As a student, taking out loans can be a necessary step to finance your education, but it's essential to understand the terms and conditions that come with borrowing. One critical aspect to consider is the interest rate, as it can significantly impact the total amount you repay. For instance, a higher interest rate can lead to thousands of dollars in additional costs over the life of the loan.

Understanding student loan interest rates is crucial for managing debt, as it allows you to make informed decisions about your borrowing and repayment strategies. By knowing the interest rate on your loan, you can anticipate how much you'll owe each month and plan accordingly. This knowledge can also help you compare different loan options and choose the one that best suits your financial situation.

To get started, it's helpful to familiarize yourself with the key concepts related to student loan interest rates, such as:

- Fixed vs. variable interest rates

- How interest accrues and capitalizes

- The differences between subsidized and unsubsidized loans

By grasping these ideas, you'll be better equipped to navigate the world of student loans and make smart choices about your financial aid. Additionally, being aware of the current interest rate environment can help you time your borrowing and repayment strategically, potentially saving you money in the long run.

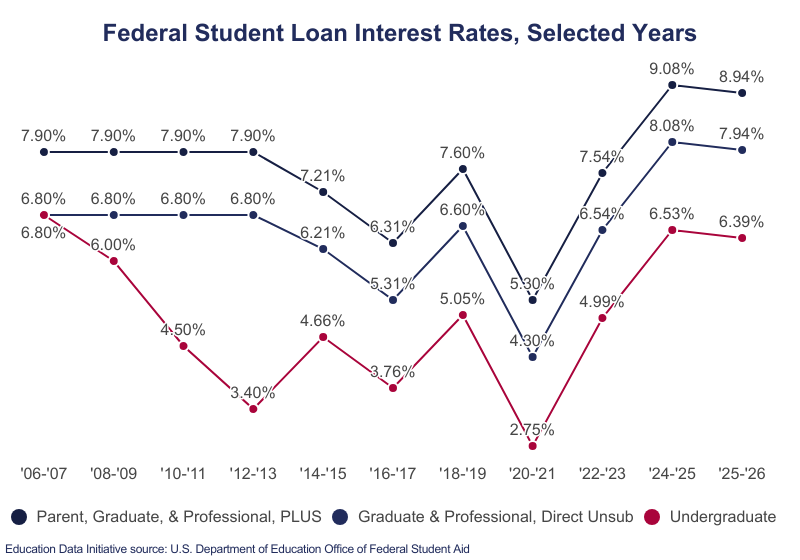

Federal Student Loan Interest Rates 2025

As a student, understanding federal student loan interest rates is crucial for managing your debt effectively. The current federal student loan interest rates for undergraduate students are around 4.53%, while graduate students can expect rates of approximately 6.54%. These rates apply to direct unsubsidized loans and direct PLUS loans.

For comparison, the interest rates for the 2023-2024 academic year were slightly lower, with undergraduate rates at 4.99% and graduate rates at 6.54%. It's essential to stay informed about potential future changes, as interest rates can fluctuate based on market conditions and government policies.

To give you a better idea, here are some key points to consider when evaluating federal student loan interest rates:

- Interest rates can vary depending on the type of loan and the borrower's degree level

- Subsidized loans, which are available to undergraduate students with demonstrated financial need, often have lower interest rates

- Interest rates for federal student loans are typically fixed, meaning they remain the same throughout the life of the loan

If you have existing federal student loans, it's a good idea to check your interest rate to understand how much you'll be paying over time. You can do this by logging into your account on the Federal Student Aid website or by contacting your loan servicer directly. For example, if you have a $10,000 loan with an interest rate of 4.53%, you can expect to pay around $453 in interest over a 10-year repayment period.

To check the interest rate on your existing federal student loans, follow these steps:

- Log in to your Federal Student Aid account online

- Click on the "My Aid" tab and select "View Loan Details"

- Look for the "Interest Rate" field, which will display the current interest rate for each of your loans

Staying on top of your federal student loan interest rates can help you make informed decisions about your debt and develop a effective repayment strategy. By understanding how interest rates work and how to manage your loans, you can save money and achieve financial stability over time.

Private Student Loan Interest Rates 2025

When exploring private student loan options, it's essential to compare interest rates among top lenders. This can help you save thousands of dollars in interest payments over the life of the loan. For instance, a 1% difference in interest rate can result in a significant reduction in your overall debt burden.

Private student loans often have higher interest rates compared to federal student loans, but they can offer more flexible repayment terms. However, federal student loans typically provide more borrower protections, such as income-driven repayment plans and forgiveness options. It's crucial to weigh the benefits and drawbacks of choosing private over federal student loans before making a decision.

Some of the benefits of private student loans include:

- Higher borrowing limits to cover education expenses

- Faster application and approval processes

- More flexible repayment terms, including longer repayment periods

On the other hand, the drawbacks of private student loans include:

- Higher interest rates, resulting in more expensive loans

- Less generous borrower protections, such as limited deferment and forbearance options

- Stricter credit requirements, making it harder for students with poor credit to qualify

To negotiate or refinance private student loans for better rates, consider the following tips:

- Check your credit report and work on improving your credit score to qualify for lower interest rates

- Compare rates among multiple lenders to find the best offer

- Consider consolidating multiple private student loans into a single loan with a lower interest rate

By doing your research and exploring your options, you can find a private student loan with a competitive interest rate that helps you achieve your educational goals. Additionally, be sure to read and understand the terms and conditions of your loan before signing any agreement.

)

Strategies to Minimize Student Loan Interest

Making timely payments is crucial to minimizing student loan interest. By paying on time, you can avoid late fees and prevent interest from accruing on your loan balance. For instance, a single late payment can result in a late fee, which can add up quickly and increase the overall cost of your loan.

Income-driven repayment plans can also significantly impact interest payments. These plans, such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE), can help lower your monthly payments by capping them at a certain percentage of your income. However, it's essential to note that while these plans can make your payments more manageable, they may not always be the best option for minimizing interest payments.

To minimize interest payments, consider the following strategies:

- Pay more than the minimum payment each month to reduce the principal balance and interest accrued over time

- Take advantage of interest rate discounts offered by your lender for setting up automatic payments

- Consider consolidating your loans to simplify your payments and potentially lower your interest rate

Using tax deductions for student loan interest can also help reduce the financial burden of your loans. You may be eligible to deduct up to $2,500 in interest paid on your student loans, which can result in significant tax savings. For example, if you paid $1,500 in interest on your student loans last year, you may be able to deduct that amount from your taxable income.

It's essential to keep accurate records of your interest payments and consult with a tax professional to ensure you're taking advantage of the tax deductions available to you. Additionally, you can use online tools and resources to track your interest payments and stay on top of your loan balance. By being proactive and informed, you can make the most of these strategies and minimize the amount of interest you pay on your student loans over time.

Budgeting for Student Loan Repayment

To create a budget that prioritizes student loan repayment, start by tracking your income and expenses to understand where your money is going. Make a list of all your necessary expenses, such as rent, utilities, and groceries, and then identify areas where you can cut back. This will help you allocate more funds towards your student loan debt.

The 50/30/20 rule is a useful guideline for allocating your income towards different expenses, where 50% goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment. When applying this rule to student loan debt management, you can adjust the proportions to allocate a larger percentage towards debt repayment, especially if you have high-interest loans. For example, you could allocate 60% of your income towards necessary expenses, 20% towards discretionary spending, and 20% towards student loan repayment.

To increase your income for loan repayment, consider taking on a side hustle or part-time job. Some ideas include:

- Freelance writing or graphic design

- Tutoring or teaching English online

- Part-time retail or food service work

- Ride-sharing or delivery driving

- Selling products online through platforms like eBay or Etsy

These side hustles can help you earn an extra $500-$1000 per month, which can be dedicated entirely towards your student loan debt.

When creating your budget, be sure to prioritize your student loans with the highest interest rates first. You can use the snowball method, where you pay off the loan with the smallest balance first, or the avalanche method, where you pay off the loan with the highest interest rate first. Consider using a budgeting app or spreadsheet to track your income and expenses and stay on top of your loan repayment progress.

In addition to increasing your income, you can also look for ways to reduce your expenses and allocate more funds towards your student loan debt. This could include cutting back on subscription services, cooking at home instead of eating out, or finding ways to lower your rent or utilities. By making a few small changes to your budget and increasing your income, you can make significant progress on paying off your student loans and achieving financial freedom.

Investing While Paying Off Student Loans

When it comes to managing your finances after graduation, you may find yourself torn between investing for the future and paying off student loans. Investing in a retirement account, such as a 401(k) or IRA, can provide long-term benefits, like compound interest and tax advantages. However, paying off high-interest loans can save you money on interest payments and free up your monthly cash flow.

Paying off high-interest loans, typically those with rates above 6%, should be your priority, as it can save you a significant amount of money in interest payments over time. On the other hand, investing in a retirement account can provide a potential long-term return on investment, which can be beneficial if you start early. For example, contributing to a 401(k) with a company match can essentially give you free money towards your retirement.

If you decide to invest while paying off student loans, consider low-risk options, such as:

- High-yield savings accounts, which provide easy access to your money and typically offer higher interest rates than traditional savings accounts

- Index funds or ETFs, which offer broad diversification and tend to be less volatile than individual stocks

- Certificates of deposit (CDs), which provide a fixed return for a specific period of time

These options can help you grow your wealth over time while minimizing the risk of losses.

Automating your investments alongside loan payments can help you make progress on both fronts. Set up a monthly transfer from your checking account to your investment account, and take advantage of automatic payment plans for your student loans. By doing so, you can ensure that you're consistently investing for the future and making timely loan payments, which can help you stay on track and achieve your financial goals.

Frequently Asked Questions (FAQ)

How do federal student loan interest rates affect my monthly payments?

When it comes to managing your student loan debt, understanding how federal student loan interest rates work is crucial. Federal student loan interest rates directly impact the total amount borrowed and monthly payments, making it essential to consider them when creating a repayment plan. By knowing your interest rate, you can anticipate how much you'll owe over the life of the loan.

The interest rate on your federal student loan can significantly affect your monthly payments. For instance, a higher interest rate means you'll pay more in interest over time, resulting in higher monthly payments. To put this into perspective, a 1% difference in interest rate can add up to thousands of dollars in interest payments over the life of the loan.

Here are some key factors to consider when thinking about federal student loan interest rates and their impact on monthly payments:

- Interest accrual: Interest on your federal student loan begins to accrue as soon as the loan is disbursed, unless you have a subsidized loan.

- Interest capitalization: Unpaid interest can capitalize, or be added to the principal balance, increasing the total amount you owe.

- Repayment term: The length of your repayment period can also impact your monthly payments, with longer repayment terms often resulting in lower monthly payments but more paid in interest over time.

To make the most of your federal student loan and keep monthly payments manageable, it's a good idea to explore income-driven repayment plans or consider consolidating your loans to simplify your payments. By doing so, you can reduce your monthly payments and make progress on paying off your debt. Additionally, making timely payments and paying more than the minimum payment when possible can help you pay off your loan faster and save on interest.

Can I refinance my federal student loans to a private lender for a lower interest rate?

Refinancing federal student loans to a private lender can be a tempting option, especially if you're looking to lower your interest rate. This can be a good move if you have a stable income and a good credit score, as you may be able to qualify for a lower interest rate than what you're currently paying. However, it's essential to weigh the pros and cons before making a decision.

When you refinance your federal student loans to a private lender, you may be able to save money on interest, but you'll often lose access to federal benefits like income-driven repayment plans and Public Service Loan Forgiveness. For example, if you're a teacher or work in a non-profit organization, you may be eligible for loan forgiveness after a certain number of years, but this benefit will be lost if you refinance with a private lender. It's crucial to consider whether the potential savings are worth giving up these benefits.

Here are some things to consider when deciding whether to refinance your federal student loans:

- Check your credit score to see if you qualify for a lower interest rate with a private lender

- Review your loan terms and calculate how much you'll save with a lower interest rate

- Research private lenders and compare their rates and terms to find the best option for you

It's also important to note that some private lenders may offer perks like flexible repayment terms or unemployment protection, which can be beneficial if you're between jobs or experiencing financial hardship.

Before refinancing, make sure you understand the terms of your new loan, including the interest rate, repayment term, and any fees associated with the loan. You should also consider speaking with a financial advisor to determine the best course of action for your individual situation. By carefully weighing the pros and cons, you can make an informed decision that works best for your financial goals.

What are some strategies for paying off high-interest student loans quickly?

Paying off high-interest student loans can be a daunting task, but with the right strategies, you can tackle your debt quickly and efficiently. Making extra payments is one of the most effective ways to pay off your loans, as it reduces the principal amount and saves you from paying interest over time. For example, if you pay an extra $100 per month on a $30,000 loan with a 6% interest rate, you can save around $1,000 in interest and pay off your loan six months earlier.

The debt avalanche method is another strategy that involves paying off loans with the highest interest rates first, while making minimum payments on other loans. This approach can save you a significant amount of money in interest over time. To illustrate, let's say you have two loans: one with a 4% interest rate and a balance of $10,000, and another with a 7% interest rate and a balance of $20,000. By paying off the loan with the 7% interest rate first, you can save around $2,000 in interest over the life of the loan.

Some other strategies for paying off high-interest student loans quickly include:

- Considering loan consolidation or refinancing to lower your interest rate and monthly payments

- Using tax deductions and credits to reduce your taxable income and free up more money for loan payments

- Automating your payments to ensure you never miss a payment and can take advantage of interest rate discounts

By implementing these strategies, you can pay off your high-interest student loans quickly and start building a stronger financial future. It's essential to create a personalized plan that works for your financial situation and goals, and to stay committed to your plan over time.