When considering higher education, it's essential to understand the financial implications of taking out student loans. A student loan calculator is a valuable tool that helps you estimate your monthly payments and total interest paid over the life of the loan. By using a calculator, you can make informed decisions about your financial aid options.

To get started, you'll need to gather some basic information, such as the loan amount, interest rate, and repayment term. You can find this information on your loan documents or by contacting your lender directly. With this information, you can plug in the numbers and get an estimate of your monthly payments.

Here are some key factors to consider when using a student loan calculator:

- Loan amount: The total amount you borrow to finance your education

- Interest rate: The percentage of the loan amount that you'll pay in interest over time

- Repayment term: The number of years you have to repay the loan

By understanding these factors, you can use a student loan calculator to create a personalized repayment plan that works for you.

Using a student loan calculator can also help you explore different repayment scenarios, such as paying more than the minimum each month or consolidating multiple loans into one. For example, if you have a $30,000 loan with a 6% interest rate and a 10-year repayment term, you can use a calculator to see how much you'll pay in interest over the life of the loan. This can help you make smart decisions about your finances and avoid costly mistakes.

Understanding Student Loan Calculators

When it comes to managing student loan debt, having the right tools can make all the difference. Student loan calculators are one such tool that can help you understand your loan obligations and make informed decisions about repayment. By using a student loan calculator, you can get a clear picture of your monthly payments, total interest paid, and payoff period.

Student loan calculators work by taking into account various factors such as loan amount, interest rate, and repayment term to provide you with a detailed breakdown of your loan costs. These calculators can be used for both federal and private loans, making them a valuable resource for anyone with student loan debt. Whether you have a subsidized or unsubsidized federal loan, or a private loan from a bank or lender, a student loan calculator can help you navigate the complexities of repayment.

There are many types of student loans that can be calculated using these tools, including:

- Federal loans, such as Direct Subsidized and Unsubsidized Loans, and PLUS Loans

- Private loans from banks, credit unions, and online lenders

- Consolidation loans, which combine multiple loans into one

By using a student loan calculator, you can compare the costs of different loan options and choose the one that best fits your financial situation.

Some popular online student loan calculators include those offered by the Department of Education, NerdWallet, and Student Loan Hero. These calculators often feature tools such as repayment estimators, loan comparison charts, and debt repayment plans. For example, the Department of Education's Repayment Estimator can help you determine which repayment plan is best for you, based on your income and loan balance.

In addition to providing estimates of monthly payments and total interest paid, many student loan calculators also offer features such as amortization schedules and payoff period calculators. These tools can help you see the impact of making extra payments or paying more than the minimum each month. By using a student loan calculator and exploring these features, you can take control of your debt and make a plan to pay off your loans efficiently.

How to Use a Student Loan Calculator

To get started with a student loan calculator, you'll need to input your loan details, including the loan amount, interest rate, and repayment term. This information will give you a baseline understanding of your monthly payments and total repayment amount. For example, if you borrowed $30,000 at a 6% interest rate with a 10-year repayment term, you can plug these numbers into the calculator to see your estimated monthly payment.

Next, you can adjust variables to see different payment scenarios and outcomes. This is a great way to explore how different repayment terms or interest rates might impact your monthly payments. By tweaking these numbers, you can get a sense of what you can afford and what might be a stretch.

Some key variables to experiment with include:

- Loan amount: Try increasing or decreasing the amount you borrowed to see how it affects your monthly payments

- Interest rate: See how different interest rates impact your total repayment amount and monthly payments

- Repayment term: Explore how shorter or longer repayment terms affect your monthly payments and overall cost

By adjusting these variables, you can gain a better understanding of your loan and make more informed decisions about repayment.

Using a student loan calculator can also help you compare different loan options and repayment strategies. For instance, you can use the calculator to weigh the pros and cons of consolidating your loans or exploring income-driven repayment plans. By plugging in different scenarios, you can see which approach might be the most beneficial for your financial situation. This can help you make a more informed decision and potentially save money in the long run.

To get the most out of a student loan calculator, be sure to take your time and experiment with different inputs and scenarios. Don't be afraid to try out different combinations of loan amounts, interest rates, and repayment terms to see how they impact your repayment outlook. With a little practice, you'll be able to use the calculator to make more informed decisions about your student loans and create a personalized plan for repayment.

Creating a Repayment Plan

Having a solid repayment plan is crucial to avoid default and manage your debt effectively. A well-structured plan helps you stay on track, make timely payments, and eventually become debt-free. By creating a plan, you can also reduce stress and anxiety related to debt.

To pay off loans quickly, consider strategies such as income-driven repayment, which adjusts your monthly payments based on your income and family size. Consolidation is another option, where you combine multiple loans into one with a lower interest rate and a single monthly payment. For example, if you have multiple credit card debts with high interest rates, consolidating them into a single personal loan with a lower interest rate can simplify your payments.

When prioritizing loans, focus on those with higher interest rates or urgent deadlines.

- Make a list of all your loans, including the balance, interest rate, and minimum payment due for each.

- Identify the loans with the highest interest rates and prioritize paying those off first.

- Consider setting up automatic payments for your loans to ensure timely payments and avoid late fees.

By prioritizing your loans and making timely payments, you can avoid late fees and negative impacts on your credit score.

It's also essential to review and adjust your repayment plan regularly to ensure you're on track to meet your debt repayment goals. You can use online tools and calculators to help you create and manage your plan, and consider seeking advice from a financial advisor if needed. By staying committed to your plan and making adjustments as needed, you can pay off your loans efficiently and achieve financial stability.

Additional Tips for Managing Student Loan Debt

When managing student loan debt, creating a budget is essential to make timely payments. Start by tracking your income and expenses to understand where your money is going, and then allocate a specific amount for loan repayment each month. This will help you stay on top of your payments and avoid late fees.

To make the most of your budget, consider ways to reduce your expenses, such as cooking at home instead of eating out or finding a roommate to split living costs. You can also take advantage of tax deductions and credits for student loan interest to minimize your taxable income. By making these adjustments, you can free up more money in your budget to put towards your loans.

Having a side hustle or part-time job can significantly increase your income, allowing you to make extra payments on your loans. Some popular side hustles include freelancing, tutoring, or participating in the gig economy. For example, you could drive for a ride-sharing service or deliver food to earn extra money on the weekends.

Here are some benefits of having a side hustle for loan repayment:

- Increase your income to make extra payments on your loans

- Build a financial safety net to fall back on in case of emergencies

- Develop new skills and gain work experience to boost your career

By taking on a side hustle, you can accelerate your loan repayment and get back on track financially.

Monitoring your credit scores and reports is crucial to ensure that your loan payments are being reported correctly. You can request a free credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) once a year to review your credit history. Check for any errors or inaccuracies, such as incorrect payment amounts or late payments, and dispute them if necessary to maintain a healthy credit score.

Regularly reviewing your credit report can also help you identify areas for improvement, such as reducing your debt-to-income ratio or avoiding new credit inquiries. By staying on top of your credit scores and reports, you can ensure that your loan repayment progress is accurately reflected and make informed decisions about your financial future.

Avoiding Common Mistakes

When it comes to managing student loans, it's easy to get overwhelmed and make mistakes that can have long-lasting consequences. Missing payments or ignoring loan statements can lead to a downward spiral of debt, making it harder to get back on track. For instance, a single missed payment can trigger late fees and penalties, adding to the overall debt burden.

Ignoring loan statements can also lead to missed opportunities for repayment assistance, such as income-driven repayment plans or loan forgiveness programs. These programs can help reduce monthly payments or even forgive part of the loan, but they require proactive steps to enroll. By staying on top of loan statements, borrowers can identify potential issues before they become major problems.

The consequences of defaulting on student loans can be severe, including damaged credit and wage garnishment. Defaulting on a loan can also lead to collection agency involvement, which can result in additional fees and stress. Some of the potential consequences of defaulting on student loans include:

- damaged credit scores, making it harder to get credit in the future

- wage garnishment, where a portion of the borrower's paycheck is withheld to pay off the debt

- collection agency involvement, which can result in harassing phone calls and letters

Fortunately, there are resources available to help borrowers get back on track with their loan repayment. Loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), can forgive part or all of the loan debt for borrowers who work in certain fields, such as education or non-profit. Additionally, credit counseling services can provide personalized advice and support to help borrowers create a plan to pay off their debt.

For borrowers struggling to make payments, there are also income-driven repayment plans that can reduce monthly payments based on income and family size. These plans can provide temporary relief and help borrowers avoid default. By seeking help and exploring available resources, borrowers can get back on track with their loan repayment and avoid the consequences of default. Some resources to consider include:

- National Foundation for Credit Counseling (NFCC), a non-profit organization that provides credit counseling and education

- Federal Student Aid, a government website that provides information and resources on student loan repayment and forgiveness

- loan forgiveness programs, such as PSLF or Teacher Loan Forgiveness, which can forgive part or all of the loan debt for eligible borrowers

Frequently Asked Questions (FAQ)

What is the average monthly payment for student loans?

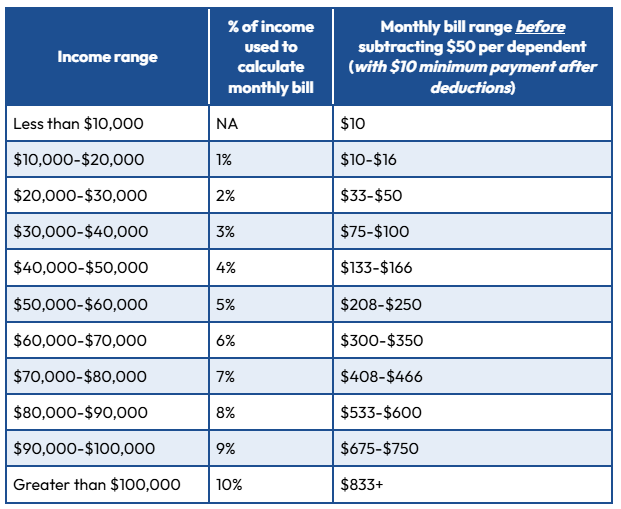

When it comes to managing student loan debt, understanding the average monthly payment is crucial for creating a realistic budget. Average monthly payments vary based on loan amount, interest rate, and repayment term, making it essential to consider these factors when calculating your expenses. For instance, a higher interest rate can significantly increase your monthly payment, even with a relatively low loan amount.

To give you a better idea, let's consider the factors that affect monthly payments:

- Loan amount: A larger loan amount typically results in a higher monthly payment

- Interest rate: A higher interest rate can increase your monthly payment, as more of your payment goes towards interest

- Repayment term: A longer repayment term can lower your monthly payment, but you'll pay more in interest over time

These factors can greatly impact your monthly payment, so it's essential to review your loan details carefully.

For example, a student with a $30,000 loan at a 4% interest rate and a 10-year repayment term might have a monthly payment of around $300. In contrast, a student with a $50,000 loan at a 6% interest rate and a 20-year repayment term might have a monthly payment of around $300 as well, despite the larger loan amount, due to the longer repayment term. By understanding how these factors interact, you can better plan your finances and make informed decisions about your student loan debt.

Can I use a student loan calculator for private loans?

When it comes to managing your student loans, having the right tools can make a big difference. A student loan calculator can be a valuable resource, helping you understand your repayment options and make informed decisions about your debt. Many students assume that these calculators are only for federal loans, but that's not the case.

In fact, many student loan calculators can be used for both federal and private loans, providing a comprehensive view of your debt obligations. By using a calculator, you can get a clear picture of your monthly payments, interest rates, and total repayment amounts. This information can be especially helpful when comparing different loan options or exploring repayment strategies.

Some key features to look for in a student loan calculator include:

- the ability to input different loan amounts and interest rates

- options for calculating monthly payments and total repayment costs

- tools for comparing different repayment plans and scenarios

By using a calculator with these features, you can make more informed decisions about your student loans and develop a personalized plan for managing your debt.

For example, let's say you have a private loan with a balance of $20,000 and an interest rate of 6%. By using a student loan calculator, you can determine your monthly payment amount and total repayment costs over a set period of time, such as 10 years. This information can help you plan your budget and make adjustments as needed to stay on track with your loan payments.

Overall, using a student loan calculator can be a simple and effective way to take control of your debt and make progress towards financial freedom. By exploring your options and creating a personalized plan, you can reduce stress and achieve your long-term goals.

How often should I check my student loan balance and repayment progress?

Checking your student loan balance and repayment progress is a crucial step in managing your debt. By doing so, you can ensure you're on track to meet your repayment goals and make any necessary adjustments to your payment plan. For instance, you might discover that you need to increase your monthly payments to pay off your loan sooner.

Regularly reviewing your loan balance can also help you identify any errors or discrepancies in your account. This could include incorrect payment amounts or missing payments, which can negatively impact your credit score if left unaddressed. To avoid such issues, it's a good idea to check your loan balance at least once a month.

Here are some benefits of regularly checking your student loan balance and repayment progress:

- Stay informed about your outstanding balance and interest accrued

- Track your repayment progress and adjust your payment plan as needed

- Identify and address any errors or discrepancies in your account

By monitoring your loan balance and repayment progress, you can take control of your debt and make informed decisions about your financial future.

In addition to checking your loan balance, you should also review your repayment progress to ensure you're meeting your goals. This can be done by tracking your payment history, monitoring your credit report, and adjusting your budget as needed. For example, you might consider consolidating your loans or enrolling in an income-driven repayment plan to lower your monthly payments.

To make the process easier, you can set up automatic reminders or notifications to check your loan balance and repayment progress on a regular basis. This could be as simple as setting a monthly reminder on your calendar or signing up for email updates from your loan servicer. By staying on top of your student loan debt, you can avoid unnecessary stress and focus on achieving your long-term financial goals.