As students navigate their high school years, they are faced with numerous decisions that can impact their financial future. Teaching financial literacy in high school is crucial, as it equips students with the necessary skills to manage their finances effectively and make informed decisions about money. By incorporating financial education into high school curricula, students can develop healthy financial habits from a young age.

Financial literacy is essential for students to understand the value of money, how to budget, and the importance of saving. For instance, students can start by creating a simple budget to track their expenses, such as allocating a portion of their allowance or part-time job earnings towards savings and spending. This habit can help them develop a sense of responsibility and prepare them for independent financial decision-making in the future.

Some key areas of financial literacy that can be taught in high school include:

- budgeting and money management

- understanding credit and debt

- investing and saving for the future

By covering these topics, students can gain a comprehensive understanding of personal finance and make smart financial decisions that will benefit them throughout their lives. For example, students can learn how to prioritize needs over wants, avoid overspending, and set financial goals for themselves.

Teaching financial literacy in high school can also have long-term benefits, such as reducing financial stress and promoting economic stability. By educating students about personal finance, we can empower them to make informed decisions about their financial lives and set them up for success in the future. This, in turn, can have a positive impact on their overall well-being and quality of life.

Why Financial Literacy Matters

Financial literacy is a crucial life skill that can significantly impact students' future financial health and stability. By understanding basic financial concepts, such as budgeting, saving, and investing, students can make informed decisions about their financial resources. This knowledge can help them avoid common pitfalls, like overspending and debt, and set themselves up for long-term financial success.

Not teaching financial literacy can have severe consequences, including debt and poor financial decisions. Without a solid understanding of personal finance, students may struggle to manage their finances effectively, leading to financial stress and instability. For example, they may accumulate high-interest credit card debt or take on excessive student loans, which can be difficult to pay off.

Some of the consequences of poor financial literacy include:

- High levels of debt, including credit card debt and student loans

- Poor credit scores, which can limit access to affordable credit and loans

- Difficulty saving for long-term goals, such as retirement or buying a home

These consequences can have a lasting impact on students' financial well-being and stability.

Fortunately, there are many successful financial literacy programs in high schools that can help students develop essential financial skills. For instance, the National Endowment for Financial Education (NEFE) offers a range of educational resources and programs to teach students about personal finance and money management. Similarly, the Jump$tart Coalition for Personal Financial Literacy provides educational materials and workshops to help students develop financial literacy skills.

Examples of successful financial literacy programs include:

- The Dave Ramsey Foundation's financial literacy curriculum, which is used in thousands of high schools across the country

- The Next Gen Personal Finance (NGPF) program, which provides free financial literacy resources and lesson plans for teachers

- The Financial Literacy and Education Commission's (FLEC) national strategy for financial literacy, which aims to improve financial education in schools and communities

These programs demonstrate the importance of teaching financial literacy in high schools and can serve as models for other educational institutions.

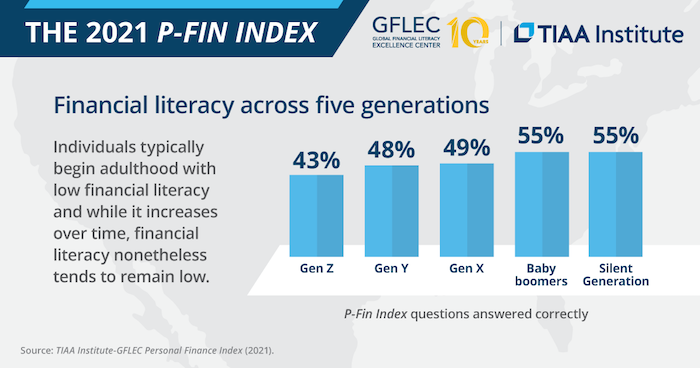

Current State of Financial Literacy

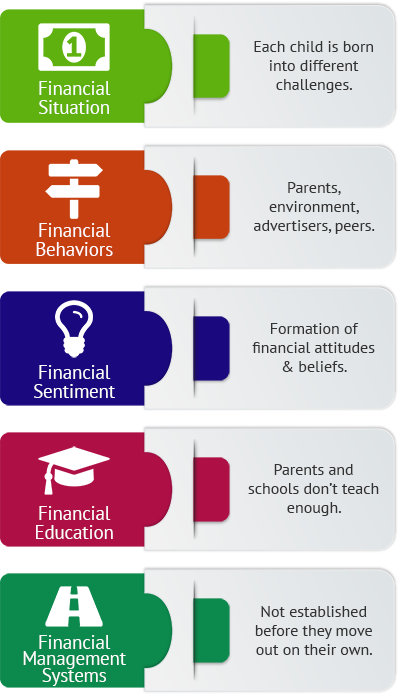

Financial literacy is a crucial life skill that is often overlooked in high school education. According to a recent survey, only 22% of high school students have a decent understanding of personal finance concepts, such as budgeting and saving. This lack of knowledge can have long-term consequences, including debt and financial instability.

The current state of financial literacy among high school students is alarming, with many students graduating without a basic understanding of financial concepts. Statistics show that 64% of high school students cannot balance a checkbook, and 45% do not understand the concept of compound interest. These numbers highlight the need for improved financial education in high schools.

Several factors contribute to the lack of financial literacy, including inadequate education and socioeconomic status. For example, students from low-income families may not have access to financial resources or guidance, making it difficult for them to develop good financial habits. Additionally, many schools do not prioritize financial education, leaving students to learn through trial and error.

Some of the key factors that contribute to the lack of financial literacy include:

- Inadequate education: Many schools do not provide comprehensive financial education, leaving students without a basic understanding of personal finance concepts.

- Socioeconomic status: Students from low-income families may not have access to financial resources or guidance, making it difficult for them to develop good financial habits.

- Lack of parental guidance: Many parents do not discuss financial matters with their children, leaving them without a role model for good financial behavior.

Financial literacy varies significantly among different demographics and socioeconomic groups. For instance, students from higher-income families tend to have a better understanding of financial concepts, such as investing and credit management. On the other hand, students from lower-income families may struggle with basic financial concepts, such as budgeting and saving.

To improve financial literacy, it is essential to provide students with access to comprehensive financial education and resources. This can include workshops, online courses, and mentorship programs that teach students about personal finance concepts and provide guidance on how to manage their finances effectively. By prioritizing financial education, we can help students develop good financial habits and set them up for long-term financial success.

Implementing Financial Literacy Programs

Implementing financial literacy programs in high schools is a crucial step in empowering students with the knowledge and skills to manage their finances effectively. To start, schools can develop a comprehensive curriculum that covers key topics such as budgeting, saving, and investing. This curriculum should be designed to be engaging and interactive, with real-life examples and case studies to help students understand the practical applications of financial concepts.

When it comes to curriculum development, it's essential to involve teachers and financial experts in the process to ensure that the material is accurate and relevant. Teachers should also receive training on how to effectively teach financial literacy, including how to use technology and online resources to enhance the learning experience. For example, online simulations and games can be used to teach students about the consequences of financial decisions, such as overspending or not saving for retirement.

The role of technology and online resources in teaching financial literacy cannot be overstated. Online platforms and tools can provide students with access to a wealth of information and resources, including:

- Interactive tutorials and quizzes

- Personal finance apps and budgeting tools

- Online forums and discussion groups

- Virtual field trips to financial institutions and organizations

These resources can help students learn about financial concepts in a fun and engaging way, and can also provide teachers with the support and materials they need to teach financial literacy effectively.

There are many examples of successful financial literacy programs that have had a positive impact on students' financial knowledge and behavior. For instance, the National Endowment for Financial Education's (NEFE) High School Financial Planning Program has been shown to improve students' financial knowledge and attitudes towards money management. Similarly, the Jump$tart Coalition's financial literacy program has been successful in increasing students' understanding of financial concepts and their ability to make informed financial decisions.

To implement a financial literacy program in a high school, administrators can start by assessing the needs and interests of their students and developing a plan that addresses those needs. This can involve partnering with local financial institutions and organizations to provide resources and expertise, as well as leveraging technology and online resources to enhance the learning experience. By taking a comprehensive and engaging approach to financial literacy education, schools can help students develop the skills and knowledge they need to achieve financial stability and success.

Overcoming Challenges and Barriers

Implementing financial literacy programs can be a daunting task, especially when faced with limited resources and lack of teacher expertise. Many schools and organizations struggle to find the necessary funds to develop and implement comprehensive financial literacy programs. As a result, they often rely on external partnerships to fill the gap.

One of the most significant barriers to financial literacy is the lack of qualified teachers who can effectively impart financial knowledge to students. To overcome this challenge, schools can partner with financial institutions and community organizations that offer financial education resources and training for teachers. For example, some banks offer free financial literacy workshops and online resources that can be used in the classroom.

Some common challenges and barriers to implementing financial literacy programs include:

- Lack of resources and funding

- Insufficient teacher expertise and training

- Limited access to financial education materials and resources

- Diverse student needs and learning styles

To overcome these challenges, schools and organizations can explore partnerships with local businesses, non-profits, and government agencies that can provide financial support, expertise, and resources.

Ongoing evaluation and assessment of financial literacy programs are crucial to ensuring their effectiveness and identifying areas for improvement. This can be done by tracking student progress, conducting regular surveys and feedback sessions, and assessing the program's impact on students' financial knowledge and behaviors. By regularly evaluating and refining their financial literacy programs, schools and organizations can ensure that they are providing students with the most effective and relevant financial education possible.

Partnerships with financial institutions and community organizations can also provide opportunities for students to engage in real-world financial experiences, such as internships, mentorship programs, and financial planning competitions. These hands-on experiences can help students develop practical financial skills and apply theoretical knowledge in a real-world context. By leveraging these partnerships and resources, schools and organizations can overcome common challenges and barriers to implementing financial literacy programs and provide students with a comprehensive and effective financial education.

Conclusion and Next Steps

As we've explored the world of financial literacy, it's clear that teaching these skills in high school is crucial for setting students up for success. By incorporating financial literacy into high school curricula, we can empower students with the knowledge and confidence to make informed decisions about their money. This, in turn, can have a lasting impact on their financial stability and overall well-being.

Effective financial literacy programs can have a significant impact on students' lives, from helping them navigate student loans to making smart investment decisions. For example, programs like the National Endowment for Financial Education's High School Financial Planning Program have been shown to improve students' financial knowledge and behaviors. By supporting and promoting these types of programs, we can help create a more financially literate generation.

To get involved in promoting financial literacy in your community, consider reaching out to local schools or organizations that offer financial education programs. You can also volunteer to teach a financial literacy class or workshop, or simply share your own knowledge and experiences with others. Some ways to take action include:

- Partnering with local businesses or organizations to offer financial workshops or seminars

- Volunteering to teach financial literacy classes at a local school or community center

- Supporting policy initiatives that promote financial literacy education in schools

If you're interested in learning more about financial literacy and how to implement programs in your community, there are many resources available. The Jump$tart Coalition for Personal Financial Literacy and the National Foundation for Credit Counseling are two organizations that offer a wealth of information and resources on financial literacy. You can also check out online courses or workshops, such as those offered by Coursera or edX, to learn more about personal finance and financial education.

For readers who want to take their financial literacy to the next level, consider checking out books like "The Total Money Makeover" or "Your Money or Your Life" for practical tips and advice. You can also follow personal finance blogs or websites, such as BudgetWiseGrad, to stay up-to-date on the latest news and trends in financial literacy. By taking these next steps, you can help promote financial literacy in your community and empower others to take control of their financial lives.

Frequently Asked Questions (FAQ)

Why is financial literacy important for high school students?

Financial literacy is a vital life skill that high school students should acquire to navigate their financial lives effectively. By understanding basic financial concepts, such as budgeting and saving, students can make informed decisions about their financial futures. This knowledge will help them avoid common financial pitfalls, like overspending and debt, and set themselves up for long-term financial stability.

As high school students prepare for college or enter the workforce, they will be faced with financial decisions that can impact their future. For instance, they may need to take out student loans or open their first credit card, which can be overwhelming without a solid understanding of personal finance. By learning about financial literacy, students can develop healthy financial habits and avoid costly mistakes.

Some key areas of financial literacy that high school students should focus on include:

- Budgeting and expense tracking to manage their money effectively

- Understanding different types of savings accounts and investment options

- Learning about credit scores and how to maintain a good credit history

By mastering these concepts, students can develop a strong foundation for financial decision-making and set themselves up for long-term financial success.

High school students can start practicing financial literacy by taking small steps, such as creating a budget for their part-time job or saving for a short-term goal, like a car or college fund. They can also seek out resources, such as online courses or financial workshops, to learn more about personal finance and stay ahead of the curve. By prioritizing financial literacy, students can build a brighter financial future and achieve their goals with confidence.

Financial literacy is not just about managing money; it's also about making smart decisions that align with one's values and goals. By educating themselves about personal finance, high school students can develop a growth mindset and take control of their financial lives. This, in turn, will help them make informed decisions about their financial futures and avoid debt and financial pitfalls.

How can parents and educators teach financial literacy to high school students?

Teaching financial literacy to high school students is crucial for their future financial well-being. Parents and educators can play a significant role in this process by using real-life examples to illustrate key financial concepts, such as budgeting and saving. For instance, they can use everyday expenses like buying lunch or paying for extracurricular activities to demonstrate how to make smart financial decisions.

Incorporating financial education into school curricula is another effective way to teach financial literacy. This can be done by introducing personal finance courses or workshops that cover topics like investing, credit management, and financial planning. By doing so, students can gain a comprehensive understanding of financial principles and develop healthy financial habits from an early age.

To further support financial learning, parents and educators can provide access to online resources and tools, such as:

- Interactive websites that offer financial simulations and games

- Mobile apps that teach budgeting and expense tracking

- Online platforms that provide educational videos and tutorials on personal finance

These resources can help students engage with financial concepts in a fun and interactive way, making learning more enjoyable and effective.

By working together, parents and educators can empower high school students with the knowledge and skills needed to manage their finances wisely and achieve long-term financial stability. This can be achieved by making financial education a priority and providing students with the tools and support they need to succeed. As a result, students will be better equipped to make informed financial decisions and navigate the complexities of the financial world with confidence.

What are some common challenges in teaching financial literacy to high school students?

Teaching financial literacy to high school students is a crucial step in preparing them for a stable financial future. However, many educators face challenges in effectively imparting this knowledge. One of the primary obstacles is the lack of resources, including textbooks, online materials, and guest speakers, which can limit the scope of financial topics that can be covered.

Teacher expertise is another significant challenge, as not all educators have a background in finance or experience teaching financial literacy. This can make it difficult for them to develop engaging lesson plans and accurately assess student understanding. To overcome this, schools can provide teachers with training and support to enhance their knowledge and confidence in teaching financial literacy.

Student engagement is also a common challenge, as financial concepts can be complex and dry, making it hard for students to stay interested. To combat this, educators can use real-life examples, such as budgeting for a prom or saving for college, to illustrate key financial concepts. Additionally, incorporating interactive activities, like simulations or games, can help students develop practical financial skills.

Some of the key challenges in teaching financial literacy include:

- Lack of resources, including textbooks and online materials

- Insufficient teacher expertise and training

- Difficulty in engaging students and making financial concepts relevant

- Complexity of financial concepts, such as investing and credit management

- Need for ongoing evaluation and assessment to measure student progress

To address these challenges, educators can seek out partnerships with financial institutions, non-profits, or community organizations that offer financial literacy resources and support. By working together, educators can provide high school students with a comprehensive and engaging financial education that prepares them for success.