The Reserve Bank of India (RBI) has taken a significant step towards supporting micro and small businesses by removing prepayment penalties on floating rate loans. This decision is expected to provide relief to many businesses that were struggling with high interest rates and rigid repayment terms. By doing so, the RBI aims to promote entrepreneurship and economic growth.

For micro and small businesses, this decision can be a game-changer, as it allows them to repay their loans ahead of schedule without incurring additional charges. This can be particularly beneficial for businesses that experience a surge in cash flow or want to refinance their loans at a lower interest rate. As a result, businesses can now make more informed decisions about their loan repayment strategies.

Some key benefits of this decision include:

- Reduced debt burden: Businesses can now repay their loans early without incurring prepayment penalties, which can help reduce their overall debt burden.

- Increased flexibility: The removal of prepayment penalties provides businesses with more flexibility in managing their cash flows and loan repayment schedules.

- Improved financial planning: Businesses can now plan their finances more effectively, as they have more control over their loan repayment terms and interest rates.

This move is expected to have a positive impact on the overall economy, as it can lead to increased lending and borrowing activity among micro and small businesses. By providing more favorable loan terms, the RBI is encouraging businesses to invest and grow, which can ultimately contribute to economic growth and development.

Understanding the RBI's Decision

The Reserve Bank of India (RBI) has made a significant move to waive prepayment penalties for micro and small business loans. This decision aims to provide relief to small businesses and entrepreneurs who often struggle with high interest rates and rigid loan terms. By waiving prepayment penalties, the RBI hopes to encourage borrowers to repay their loans early, thereby reducing their overall debt burden.

For borrowers with floating rate loans, this decision can be particularly beneficial. When interest rates fall, borrowers with floating rate loans can benefit from lower monthly payments, but they often face penalties for prepaying their loans. The RBI's decision to waive prepayment penalties allows these borrowers to take advantage of lower interest rates without incurring additional costs.

Some key benefits of this decision include:

- Reduced debt burden for small businesses and entrepreneurs

- Increased flexibility in loan repayment options

- Opportunities to take advantage of lower interest rates without incurring penalties

This move can help small businesses and entrepreneurs to better manage their finances and make informed decisions about their loan repayments. For example, a small business owner with a floating rate loan can now consider prepaying their loan when interest rates fall, without worrying about incurring penalties.

The potential benefits for small businesses and entrepreneurs are significant. By waiving prepayment penalties, the RBI is providing them with more flexibility and autonomy to manage their loan repayments. This can help to reduce their debt burden, improve their cash flow, and increase their overall financial stability. As a result, small businesses and entrepreneurs can focus on growing their businesses, rather than struggling with rigid loan terms and high interest rates.

In practical terms, this decision can help small businesses and entrepreneurs to save money on interest payments and reduce their financial risks. For instance, a small business owner who takes out a loan of Rs 10 lakhs with a floating interest rate of 12% per annum can save up to Rs 1 lakh in interest payments over the loan tenure by prepaying their loan when interest rates fall. This can be a significant saving for a small business, and can help to improve their overall financial health.

Impact on Small Businesses and Borrowers

The removal of prepayment penalties can have a significant impact on small businesses and borrowers, allowing them to reduce their debt burdens more efficiently. This change can be especially beneficial for small businesses that need to manage their cash flow carefully, as they can now pay off loans earlier without incurring additional fees. By doing so, they can free up more resources for investment and growth.

For borrowers, the removal of prepayment penalties can be a game-changer in certain scenarios, such as when interest rates drop or when they receive a lump sum of money. For instance, if a borrower takes out a loan with a high interest rate and later finds a better deal, they can now refinance their loan without facing penalties. This can lead to significant savings over the life of the loan.

Some examples of scenarios where borrowers can benefit from this decision include:

- Refinancing a loan to take advantage of lower interest rates

- Paying off a loan early after receiving a tax refund or inheritance

- Consolidating multiple loans into a single, lower-interest loan

In these situations, the removal of prepayment penalties can provide borrowers with more flexibility and options for managing their debt.

The potential implications for loan repayment strategies are also significant, as borrowers can now focus on paying off their loans as quickly as possible without worrying about penalties. This can involve making extra payments or using the snowball method to pay off loans with the highest interest rates first. By taking a proactive approach to loan repayment, borrowers can save money and achieve financial freedom more quickly.

Ultimately, the removal of prepayment penalties can be a powerful tool for small businesses and borrowers looking to reduce their debt burdens and achieve financial stability. By understanding the implications of this change and taking advantage of the opportunities it presents, borrowers can make more informed decisions about their loans and create a brighter financial future.

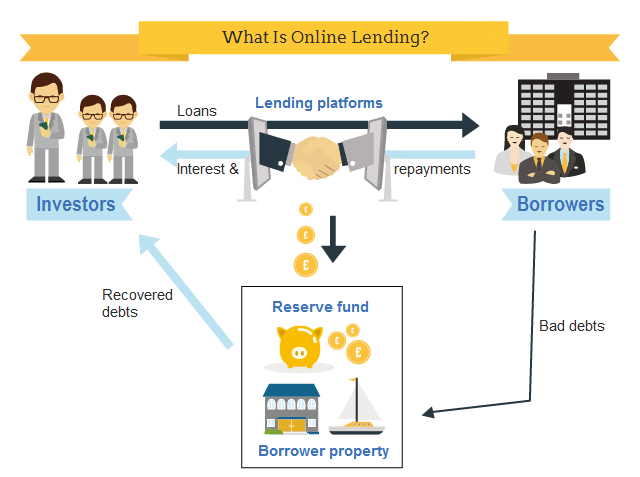

Considering Alternative Lending Options

As a small business owner, you may find it challenging to secure a traditional bank loan, especially if you have a limited credit history or are just starting out. Alternative lending options can provide a viable solution, offering more flexible terms and faster access to funds. For instance, online lenders like Lending Club and Funding Circle have become popular alternatives to traditional banks.

Alternative lending options include crowdfunding, invoice financing, and community development financial institutions (CDFI). These options cater to different business needs and can be more accessible than traditional loans. Crowdfunding platforms like Kickstarter and Indiegogo, for example, allow businesses to raise funds from a large number of people, typically in exchange for rewards or equity.

When considering alternative lending options, it's essential to weigh the benefits and drawbacks of each. Some alternatives may offer faster funding and more flexible repayment terms, but may also come with higher interest rates or fees. Here are some key factors to consider:

- Interest rates and fees: Compare the costs associated with each lending option to ensure you're getting the best deal.

- Repayment terms: Consider the flexibility of repayment terms and whether they align with your business cash flow.

- Collateral requirements: Determine whether the lender requires collateral and what type of assets are accepted.

To choose the most suitable lending option, start by assessing your business needs and financial situation. Consider your credit score, cash flow, and the purpose of the loan to determine which alternative lending option is best for you. For example, if you have a solid credit score and a stable cash flow, you may qualify for a lower-interest loan from a online lender like Prosper or Upstart.

Ultimately, selecting the right alternative lending option requires careful research and comparison of the available options. By understanding the benefits and drawbacks of each alternative, you can make an informed decision that supports your business growth and financial well-being. It's also crucial to read reviews and check the lender's reputation before making a decision, as some alternative lenders may have more stringent requirements or less favorable terms than others.

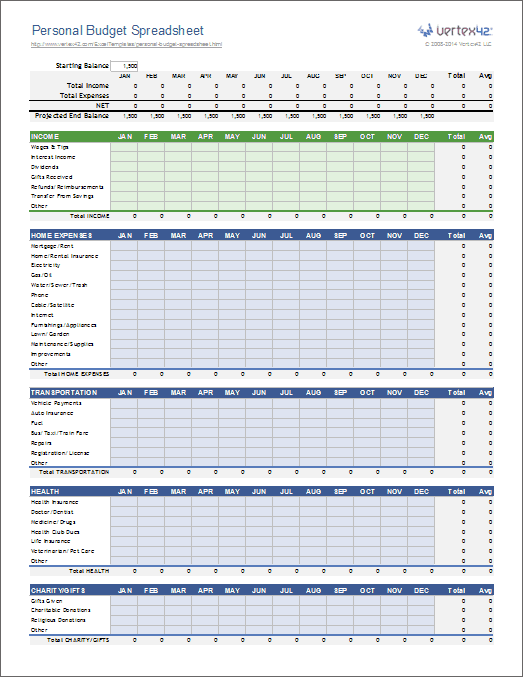

Budgeting and Financial Planning for Borrowers

When it comes to managing your finances as a borrower, creating a budget is essential. This budget should account for your loan repayments, ensuring you never miss a payment and avoiding any potential penalties. A good starting point is to gather all your financial documents, including your loan agreements and income statements, to get a clear picture of your financial situation.

To manage your cash flow effectively, you need to prioritize your expenses and allocate your income accordingly. It's crucial to make timely loan repayments while also covering essential expenses like rent, utilities, and food. By doing so, you'll be able to reduce your debt burden over time and make progress towards financial stability.

Here are some strategies for managing cash flow and reducing debt:

- Make a list of all your debts, including the balance, interest rate, and minimum payment for each

- Prioritize your debts, focusing on the ones with the highest interest rates or the smallest balances

- Consider consolidating your debts into a single loan with a lower interest rate and a longer repayment period

This approach can help simplify your finances and make it easier to stay on top of your payments.

Having an emergency fund in place is also vital for borrowers, as it provides a safety net in case of unexpected expenses or income disruptions. Aim to save 3-6 months' worth of living expenses in an easily accessible savings account, which can help you avoid going further into debt when unexpected costs arise. For example, if you lose your job or face a medical emergency, your emergency fund can help cover your essential expenses while you get back on your feet.

In terms of building an emergency fund, start by setting aside a small amount each month, even if it's just $100 or $500. Over time, this amount can add up, providing you with a cushion against financial shocks. Additionally, consider automating your savings by setting up a monthly transfer from your checking account to your savings or emergency fund account. This way, you'll ensure that you're consistently building your emergency fund without having to think about it.

Frequently Asked Questions (FAQ)

What types of loans are eligible for the prepayment penalty waiver?

When it comes to prepayment penalty waivers, it's essential to understand which types of loans qualify. The waiver applies to floating rate micro and small business loans, providing relief to entrepreneurs and small business owners who want to prepay their loans without incurring additional charges. This can be particularly beneficial for businesses that experience a surge in revenue and want to clear their debts quickly.

To be eligible for the waiver, the loan must meet specific criteria, including being a micro or small business loan with a floating interest rate. This means that businesses with fixed-rate loans or larger enterprises may not be eligible for the waiver. It's crucial to review the loan agreement and understand the terms and conditions before making any prepayment.

Some examples of eligible loans include:

- Floating rate term loans for small businesses

- Microloans with variable interest rates

- Working capital loans with floating rates for small enterprises

These types of loans can benefit from the prepayment penalty waiver, allowing business owners to prepay their loans without incurring additional charges. By understanding the eligibility criteria and types of eligible loans, business owners can make informed decisions about their loan repayment strategy.

It's also important to note that the waiver may have certain conditions, such as a minimum loan tenure or a specific prepayment amount. Business owners should carefully review their loan agreement and consult with their lender to determine if they are eligible for the prepayment penalty waiver. By doing so, they can avoid any potential penalties and make the most of this benefit.

How will this decision affect my existing loan repayment plan?

When considering the impact of a loan waiver on your existing repayment plan, it's essential to review your overall financial situation. This decision can significantly alter your monthly payments and long-term financial goals. By adjusting your loan repayment strategy, you can make the most of the waiver and potentially save money on interest.

To get started, borrowers should assess their current loan terms, including the interest rate, repayment period, and monthly payment amount. They should also consider their income, expenses, and other debt obligations to determine how the waiver will affect their overall financial situation. This evaluation will help identify areas where adjustments can be made to maximize the benefits of the waiver.

Some key factors to consider when adjusting your loan repayment plan include:

- Reducing monthly payments to free up funds for other expenses or savings

- Increasing payments to pay off the loan more quickly and save on interest

- Consolidating multiple loans into a single loan with a lower interest rate

By carefully evaluating these options and making informed decisions, borrowers can create a revised loan repayment plan that takes advantage of the waiver and supports their long-term financial goals.

For example, if you have a high-interest loan with a large monthly payment, you may be able to reduce your payments and allocate the saved funds towards other debt obligations or savings. On the other hand, if you have a low-interest loan with a relatively small monthly payment, you may choose to continue making the same payments to pay off the loan more quickly. By considering your individual circumstances and adjusting your loan repayment strategy accordingly, you can make the most of the waiver and achieve greater financial stability.

Are there any other benefits or incentives for small businesses and borrowers?

The decision made by the RBI is likely to have a positive impact on small businesses and borrowers, and it may be just the beginning. As part of a larger effort to support small businesses and entrepreneurs, the RBI may announce additional benefits and incentives in the future. This could include measures such as reduced interest rates, increased access to credit, and other forms of support.

Some potential benefits that may be announced include tax breaks, subsidies, and other forms of financial assistance. These benefits could be targeted at specific industries or sectors, such as agriculture, manufacturing, or technology. For example, small businesses in the agriculture sector may be eligible for subsidies on equipment and supplies.

The RBI's efforts to support small businesses and entrepreneurs may also include non-financial benefits, such as:

- Business training and mentorship programs

- Access to networking events and conferences

- Support for research and development

These types of benefits can help small businesses and entrepreneurs build their skills and knowledge, and gain access to new markets and opportunities.

In addition to the benefits announced by the RBI, small businesses and borrowers may also be eligible for benefits and incentives offered by other government agencies and organizations. For instance, some states and cities offer tax breaks and other forms of support to small businesses that locate in specific areas or industries. By taking advantage of these benefits, small businesses and borrowers can gain a competitive edge and achieve their goals.