As a young adult, starting a business can be both exciting and intimidating, especially when it comes to managing finances. Short-term business loans can provide the necessary funding to get your business off the ground or help you navigate through a tough period. With the right loan, you can cover expenses such as rent, equipment, or payroll, and focus on growing your business.

For many young entrepreneurs, understanding the ins and outs of short-term business loans can be overwhelming, but it's essential to make informed decisions. A short-term business loan typically has a repayment period of less than a year, and the application process is often faster and more straightforward compared to traditional bank loans. This makes it an attractive option for young adults who need quick access to capital.

Some common uses of short-term business loans include:

- Covering unexpected expenses or emergencies

- Financing marketing campaigns or advertising efforts

- Purchasing inventory or equipment to meet demand

- Managing cash flow during slow periods

By understanding how short-term business loans work and how to use them effectively, young adults can set their businesses up for success and achieve their financial goals. Whether you're just starting out or looking to expand your existing business, short-term business loans can provide the necessary funding to help you take your business to the next level.

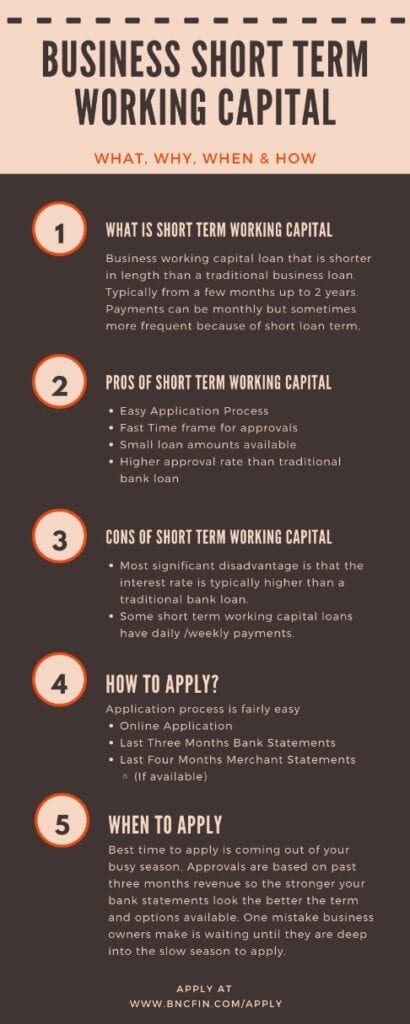

What are Short-Term Business Loans?

Short-term business loans provide companies with temporary access to capital, helping them cover immediate expenses or capitalize on new opportunities. These loans typically have a repayment period of less than a year, with some lasting only a few months. For example, a retail business might use a short-term loan to finance a holiday season marketing campaign or to manage inventory during a peak sales period.

The benefits of short-term business loans include quick access to capital, allowing businesses to respond rapidly to changing market conditions or unexpected expenses. Flexible repayment terms are also a key advantage, as they can be tailored to suit the business's cash flow and financial situation. This flexibility can be especially helpful for businesses with variable revenue streams, such as those in the food service or hospitality industries.

Some common examples of short-term business loans include lines of credit, invoice financing, and merchant cash advances. These products can be used to address a range of business needs, from managing cash flow and paying suppliers to investing in new equipment or marketing initiatives. By understanding the different types of short-term loans available, businesses can make informed decisions about which products best suit their needs.

To be eligible for a short-term business loan, companies typically need to meet certain requirements, including:

- A minimum credit score, which can vary depending on the lender and loan product

- A established business history, which may involve providing financial statements and tax returns

- A clear plan for using the loan proceeds and repaying the debt

Lenders may also consider other factors, such as the business's revenue, cash flow, and industry, when evaluating loan applications. By carefully reviewing these requirements and preparing a solid application, businesses can increase their chances of securing a short-term loan and achieving their financial goals.

In terms of practical tips, businesses should carefully review the terms and conditions of any loan before applying, including the interest rate, fees, and repayment schedule. It's also essential to have a clear plan for using the loan proceeds and repaying the debt, as well as a backup plan in case the business encounters unexpected financial challenges. By being proactive and prepared, businesses can use short-term loans to drive growth and success, while minimizing the risks associated with borrowing.

Types of Short-Term Business Loans

When it comes to short-term business loans, there are several options available to help businesses achieve their goals. A line of credit is one popular option, which provides businesses with access to a set amount of funds that can be drawn upon as needed. This type of loan is ideal for businesses that need to manage cash flow or cover unexpected expenses.

Lines of credit typically come with variable interest rates and fees, which can add up quickly if not managed properly. For example, a business may be charged a monthly maintenance fee, as well as interest on the outstanding balance. It's essential to carefully review the terms and conditions before applying for a line of credit.

Another type of short-term loan is invoice financing, which allows businesses to borrow against outstanding invoices. This option is ideal for businesses that have a high volume of accounts receivable and need to improve cash flow.

- Invoice financing can provide businesses with quick access to funds, often within 24 hours

- It can help businesses to pay employees, suppliers, and other expenses on time

- However, it can be more expensive than other types of loans, with fees ranging from 1-5% of the invoice value

For instance, a freelance writer may use invoice financing to borrow against outstanding invoices from clients, allowing them to pay their own bills on time.

Other types of short-term loans include merchant cash advances, which provide businesses with a lump sum of cash in exchange for a percentage of future sales.

- Merchant cash advances can be a good option for businesses with a high volume of credit card sales

- They can provide quick access to funds, often within a few days

- However, they can be more expensive than other types of loans, with interest rates ranging from 20-50% APR

A small retail business, for example, may use a merchant cash advance to cover the cost of new inventory or equipment.

Ultimately, the right type of short-term loan will depend on the specific needs and goals of the business. By carefully considering the pros and cons of each option, businesses can make informed decisions and achieve their goals. It's essential to shop around and compare rates and terms from different lenders to find the best deal.

How to Choose the Best Short-Term Business Loan

When it comes to choosing the best short-term business loan, it's essential to evaluate and compare different options carefully. This involves considering several key factors that can impact the overall cost and affordability of the loan. By taking a step-by-step approach, you can make an informed decision that meets your business needs.

First, consider the interest rates offered by different lenders, as these can vary significantly. For example, a loan with an interest rate of 10% may seem attractive, but if it comes with high fees, it may not be the best option in the long run. Look for lenders that offer competitive interest rates and transparent fee structures.

Some key factors to consider when evaluating short-term loan options include:

- Interest rates and fees, including any origination fees or late payment charges

- Repayment terms, including the loan tenure and frequency of payments

- Collateral requirements, if any, and the potential risks involved

These factors can have a significant impact on the overall cost of the loan and your ability to repay it.

To negotiate the best possible terms, it's essential to do your research and compare offers from different lenders. Consider working with a lender that offers flexible repayment terms or a line of credit that can be drawn upon as needed. You can also try to negotiate the interest rate or fees, especially if you have a good credit score or a long-standing relationship with the lender.

In addition to negotiating the best terms, it's also important to avoid common pitfalls, such as hidden fees or unrealistic repayment schedules. Be sure to read the fine print carefully and ask questions if you're unsure about any aspect of the loan. By taking a careful and informed approach, you can find a short-term business loan that meets your needs and helps your business thrive.

Finally, consider seeking advice from a financial advisor or accountant if you're unsure about the best loan option for your business. They can help you evaluate your financial situation and make a recommendation based on your specific needs and goals. With the right loan and a solid repayment plan, you can achieve your business objectives and set yourself up for long-term success.

Top Short-Term Business Loan Providers in September 2025

When it comes to short-term business loans, there are numerous providers to choose from, each with their unique features and benefits. For instance, Fundbox and BlueVine are popular options that offer lines of credit and invoice financing, allowing businesses to access funds quickly. These loans are ideal for businesses that need to cover unexpected expenses or manage cash flow.

The interest rates, fees, and repayment terms offered by each provider vary significantly, and it's essential to compare these before making a decision. Some providers, like Square Capital and PayPal Working Capital, offer competitive interest rates and flexible repayment terms, while others, such as Lending Club and Funding Circle, may have higher interest rates but more comprehensive loan options.

- Fundbox: 10.5% - 79.9% APR, 12-24 weeks repayment term

- BlueVine: 15% - 78% APR, 6-12 months repayment term

- Square Capital: 10% - 16% APR, 18 months repayment term

The application process and requirements for each provider also differ, with some requiring extensive documentation and others offering a more streamlined process. For example, online lenders like OnDeck and Kabbage often have a faster application process, typically requiring only basic business and financial information, while traditional banks may require more detailed financial statements and a longer application process. It's crucial to review the requirements and application process before choosing a provider to ensure the best fit for your business needs.

To get the most out of a short-term business loan, it's essential to carefully review the terms and conditions, including any fees or penalties for early repayment or late payments. By doing so, businesses can make informed decisions and avoid potential pitfalls, such as accumulating debt or damaging their credit score.

- Check the APR and fees associated with the loan

- Review the repayment terms and schedule

- Understand any penalties or fees for early repayment or late payments

In conclusion, selecting the right short-term business loan provider can be a daunting task, but by comparing the features, benefits, and terms of each provider, businesses can make an informed decision that meets their unique needs. By considering factors such as interest rates, fees, and repayment terms, businesses can find a loan that helps them achieve their goals without breaking the bank.

Managing Debt and Repaying Short-Term Business Loans

When it comes to managing debt and repaying short-term business loans, having a solid plan in place is crucial. This starts with creating a budget that accounts for all of your business expenses, including loan repayments. By prioritizing your spending and making timely payments, you can avoid falling behind on your debts.

Budgeting and cash flow management are essential strategies for managing debt and repaying short-term business loans. This involves tracking your income and expenses, identifying areas where you can cut back, and allocating sufficient funds for loan repayments. For example, you can use the 50/30/20 rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment.

Making timely payments is vital to avoiding late fees and penalties, which can quickly add up and increase the overall cost of your loan. To stay on track, consider setting up automatic payments or reminders to ensure you never miss a payment. Additionally, be sure to review your loan agreement carefully to understand the terms and conditions of your loan, including the interest rate and repayment schedule.

To build credit and improve your financial health over time, consider the following tips:

- Make all payments on time, every time, to demonstrate your creditworthiness

- Keep your credit utilization ratio low, ideally below 30%

- Monitor your credit report regularly to ensure it is accurate and up-to-date

- Avoid taking on too much debt, as this can negatively impact your credit score

By following these tips and maintaining good credit habits, you can improve your financial health and increase your access to credit in the future.

In addition to making timely payments, it's also important to communicate with your lender if you're experiencing financial difficulties. Many lenders offer flexible repayment options or temporary hardship programs that can help you get back on track. Don't be afraid to reach out to your lender if you need assistance, as they may be willing to work with you to find a solution.

Frequently Asked Questions (FAQ)

What are the typical interest rates for short-term business loans?

When exploring short-term business loan options, it's essential to understand the associated interest rates. Interest rates vary by lender and loan type, but typically range from 10-30% APR. This range can help you prepare for the potential costs of borrowing.

To give you a better idea, here are some common short-term business loan types and their corresponding interest rates:

- Merchant cash advances: 20-30% APR

- Invoice financing: 10-20% APR

- Line of credit: 10-25% APR

These rates can fluctuate depending on your business's creditworthiness, industry, and loan term.

It's crucial to factor in these interest rates when calculating the total cost of your loan. For instance, if you borrow $10,000 at an APR of 20% for 6 months, you'll end up paying around $11,219, including interest. This example illustrates the importance of carefully reviewing loan terms before signing an agreement.

To make an informed decision, research and compare rates from multiple lenders, considering factors such as repayment terms, fees, and loan amounts. By doing so, you can find the most suitable short-term business loan for your needs and avoid excessive interest charges.

How quickly can I get approved for a short-term business loan?

When it comes to getting approved for a short-term business loan, time is often of the essence. Approval times can vary significantly depending on the lender and the specific loan product. Some lenders may take several days or even weeks to review and approve an application, while others can provide a decision much more quickly.

Many lenders specialize in providing rapid approval and funding for short-term business loans. These lenders often use streamlined online application processes and may not require as much documentation as traditional lenders. This can help to speed up the approval process and get businesses the funding they need more quickly.

Some lenders offer same-day or next-day approval for short-term business loans, which can be a huge advantage for businesses that need to act quickly. To take advantage of these rapid approval options, it's a good idea to:

- Have all necessary documentation ready before applying, such as business financial statements and tax returns

- Choose a lender that offers online applications and rapid approval

- Be prepared to provide additional information or answer questions from the lender to help speed up the process

By doing some research and preparing in advance, businesses can increase their chances of getting approved for a short-term business loan quickly and easily. It's also important to carefully review the terms and conditions of any loan before accepting it, to make sure it's a good fit for the business's needs. With the right lender and some advance preparation, businesses can get the funding they need to succeed.

Can I use a short-term business loan for personal expenses?

When considering a short-term business loan, it's essential to understand the intended use of these funds. Short-term business loans are designed to help businesses cover immediate expenses, such as payroll or inventory costs, and should not be used for personal expenses. This is because lenders typically require borrowers to provide a business plan and financial projections to demonstrate how the loan will be repaid.

Using a short-term business loan for personal expenses can lead to financial trouble and potentially harm your credit score. For instance, if you use a business loan to pay for a vacation or personal debt, you may struggle to repay the loan, which can damage your business's financial reputation. It's crucial to keep personal and business finances separate to avoid any potential risks.

Here are some examples of acceptable uses for a short-term business loan:

- Covering unexpected business expenses, such as equipment repairs or utility bills

- Financing inventory or supplies for a busy sales period

- Meeting payroll obligations during a slow sales period

It's essential to review the loan agreement and understand the terms and conditions before accepting a short-term business loan. By using these funds for legitimate business purposes, you can help your business thrive and avoid any potential financial pitfalls.

If you're struggling to manage personal expenses, it's recommended that you explore alternative options, such as a personal loan or credit counseling services. These options can provide you with the necessary support to get your personal finances back on track without jeopardizing your business's financial health. By keeping your personal and business finances separate, you can maintain a healthy financial balance and make informed decisions about your business's growth and development.