a manageable repayment plan

By consolidating debt with a personal loan, you can create a manageable repayment plan and make progress towards becoming debt-free. It's essential to choose a personal loan with a repayment term that works for you and to make timely payments to avoid accumulating more debt.

To get the most out of consolidating debt with a personal loan, it's crucial to compare rates and terms from different lenders and choose a loan that meets your needs. You can also consider working with a financial advisor to create a personalized debt consolidation plan. By taking control of your debt and creating a plan to pay it off, you can achieve financial stability and peace of mind.