As a recent graduate, managing student loans can be overwhelming, especially with the constant changes in regulations and proposals. The idea of handling student loans through the Small Business Administration (SBA) is an interesting concept that has sparked intense debate. This approach, initially proposed by Trump, aims to simplify the loan process and provide more flexible repayment options.

The SBA is well-known for supporting small businesses and entrepreneurs, but its potential role in managing student loans is still a topic of discussion. By exploring this proposal, we can better understand the potential implications for students and recent graduates. For instance, the SBA's involvement could lead to more innovative repayment plans, such as income-driven repayment options.

Some of the key aspects of this proposal include:

- Streamlining the loan process to reduce bureaucracy and paperwork

- Offering more flexible repayment terms, including income-driven repayment plans

- Providing access to additional resources and support for students and graduates

These potential benefits could have a significant impact on the way students manage their loans, making it easier for them to focus on their careers and financial stability. By examining the details of this proposal, we can gain a deeper understanding of how it could shape the future of student loan management.

The potential consequences of handling student loans through the SBA are far-reaching, and it is essential to consider the potential risks and benefits. For example, students may need to adapt to new repayment terms or navigate a different loan servicing system. As we delve into the specifics of this proposal, we will explore the potential advantages and disadvantages, providing readers with a comprehensive understanding of what it could mean for their financial futures.

Understanding the Proposal

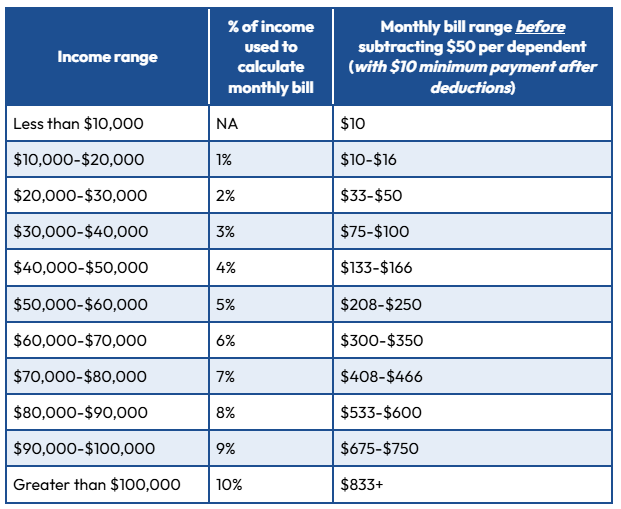

To understand the context behind the proposal, it's essential to consider the current state of student loan debt in the US. The proposal, introduced by Trump, aims to reform the existing student loan structures by potentially involving the Small Business Administration (SBA) in student loan management. This change could significantly impact the way students and graduates manage their debt.

Involving the SBA in student loan management could bring some benefits, such as more flexible repayment terms and potentially lower interest rates. However, it also raises concerns about the SBA's ability to handle the complex world of student loans. For example, the SBA's primary focus is on supporting small businesses, so it may not have the necessary expertise to manage student loans effectively.

Some potential benefits of this proposal include:

- More flexible repayment options, such as income-driven repayment plans

- Potentially lower interest rates, making it easier for borrowers to repay their loans

- Streamlined loan forgiveness programs, making it easier for borrowers to understand and access these programs

On the other hand, there are also some potential drawbacks to consider, such as the SBA's lack of experience in managing student loans and the potential for increased bureaucracy.

The impact on borrowers could be significant, with changes to repayment terms and interest rates being two of the most critical factors. For instance, borrowers may be able to take advantage of more flexible repayment plans, such as income-driven repayment plans, which can help make monthly payments more manageable. Additionally, the proposal could lead to lower interest rates, which would save borrowers money over the life of the loan.

To prepare for these potential changes, borrowers can start by reviewing their current loan terms and repayment options. They can also consider consolidating their loans or exploring income-driven repayment plans to make their monthly payments more manageable. By staying informed and proactive, borrowers can navigate any changes to the student loan system and make the most of the available options.

It's also important for borrowers to understand how the proposal could affect their overall financial situation, including their credit score and long-term financial goals. For example, borrowers who take advantage of income-driven repayment plans may have lower monthly payments, but they may also end up paying more in interest over the life of the loan. By considering these factors and planning carefully, borrowers can make informed decisions about their student loans and achieve financial stability.

Impact on Borrowers

The proposed changes to student loan management are likely to have a significant impact on borrowers. For instance, borrowers who currently rely on income-driven repayment plans may need to reassess their debt management strategy. This could involve exploring alternative repayment options or seeking professional advice to navigate the new landscape.

One key area of concern is the potential changes to income-driven repayment plans, which could affect how borrowers manage their debt. Borrowers who are currently enrolled in these plans may need to adjust their budgets and payment schedules accordingly. For example, if the proposal limits the amount of debt that can be forgiven, borrowers may need to prioritize their payments to maximize the benefits.

The potential effects on borrowers' credit scores and financial health are also a major concern. A change in repayment terms or interest rates could negatively impact credit scores, making it harder for borrowers to secure loans or credit in the future. To mitigate this risk, borrowers can focus on making timely payments and keeping their debt-to-income ratio low.

To prepare for potential changes, borrowers can take proactive steps, such as:

- Reviewing their current repayment plans and budget to identify areas for adjustment

- Exploring alternative repayment options, such as consolidating loans or refinancing

- Building an emergency fund to cover unexpected expenses or changes in income

By taking these steps, borrowers can better navigate the potential changes and protect their financial health.

Borrowers can also stay informed about the proposal and its progress by following reputable sources, such as the Department of Education or financial news outlets. This will help them stay up-to-date on any developments and make informed decisions about their debt management. Additionally, borrowers can seek guidance from financial advisors or credit counselors to get personalized advice on managing their debt.

Alternative Debt Management Strategies

Debt consolidation is a popular strategy for managing debt, and it involves combining multiple debts into one loan with a lower interest rate and a single monthly payment. This can simplify the debt repayment process and potentially save money on interest charges. For example, consolidating high-interest credit card debt into a lower-interest personal loan can help borrowers pay off their debt more efficiently.

When it comes to paying off debt, having a side hustle or additional income stream can be a game-changer. This extra income can be used to make extra payments on debt, reducing the principal balance and saving money on interest charges. Some popular side hustles include freelancing, selling products online, or participating in the gig economy.

There are many resources available to help borrowers manage their debt and create a budget. Some useful tools include:

- Spreadsheets like Google Sheets or Microsoft Excel to track income and expenses

- Budgeting apps like Mint or You Need a Budget (YNAB) to automate budgeting and track spending

- Financial planning websites like NerdWallet or The Balance to provide guidance and support

These resources can help borrowers create a personalized budget and debt repayment plan, taking into account their unique financial situation and goals.

In addition to debt consolidation and side hustles, there are other alternative debt management strategies that borrowers can explore. For instance, income-driven repayment plans can help borrowers with federal student loans lower their monthly payments and potentially qualify for loan forgiveness. By exploring these options and using the right tools and resources, borrowers can take control of their debt and achieve financial stability.

Investing in Financial Health

Investing in financial health is a crucial step towards securing your future and achieving long-term stability. By prioritizing financial health, you can build a safety net that protects you from unexpected expenses and ensures a comfortable retirement. This involves creating a comprehensive plan that addresses multiple aspects of your financial life, including saving, investing, and debt management.

Building an emergency fund is a fundamental aspect of investing in financial health, as it provides a cushion in case of unexpected events, such as job loss or medical emergencies. Aim to save 3-6 months' worth of living expenses in a readily accessible savings account. This fund will help you avoid going into debt when unexpected expenses arise, allowing you to stay on track with your long-term financial goals.

Investing in retirement savings, such as a 401(k) or IRA, can have a significant impact on your financial stability and security. These accounts offer tax benefits and compound interest, helping your savings grow over time. For example, contributing to a 401(k) plan can reduce your taxable income, while also building a nest egg for your golden years.

To get started with investing in financial health, consider the following tips:

- Take advantage of employer matching contributions to your 401(k) or other retirement accounts

- Automate your savings by setting up monthly transfers from your checking account

- Review and adjust your budget to ensure you're allocating enough funds towards savings and debt repayment

By following these tips and prioritizing financial health, you can set yourself up for long-term success and achieve your goals.

Balancing debt repayment with investing in financial health requires careful planning and discipline. Start by prioritizing high-interest debts, such as credit card balances, and focus on paying those off as quickly as possible. Meanwhile, continue to contribute to your retirement accounts and emergency fund, even if it's just a small amount each month. This will help you make progress towards your long-term goals while also tackling your debt.

Next Steps for Borrowers

The proposal has several key takeaways that borrowers should be aware of, including potential changes to interest rates, repayment terms, and forgiveness programs. These changes could have a significant impact on borrowers, affecting their monthly payments and overall debt burden. For example, a change in interest rates could save borrowers hundreds of dollars per year.

To prepare for these changes, borrowers can take several steps, including reviewing their current loan terms and understanding how the proposed changes may affect them. This can involve checking their loan statements and contacting their loan servicer with any questions. Borrowers can also start by taking the following actions:

- Checking their credit report to ensure it is accurate and up-to-date

- Researching income-driven repayment plans and forgiveness programs

- Creating a budget that accounts for potential changes in monthly payments

Staying informed about updates to the proposal and its implementation is crucial for borrowers. This can involve following reputable news sources and government websites, such as the Department of Education, to stay up-to-date on the latest developments. By doing so, borrowers can ensure they are prepared for any changes that may affect their student loans and can take advantage of any new programs or benefits that become available.

Borrowers can also take proactive steps to manage their debt, such as consolidating their loans or refinancing to a lower interest rate. Additionally, they can explore options for deferment or forbearance if they are experiencing financial hardship. By being informed and taking action, borrowers can navigate the potential changes to student loan management and make the best decisions for their financial situation.

It is essential for borrowers to stay organized and keep track of important deadlines and updates. They can do this by setting reminders and following financial experts and bloggers who provide timely and relevant information on student loan management. By doing so, borrowers can ensure they are well-prepared for any changes that may come their way.

Frequently Asked Questions (FAQ)

How will Trump's proposal affect my current student loan repayment plan?

When considering the potential effects of Trump's proposal on your current student loan repayment plan, it's essential to understand that the impact will vary depending on the specifics of the proposal and how it is implemented. This means that borrowers will need to wait for the official details to be released before making any changes to their repayment strategy. For now, it's crucial to continue making payments and monitoring the situation closely.

The proposal's impact on current repayment plans will depend on several factors, including the type of loan you have and the repayment plan you're currently enrolled in. If you're unsure about how the proposal might affect you, it's a good idea to review your loan documents and repayment terms to get a better understanding of your situation. You can also contact your loan servicer for guidance and support.

Some key aspects of the proposal that could influence your repayment plan include:

- Changes to interest rates or fees associated with your loan

- Modifications to repayment terms, such as the length of the repayment period

- Introduction of new repayment plans or forgiveness programs

These potential changes could have a significant impact on your monthly payments and overall repayment strategy, so it's vital to stay informed and adapt your plan accordingly.

To prepare for any potential changes, consider reviewing your budget and identifying areas where you can make adjustments to free up more money for loan payments. You can also explore income-driven repayment plans or forgiveness programs that may be available to you. By taking proactive steps and staying up-to-date on the latest developments, you can minimize the potential disruption to your repayment plan and stay on track with your financial goals.

Can I still consolidate my debt if the Small Business Administration takes over student loans?

Recently, there have been discussions about the Small Business Administration (SBA) potentially taking over student loans, which has left many borrowers wondering about their debt consolidation options. The proposal's details will determine the future of debt consolidation options for borrowers, and it is essential to understand how this change could impact your financial situation. If the SBA takes over student loans, it may introduce new rules and regulations that could affect existing debt consolidation programs.

For borrowers who are considering consolidating their debt, it is crucial to stay informed about the proposal's progress and any changes that may occur. This will help you make informed decisions about your debt consolidation options and avoid any potential pitfalls. You can check the official government website or consult with a financial advisor to stay up-to-date on the latest developments.

Some key factors to consider when evaluating debt consolidation options under the potential new system include:

- Interest rates: How will the SBA's takeover affect interest rates on student loans, and will this impact your debt consolidation options?

- Repayment terms: Will the SBA introduce new repayment terms or modify existing ones, and how will this affect your ability to consolidate your debt?

- Eligibility: Who will be eligible for debt consolidation under the new system, and what are the requirements for qualifying?

By understanding these factors, you can make informed decisions about your debt consolidation options and create a plan that works best for your financial situation.

If the SBA takes over student loans, it may also introduce new benefits or programs that can help borrowers manage their debt. For example, the SBA may offer more flexible repayment terms or income-driven repayment plans that can help reduce your monthly payments. By staying informed and adapting to the changes, you can take advantage of these benefits and make progress towards becoming debt-free.

What can I do now to prepare for potential changes in student loan management?

As a student loan borrower, it's essential to be proactive and adapt to any potential changes in student loan management. Reviewing your current repayment plans is a great place to start, allowing you to understand your options and make informed decisions about your debt. This includes checking your interest rates, loan terms, and monthly payment amounts to ensure you're on the right track.

Exploring budgeting tools can also help you manage your student loans more effectively. Websites and apps like Mint, You Need a Budget (YNAB), and Personal Capital offer free or low-cost resources to track your expenses, create a budget, and set financial goals. By using these tools, you can identify areas where you can cut back on unnecessary expenses and allocate more funds towards your student loan debt.

To pay off your debt more efficiently, consider strategies such as the snowball method or the avalanche method. Here are some key considerations:

- Pay more than the minimum payment each month to reduce the principal amount and interest accrued over time

- Consolidate your loans to simplify your payments and potentially lower your interest rate

- Take advantage of income-driven repayment plans or forgiveness programs, if eligible

By implementing these strategies, you can make steady progress on your student loan debt and be better prepared for any changes that may come your way.