As we explore the world of personal finance, it's inspiring to hear stories of individuals who have achieved their goals through smart planning. One notable example is that of a 45-year-old retiree who was able to leave the workforce early, thanks to careful budgeting and investing. By prioritizing needs over wants and making conscious financial decisions, this individual was able to build a sustainable nest egg.

The key to this person's success lay in their ability to create a comprehensive financial plan, which included setting clear goals, tracking expenses, and making smart investment choices. For instance, they took advantage of tax-advantaged retirement accounts, such as 401(k) and IRA, to maximize their savings. This approach allowed them to make the most of their hard-earned money and stay on track to meet their objectives.

Some of the strategies that contributed to this individual's financial success include:

- Living below their means and avoiding debt

- Building a diversified investment portfolio

- Continuously educating themselves on personal finance and investing

By following these principles, anyone can take control of their financial future and work towards achieving their goals, whether it's early retirement or simply building a more secure financial foundation. With the right mindset and tools, it's possible to make progress and create a brighter financial future.

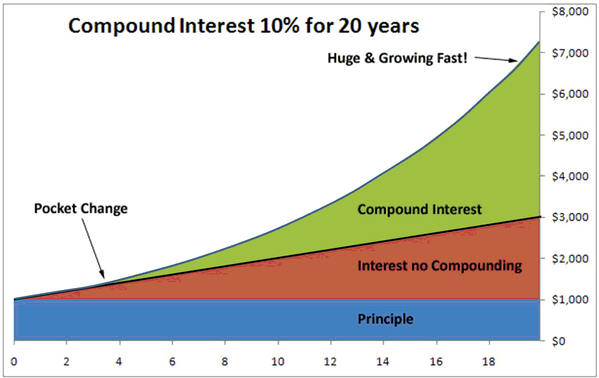

Understanding the Power of Compounding

Consistent saving and investing can lead to significant wealth over time, as seen in the example of the individual who retired at 45. This individual was able to achieve their goal by starting to save and invest early, and letting the power of compounding work in their favor. By doing so, they were able to build a substantial nest egg that allowed them to retire comfortably.

The concept of compounding is simple: it's the process of earning interest on both the principal amount and any accrued interest over time. This can lead to exponential growth, as the interest earned in previous periods becomes the base for the interest earned in subsequent periods. For instance, if you save $1,000 and earn a 5% interest rate, you'll have $1,050 after the first year, and then $1,102.50 after the second year, and so on.

To start a compounding plan, consider the following tips:

- Set up automatic transfers to a savings or investment account to make saving easier and less prone to being neglected

- Take advantage of tax-advantaged accounts such as 401(k) or IRA to maximize your savings

- Start small and be consistent, even if it's just $10 or $20 per month

These small, consistent transfers can add up over time and provide a solid foundation for your compounding plan.

Patience and long-term vision are crucial in achieving financial goals through compounding. It's essential to resist the temptation to withdraw from your savings or investment accounts, and instead, let the power of compounding work in your favor over time. By doing so, you'll be able to build wealth that can last a lifetime, and achieve financial freedom, just like the individual who retired at 45.

To illustrate the importance of patience, consider the example of two individuals who start saving at different ages. One starts saving at 25, while the other starts at 35. Assuming both save the same amount each month, the individual who starts at 25 will have significantly more wealth by the time they retire, due to the power of compounding. This highlights the importance of starting early and being patient, as it can make a significant difference in achieving long-term financial goals.

Debt Management and Financial Discipline

Debt management plays a critical role in achieving early retirement, as it enables individuals to free themselves from the burden of high-interest loans and credit cards. By prioritizing debt repayment, individuals can allocate more resources towards savings and investments, ultimately accelerating their journey towards financial independence. For instance, consider consolidating high-interest debt into a lower-interest loan or balance transfer credit card to reduce overall interest payments.

Creating a budget that prioritizes needs over wants is essential for effective debt management and long-term financial discipline. This involves categorizing expenses into essential needs, such as housing and food, and discretionary wants, such as entertainment and hobbies. By allocating a significant portion of income towards savings and investments, individuals can make steady progress towards their financial goals.

To create a budget that supports debt management and financial discipline, consider the following strategies:

- Track income and expenses to understand where money is being spent

- Set clear financial goals, such as paying off debt or building an emergency fund

- Allocate 50-30-20: 50% of income towards essential needs, 30% towards discretionary wants, and 20% towards savings and investments

By following this framework, individuals can make conscious financial decisions that align with their long-term goals.

Cultivating financial discipline requires a deep understanding of the psychological aspects of money management. This involves recognizing the emotional triggers that lead to impulse purchases and developing habits that support long-term financial goals. For example, implementing a 30-day waiting period for non-essential purchases can help individuals avoid making impulsive buying decisions. By acknowledging the psychological factors that influence financial behavior, individuals can develop strategies to overcome obstacles and stay focused on their goals.

Developing healthy financial habits, such as regular saving and investing, can have a profound impact on long-term financial success. By automating savings and investments, individuals can ensure consistent progress towards their goals, even when motivation wanes. Additionally, celebrating small victories along the way can help build momentum and reinforce positive financial habits. By combining discipline, patience, and persistence, individuals can overcome financial challenges and achieve a secure, prosperous future.

Investing Wisely Without Relying on Stock Tips

When it comes to investing, it's essential to have a solid understanding of diversified investing. This approach involves spreading your investments across various asset classes to manage risk and maximize returns. By doing so, you can reduce your reliance on any one particular investment and increase your potential for long-term growth.

Diversified investing is crucial for managing risk, as it helps to mitigate potential losses by not putting all your eggs in one basket. For example, if you invest solely in stocks and the market experiences a downturn, your entire portfolio could be affected. On the other hand, a diversified portfolio can help you weather market fluctuations and stay on track with your investment goals.

One sensible investment strategy for long-term wealth accumulation is to invest in low-cost index funds and ETFs. These funds track a specific market index, such as the S&P 500, and provide broad diversification and low fees. Some popular options include:

- Vanguard 500 Index Fund

- SPDR S&P 500 ETF Trust

- iShares Core S&P Total U.S. Stock Market ETF

These funds are often a good starting point for beginner investors, as they offer a straightforward and cost-effective way to invest in the market.

It's also important to avoid get-rich-quick schemes and stock tips, as these can be detrimental to your investment portfolio. Instead, focus on developing a well-thought-out investment plan that aligns with your financial goals and risk tolerance. This may involve consulting with a financial advisor or conducting your own research to determine the best investment strategy for your needs.

To get started with investing, consider the following tips:

- Set clear investment goals, such as saving for retirement or a down payment on a house

- Assess your risk tolerance and adjust your portfolio accordingly

- Start with a solid foundation of low-cost index funds and ETFs

By following these tips and avoiding the temptation of get-rich-quick schemes, you can set yourself up for long-term investment success and achieve your financial goals.

In conclusion, investing wisely requires a thoughtful and disciplined approach. By prioritizing diversified investing, low-cost index funds, and a well-thought-out investment plan, you can minimize risk and maximize returns over the long term. Remember to stay informed, avoid impulsive decisions, and always keep your investment goals in mind.

Building Multiple Income Streams

Creating multiple income streams can be a game-changer for accelerating wealth accumulation. By diversifying your income sources, you can reduce your reliance on a single income stream and increase your overall financial stability. This approach can also help you build wealth faster, as you'll have more money to invest and save.

One way to create additional income streams is through real estate investing, which can provide a steady stream of rental income. For example, you could invest in a rental property or consider real estate investment trusts (REITs) for a more hands-off approach. This can be a lucrative option, but it's essential to do your research and understand the local market before making a decision.

Another alternative income source is peer-to-peer lending, which allows you to lend money to individuals or small businesses and earn interest on your investment. This can be a higher-risk option, but it can also provide higher returns than traditional savings accounts. You can use platforms like Lending Club or Prosper to get started, but be sure to assess the creditworthiness of borrowers and diversify your portfolio to minimize risk.

When exploring different income streams, it's crucial to assess and mitigate the risks associated with each option. Here are some tips to consider:

- Research the investment thoroughly and understand the potential risks and returns

- Diversify your portfolio to minimize risk and maximize returns

- Set clear financial goals and develop a plan to achieve them

- Monitor and adjust your investments regularly to ensure they remain aligned with your goals

By taking a thoughtful and informed approach to creating multiple income streams, you can set yourself up for long-term financial success and build wealth faster.

Starting a small business can also be a viable option for creating an additional income stream. This could be something as simple as freelancing or selling products online, or it could be a more complex venture like starting a consulting firm or restaurant. The key is to identify your passions and skills and find a way to monetize them, whether it's through a part-time side hustle or a full-time business venture.

Ultimately, building multiple income streams requires patience, persistence, and a willingness to take calculated risks. By exploring alternative income sources and taking a thoughtful approach to investing and risk management, you can create a more stable and prosperous financial future for yourself. With the right mindset and strategy, you can achieve financial freedom and build wealth that lasts a lifetime.

Achieving Financial Independence

Financial independence is a state where you have the freedom to make choices based on your personal values, rather than just financial necessity. This means having enough wealth to pursue your passions and interests without being tied to a 9-to-5 job. It's essential to note that financial independence is different from early retirement, as it's not just about stopping work, but about having the autonomy to live life on your own terms.

The psychological and emotional aspects of achieving financial independence should not be overlooked, as it can lead to increased happiness and fulfillment. When you're not stressed about money, you can focus on what truly matters to you, leading to a more purposeful life. For example, you might find joy in volunteering, traveling, or spending time with loved ones, which can bring a sense of satisfaction and contentment.

To set and work towards financial independence, it's crucial to set clear goals, such as saving a certain amount of money or paying off debt. You can start by tracking your expenses and creating a budget that allocates your resources effectively. Some key steps to consider include:

- Setting a specific target date for achieving financial independence

- Breaking down larger goals into smaller, manageable tasks

- Automating your savings and investments to make progress easier

By following these steps and staying committed to your goals, you can make steady progress towards financial independence.

Staying motivated is also vital, as the journey to financial independence can be long and challenging. You can find motivation by celebrating small victories, such as paying off a credit card or reaching a savings milestone. Additionally, surrounding yourself with like-minded individuals, such as joining a financial support group or finding a money mentor, can provide encouragement and support.

Tracking progress is also essential to achieving financial independence, as it helps you stay on course and make adjustments as needed. You can use tools like spreadsheets or budgeting apps to monitor your expenses, income, and savings. By regularly reviewing your progress, you can identify areas for improvement and make changes to stay on track.

Ultimately, achieving financial independence requires patience, discipline, and a willingness to make lifestyle changes. By prioritizing your goals, staying focused, and seeking support when needed, you can overcome obstacles and achieve the freedom to live life on your own terms. With persistence and dedication, you can create a more fulfilling and financially secure future.

Frequently Asked Questions (FAQ)

What is the first step towards achieving early retirement?

To begin your journey towards early retirement, it's essential to develop a habit of saving and investing consistently. This means setting aside a portion of your income each month, no matter how small, and allocating it towards your retirement fund. By doing so, you'll be taking the first crucial step towards securing your financial future.

Starting to save early allows you to take advantage of compound interest, which can significantly grow your wealth over time. For instance, if you start saving $100 per month at the age of 25, you'll have a substantial amount by the time you're 50, even with modest investment returns. This highlights the power of consistent saving and investing.

Some practical tips to get you started include:

- Setting up an automatic transfer from your checking account to your retirement account

- Taking advantage of employer-matched retirement accounts, such as a 401(k) or IRA

- Exploring low-cost index funds or ETFs for your investment portfolio

By following these tips and maintaining a consistent savings routine, you'll be well on your way to achieving your early retirement goals. It's also important to remember that it's not about saving a large amount at once, but rather making steady progress over time.

As you continue on your path towards early retirement, you'll want to regularly review and adjust your savings and investment strategy to ensure you're on track to meet your goals. This may involve increasing your monthly savings amount, exploring other investment options, or seeking the advice of a financial advisor. By staying committed and adaptable, you can overcome any obstacles and achieve the financial freedom you desire.

How can I avoid getting caught up in get-rich-quick schemes or stock tips?

To avoid getting caught up in get-rich-quick schemes or stock tips, it's essential to have a solid understanding of sound investment principles. This includes learning about different asset classes, such as stocks, bonds, and real estate, and how they can be used to achieve long-term financial goals. By taking the time to educate yourself, you'll be better equipped to make informed decisions about your investments.

One of the most effective ways to avoid getting caught up in get-rich-quick schemes is to focus on long-term wealth accumulation strategies. This means setting clear financial goals, such as saving for retirement or a down payment on a house, and creating a plan to achieve them. By focusing on the long-term, you'll be less likely to get caught up in short-term market fluctuations or speculative investments.

Some key investment principles to keep in mind include:

- Diversification: spreading your investments across different asset classes to reduce risk

- Dollar-cost averaging: investing a fixed amount of money at regular intervals, regardless of market conditions

- Compounding: allowing your investments to grow over time, with returns reinvested to earn even more

By following these principles, you can create a solid foundation for your investments and avoid getting caught up in get-rich-quick schemes or stock tips.

In addition to educating yourself on sound investment principles, it's also important to be wary of unsolicited investment advice or tips. If someone is promising unusually high returns or guaranteed success, it's likely a scam. Instead, focus on reputable sources of information, such as financial news websites or established investment firms, and do your own research before making any investment decisions.

Is it necessary to have a side hustle to retire early?

Achieving early retirement is a dream for many, and while having a side hustle can certainly help, it's not the only path to getting there. With a solid understanding of personal finance and a well-thought-out plan, it's possible to retire early through smart financial planning, disciplined saving, and wise investing alone. By living below your means and making the most of your money, you can set yourself up for long-term financial success.

One key aspect of achieving early retirement is creating a budget that works for you, not against you. This means tracking your expenses, cutting back on unnecessary spending, and allocating your money towards savings and investments. For example, consider implementing the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment.

Disciplined saving is also crucial when it comes to retiring early, and there are several strategies you can use to make the most of your savings.

- Take advantage of tax-advantaged retirement accounts such as 401(k) or IRA

- Set up automatic transfers from your checking account to your savings or investment accounts

- Consider using a savings challenge, such as the "52-week savings challenge" to stay on track

By making saving a priority and being consistent, you can build up a sizable nest egg over time.

Wise investing is another important factor in achieving early retirement, as it allows your money to grow over time and provides a potential source of passive income. This can involve investing in a diversified portfolio of stocks, bonds, and other assets, or working with a financial advisor to create a customized investment plan. By doing your research and being patient, you can make informed investment decisions that help you reach your long-term financial goals.