As a young adult, navigating the world of student loans can be overwhelming, especially with so many options available. Sallie Mae student loans are a popular choice, but it's essential to understand their features, benefits, and drawbacks before making a decision. By doing your research, you can make an informed choice that suits your financial needs and goals.

When considering Sallie Mae student loans, it's crucial to weigh the pros and cons. On the one hand, Sallie Mae offers a range of loan options, including undergraduate, graduate, and career training loans. For example, their undergraduate loans offer competitive interest rates and flexible repayment terms, making them an attractive option for many students.

Some of the key benefits of Sallie Mae student loans include:

- Competitive interest rates and repayment terms

- No origination fees or prepayment penalties

- Multiple repayment options, including deferment and forbearance

These benefits can help you manage your debt and stay on top of your finances, even after graduation. By understanding the features and benefits of Sallie Mae student loans, you can make a more informed decision about your financial aid options.

In this article, we'll delve deeper into the world of Sallie Mae student loans, exploring their features, benefits, and drawbacks in detail. We'll also provide practical tips and examples to help you navigate the application process and make the most of your loan. Whether you're a student, parent, or recent graduate, this guide will provide you with the information you need to make smart financial decisions.

Overview of Sallie Mae Student Loans

Sallie Mae has been a prominent player in the student loan industry for over 40 years, initially founded as a government-sponsored entity. Over time, the company has evolved to become a private lender, offering a range of student loan products to help students achieve their higher education goals. With a long history of providing financial aid, Sallie Mae has built a reputation as a trusted and reliable lender.

The company offers various types of student loans, including undergraduate and graduate loans, designed to cater to different academic pursuits. For instance, undergraduate students can opt for the Smart Option Student Loan, which provides flexible repayment terms and competitive interest rates. Graduate students, on the other hand, can explore the MBA Loan or the Medical School Loan, tailored to meet the specific needs of these fields.

Some of the key features of Sallie Mae student loans include:

- Competitive interest rates and flexible repayment terms

- No origination fees or prepayment penalties

- Multiple repayment options, including deferred payment and interest-only payment plans

These features can help students manage their debt effectively and make informed decisions about their financial aid.

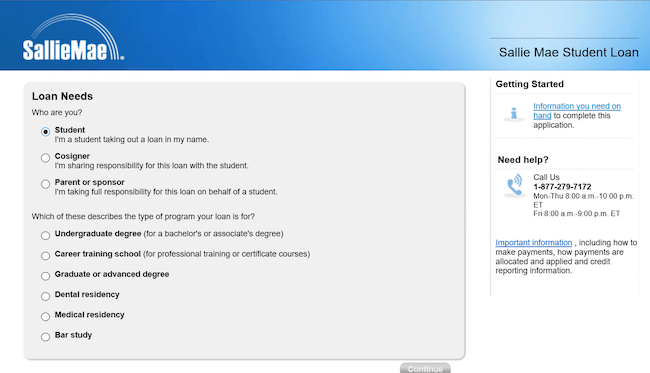

To apply for a Sallie Mae student loan, students typically need to provide documentation, such as proof of enrollment, income verification, and credit information. The application process usually involves an online application, followed by a review of the student's creditworthiness and loan eligibility. For example, students can apply for a Sallie Mae student loan by visiting the company's website and submitting their application, which will then be reviewed and processed.

The required documentation for Sallie Mae student loans may vary depending on the loan type and the student's individual circumstances. However, some common documents required include:

- Social Security number or Individual Taxpayer Identification Number

- Proof of income, such as a W-2 form or tax return

- Proof of enrollment, such as a letter from the school or a course schedule

Students can check the Sallie Mae website for specific requirements and to initiate the application process.

Interest Rates and Repayment Terms

When exploring student loan options, it's essential to consider interest rates and repayment terms. Sallie Mae student loans offer competitive interest rates, ranging from 2.50% to 12.60% APR, which can vary depending on the type of loan and borrower credit score. For instance, a lower interest rate can save you hundreds or even thousands of dollars over the life of the loan.

To make an informed decision, compare the interest rates of Sallie Mae student loans to those of other lenders, such as Discover, Wells Fargo, or federal student loans. This comparison can help you identify the most affordable option for your financial situation. For example, federal student loans may offer more favorable interest rates, with rates as low as 4.53% for undergraduate students.

Repayment terms and options are also crucial to understand, as they can significantly impact your ability to repay the loan. Some common repayment terms and options include:

- Deferment, which allows you to temporarily postpone loan payments due to financial hardship or other circumstances

- Forbearance, which provides a temporary reduction or suspension of loan payments

- Income-driven repayment plans, which adjust your monthly payments based on your income and family size

These options can provide much-needed flexibility and relief during challenging financial periods.

The interest rate on your student loan can have a substantial impact on the overall cost of the loan and your repayment amount. For instance, a higher interest rate can lead to a larger total repayment amount over the life of the loan. To illustrate, a $20,000 loan with a 6% interest rate may require a total repayment of $26,000 over 10 years, whereas the same loan with a 4% interest rate may only require a total repayment of $23,000. Understanding the potential impact of interest rates can help you make informed decisions about your student loan and repayment strategy.

Benefits and Drawbacks of Sallie Mae Student Loans

When it comes to financing your education, Sallie Mae student loans are a popular option for many students. One of the benefits of Sallie Mae student loans is that they offer flexible repayment options, allowing you to choose a plan that works best for your financial situation. For example, you can opt for a graduated repayment plan, which starts with lower payments that increase over time.

Another advantage of Sallie Mae student loans is that they do not charge origination fees, which can save you money upfront. This is a significant benefit, especially for students who are already struggling to cover tuition costs. Additionally, Sallie Mae offers a range of loan options, including undergraduate and graduate loans, as well as loans for specific fields of study, such as medical or law school.

However, there are also some drawbacks to consider when it comes to Sallie Mae student loans. One of the potential downsides is the risk of late fees, which can add up quickly if you miss a payment. Some other drawbacks include:

- Limited forgiveness options, which may not be as generous as those offered by federal loan programs

- Variable interest rates, which can increase over time

- Less stringent borrower protections, which may leave you vulnerable to unfair lending practices

In comparison to other student loan options, Sallie Mae student loans may offer more flexible repayment terms than some federal loans, but they may not offer the same level of forgiveness options or borrower protections. Private loans from other lenders may offer more competitive interest rates, but they may also come with less flexible repayment terms. For example, federal loans such as the Direct Subsidized and Unsubsidized Loans offer more generous forgiveness options, including Public Service Loan Forgiveness.

To get the most out of a Sallie Mae student loan, it's essential to carefully review the terms and conditions before signing on the dotted line. This includes understanding the interest rate, repayment terms, and any fees associated with the loan. By doing your research and comparing different loan options, you can make an informed decision that works best for your financial situation. It's also a good idea to explore other financing options, such as scholarships, grants, and work-study programs, to help minimize your reliance on loans.

Alternatives to Sallie Mae Student Loans

When it comes to financing your education, Sallie Mae is a well-known option, but it's not the only one. Federal loans, such as Direct Subsidized and Unsubsidized Loans, are a great alternative, offering competitive interest rates and flexible repayment terms. For example, the interest rate for Direct Subsidized Loans is currently around 4.5%, making them a more affordable option for many students.

Private loans from other lenders, like Discover and Wells Fargo, are also available, offering a range of interest rates and repayment terms. These loans can be a good option for students who have exhausted their federal loan options or need additional funding. However, it's essential to carefully review the terms and conditions, as private loans often have higher interest rates and less flexible repayment terms.

Some benefits of alternative student loan options include:

- Lower interest rates, which can save you money in the long run

- More flexible repayment terms, such as income-driven repayment plans

- No origination fees, which can reduce the overall cost of the loan

On the other hand, some drawbacks to consider are:

- Stricter eligibility requirements, which may make it harder to qualify

- Less generous borrowing limits, which may not cover all your education expenses

- Fewer borrower benefits, such as forbearance and deferment options

To choose the best student loan option for your individual needs and financial situation, consider your credit score, income, and expenses. You should also research and compare different lenders, looking for the most competitive interest rates and repayment terms. For instance, if you have a good credit score, you may be able to qualify for a lower interest rate with a private lender.

Ultimately, finding the right student loan option requires careful consideration and research. By weighing the benefits and drawbacks of each alternative, you can make an informed decision that works for you and your financial situation. It's also essential to borrow only what you need and to explore other funding options, such as scholarships and grants, to minimize your debt.

)

Managing Sallie Mae Student Loans for Financial Health

When it comes to managing Sallie Mae student loans, creating a budget is essential. This involves tracking your income and expenses to determine how much you can allocate towards loan repayment each month. By making a budget, you can prioritize your expenses and make timely payments.

To develop an effective repayment plan, consider your loan terms, interest rates, and repayment options. You can choose from various repayment plans, such as the income-driven repayment plan or the graduated repayment plan, depending on your financial situation. For example, if you have a variable interest rate, you may want to prioritize paying off that loan first to minimize interest accumulation.

Monitoring your credit scores and reports is crucial when repaying student loans. Your credit score can affect your ability to secure loans or credit cards in the future, so it's essential to check your report regularly for errors or inaccuracies. You can request a free credit report from the three major credit bureaus (Experian, TransUnion, and Equifax) once a year.

Here are some tips for managing your credit score while repaying student loans:

- Make on-time payments to demonstrate responsible credit behavior

- Keep credit utilization below 30% to maintain a healthy credit mix

- Avoid applying for multiple credit cards or loans in a short period

By following these tips, you can maintain a good credit score and improve your overall financial health.

The impact of student loan debt on long-term financial health and stability can be significant. High-interest debt can limit your ability to save for retirement, purchase a home, or achieve other long-term financial goals. For instance, if you have a large amount of high-interest debt, you may need to allocate a larger portion of your income towards debt repayment, leaving less room for savings and investments.

To mitigate the impact of student loan debt, consider consolidating your loans or refinancing to a lower interest rate. You can also explore income-driven repayment plans or loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), which can help reduce your debt burden. By taking proactive steps to manage your student loan debt, you can achieve financial stability and security in the long run.

Frequently Asked Questions (FAQ)

What are the eligibility requirements for Sallie Mae student loans?

To qualify for a Sallie Mae student loan, you must meet specific eligibility criteria. Being a US citizen or permanent resident is a fundamental requirement, as it ensures you have a valid social security number and are eligible to receive federal and private loans. This requirement applies to both undergraduate and graduate students.

Enrollment in a degree-granting program at an eligible institution is also necessary, as Sallie Mae only provides loans to students who are actively pursuing a degree. This can include associate's, bachelor's, master's, or doctoral programs, as well as certificate programs in certain fields. It's essential to check with your school to confirm their eligibility.

In terms of credit and income requirements, Sallie Mae considers several factors, including:

- credit score, with a minimum score often required for loan approval

- income level, as lenders want to ensure you have a stable source of income to repay the loan

- debt-to-income ratio, which should be reasonable to avoid over-borrowing

These requirements may vary depending on the specific loan product and your individual circumstances, so it's crucial to review the terms and conditions carefully.

For example, if you're an undergraduate student with limited credit history, you may need to apply with a cosigner who meets the credit and income requirements. This can help you qualify for a loan with a more favorable interest rate and repayment terms. By understanding the eligibility requirements and carefully reviewing your options, you can make informed decisions about your student loan choices.

Can I consolidate or refinance my Sallie Mae student loans?

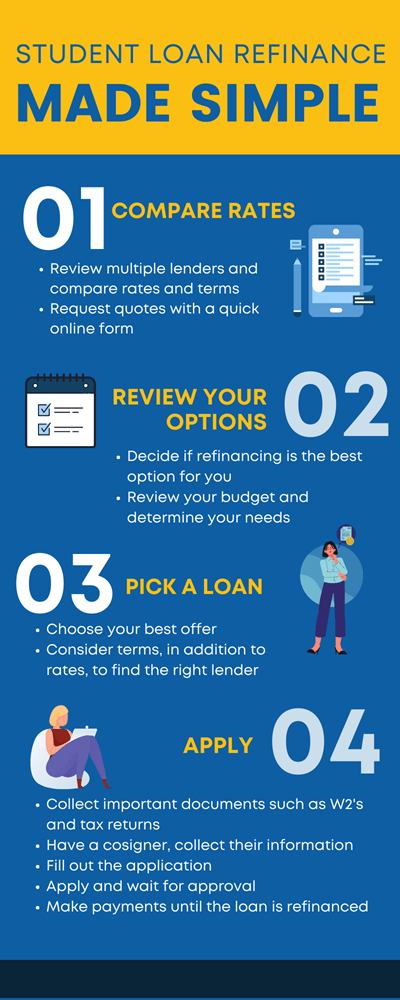

Consolidating or refinancing your student loans can be a great way to simplify your repayment process and potentially save money. If you have Sallie Mae student loans, you may be wondering if you can consolidate or refinance them. The good news is that yes, it is possible to consolidate or refinance Sallie Mae student loans, which can help you manage your debt more effectively.

To consolidate your Sallie Mae student loans, you can combine multiple loans into one loan with a single interest rate and monthly payment. This can make it easier to keep track of your payments and avoid missing any. For example, if you have multiple Sallie Mae loans with different interest rates and payment due dates, consolidating them into one loan can simplify your repayment process.

There are several benefits to consolidating or refinancing your Sallie Mae student loans, including:

- Lower monthly payments: Consolidating or refinancing your loans can lower your monthly payments, making it easier to manage your debt.

- Lower interest rates: You may be able to qualify for a lower interest rate, which can save you money over the life of the loan.

- Simplified repayment: Consolidating your loans can simplify your repayment process, making it easier to keep track of your payments.

It's worth noting that consolidating or refinancing your Sallie Mae student loans may not always be the best option, so it's essential to weigh the pros and cons before making a decision.

When considering consolidating or refinancing your Sallie Mae student loans, it's crucial to shop around and compare rates and terms from different lenders. You can start by checking with Sallie Mae to see if they offer any consolidation or refinancing options, and then compare those with other lenders. By doing your research and comparing your options, you can make an informed decision that's right for you.

How do I contact Sallie Mae customer service for help with my student loan?

When you need help with your student loan, contacting Sallie Mae customer service is a great place to start. You can reach out to them through various channels, including phone, email, or online chat, depending on what you prefer. This flexibility makes it easy to get the assistance you need in a way that's convenient for you.

To get started, you can visit the Sallie Mae website to find the contact information for their customer service team. They are available to help with a range of issues, from answering questions about your loan balance to assisting with payment plans. Whether you're a current student or a graduate, their team is there to provide support and guidance.

Some common reasons to contact Sallie Mae customer service include:

- Questions about your loan balance or payment due dates

- Issues with making payments or setting up a payment plan

- Requests for loan deferment or forbearance

- Concerns about interest rates or loan terms

By reaching out to their customer service team, you can get the help you need to manage your student loan effectively and make informed decisions about your financial situation.

If you're not sure where to start, you can begin by reviewing the Sallie Mae website for FAQs and other resources that may answer your questions. If you still need assistance, you can contact their customer service team directly, and they will be happy to help you with your student loan-related queries. Remember to have your account information ready when you reach out to them, as this will help them to assist you more efficiently.