As a graduate student pursuing a career in medicine or law, managing student loans is a significant concern. The spending bill signed into law by former President Trump has notable implications for aspiring doctors and lawyers. This legislation affects the ways in which student loans are structured, repaid, and forgiven, making it essential for students to understand these changes.

For students in these fields, the spending bill's provisions can have a substantial impact on their financial planning. For instance, the bill's changes to income-driven repayment plans and public service loan forgiveness programs can affect how much aspiring doctors and lawyers repay each month. Understanding these changes can help students make informed decisions about their financial aid and loan repayment strategies.

Some key aspects of the spending bill that students should be aware of include:

- Changes to income-driven repayment plans, which can lower monthly payments for some borrowers

- Modifications to public service loan forgiveness programs, which can benefit students pursuing careers in public interest law or medicine

- Increased funding for programs that support students pursuing careers in high-need fields, such as primary care medicine

These provisions can have a significant impact on a student's overall financial situation, and being aware of them can help students navigate the complex world of student loans. By understanding the implications of the spending bill, aspiring doctors and lawyers can make more informed decisions about their financial aid and loan repayment strategies.

Understanding the Loan Change

The recent spending bill has introduced significant changes to the student loan landscape, affecting graduate students in particular. This loan change aims to reduce the federal deficit, but it may have unintended consequences for students pursuing higher education. As a result, it is essential for students to understand the specifics of the bill and how it will impact their financial plans.

The bill affects student loans by altering the interest rates and repayment terms, which may lead to an increase in debt burden for students. Graduate students, especially those pursuing professional degrees like medicine and law, will be disproportionately affected due to the already high cost of these programs. For instance, medical students may face higher interest rates on their loans, making it more challenging to repay their debt after graduation.

Some of the key changes to the loan program include:

- Increased interest rates on graduate loans

- Changes to the income-driven repayment plans

- Reduced loan forgiveness options

These changes may force students to reassess their financial plans and consider alternative options, such as attending lower-cost institutions or pursuing different career paths.

The potential increase in debt burden may also impact students' career choices, as they may be less likely to pursue lower-paying jobs in fields like public service or non-profit work. For example, a student who wants to become a public interest lawyer may need to reconsider their career goals due to the high debt burden associated with law school. To mitigate this, students can explore alternative loan options, such as private loans or scholarships, to help fund their education.

Students can also take proactive steps to manage their debt, such as creating a budget and repayment plan, and exploring loan forgiveness options. By understanding the loan change and its potential implications, students can make informed decisions about their financial plans and career choices, and develop strategies to minimize their debt burden. It is crucial for students to stay informed and adapt to the changing landscape of student loans to ensure they can achieve their educational and career goals.

Impact on Aspiring Doctors and Lawyers

Aspiring doctors and lawyers often face significant financial challenges as they pursue their degrees. High tuition costs, which can range from $50,000 to over $60,000 per year, are a major concern for these students. Additionally, limited financial aid options can make it difficult for students to cover these expenses.

The loan change could exacerbate these challenges, making it even harder for students to afford the cost of attending medical or law school. For example, if the loan change results in higher interest rates or less favorable repayment terms, students may be deterred from pursuing these careers due to the increased financial burden. This could have long-term consequences for the healthcare and legal professions.

Some of the key financial challenges faced by medical and law students include:

- High tuition costs, which can lead to significant debt burdens

- Limited financial aid options, such as scholarships and grants

- High living expenses, particularly for students attending school in urban areas

To mitigate the impact of the loan change, students could explore alternative funding options, such as private scholarships or part-time jobs.

Students could also consider financial strategies like budgeting and saving to reduce their expenses and make the most of their financial aid. For instance, creating a budget that accounts for all expenses, including tuition, living expenses, and transportation, can help students prioritize their spending and make informed financial decisions.

Another option for students is to look into income-driven repayment plans, which can help make loan payments more manageable after graduation. By exploring these alternative funding options and financial strategies, aspiring doctors and lawyers can reduce the financial burden of pursuing their degrees and achieve their career goals.

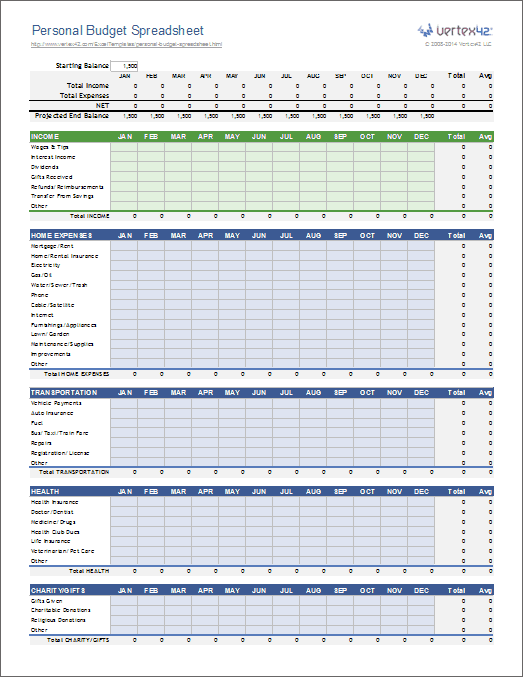

Budgeting and Financial Planning Strategies

Creating a personalized budget is essential for managing finances effectively, especially when considering the potential increase in student loan debt. To start, track your income and expenses to understand where your money is going and identify areas for improvement. This can be done using a budgeting app or a simple spreadsheet.

When building your budget, prioritize essential expenses such as rent, utilities, and food, and then allocate funds for non-essential expenses like entertainment and hobbies. It's also crucial to factor in debt repayment, including student loans, and aim to pay more than the minimum payment each month. For example, consider using the 50/30/20 rule, where 50% of your income goes towards essential expenses, 30% towards non-essential expenses, and 20% towards saving and debt repayment.

Exploring side hustles or part-time jobs can significantly supplement your income and reduce reliance on loans. Some popular side hustles include freelancing, tutoring, or participating in the gig economy. Consider your skills and interests when choosing a side hustle, and be sure to research the potential earnings and time commitment required.

To further secure your financial stability, consider investing in a retirement account or other long-term investment vehicles. This can include:

- Contributing to a Roth IRA or traditional IRA

- Investing in a 401(k) or other employer-sponsored retirement plan

- Exploring low-cost index funds or ETFs

These options can provide a safety net for the future and help you build wealth over time.

Investing in your future doesn't have to be complicated or overwhelming. Start by educating yourself on the different types of investment vehicles and seeking guidance from a financial advisor if needed. Additionally, consider setting up automatic transfers from your checking account to your investment accounts to make saving and investing easier and less prone to being neglected.

By following these budgeting and financial planning strategies, you can set yourself up for long-term financial success and reduce the burden of student loan debt. Remember to regularly review and adjust your budget to ensure it's working effectively for you, and don't be afraid to seek help when needed. With patience, discipline, and the right guidance, you can achieve financial stability and secure a brighter financial future.

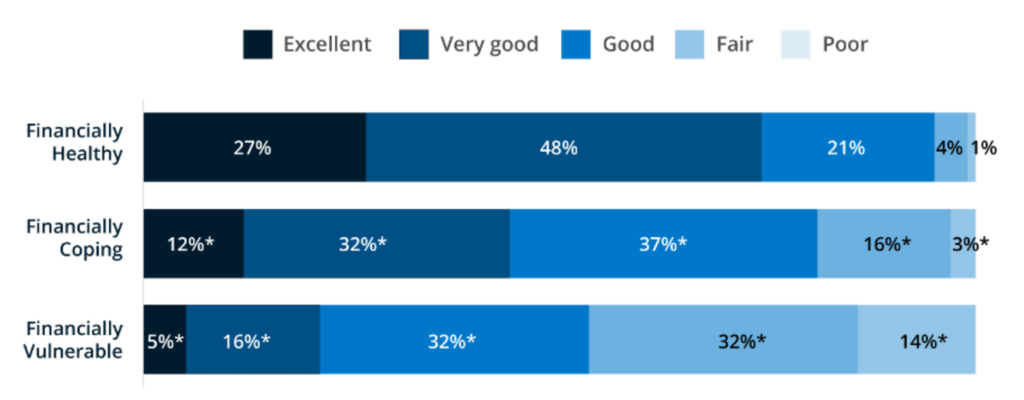

Long-Term Financial Health Implications

When it comes to long-term financial health, changes in loan terms can have a significant impact on students' credit scores. A single missed payment or high debt-to-income ratio can lower a credit score, making it harder to secure loans or credit cards in the future. For example, a student with a high credit score may qualify for a lower interest rate on a car loan, saving them hundreds of dollars in interest payments.

Students' debt-to-income ratios are also affected by loan changes, as a higher debt burden can limit their ability to take on new debt, such as a mortgage. This can have long-term implications for students' ability to purchase homes, start families, or achieve other financial milestones. To mitigate this, students can focus on paying down high-interest debt and building an emergency fund to cover 3-6 months of living expenses.

Some key strategies for managing debt and maintaining financial stability include:

- Creating a budget and tracking expenses to understand where money is going

- Prioritizing high-interest debt and making extra payments to pay off balances quickly

- Building an emergency fund to cover unexpected expenses and avoid going further into debt

By taking a proactive approach to debt management, students can protect their long-term financial health and achieve their goals, even in the face of uncertainty.

In terms of achieving financial milestones, students who are struggling with debt may need to delay purchasing a home or starting a family. However, with careful planning and debt management, it's possible to get back on track and achieve these goals. For example, students can consider working with a financial advisor to create a personalized plan for paying off debt and building wealth over time.

Ultimately, maintaining financial stability requires a combination of short-term and long-term planning. By understanding the potential implications of loan changes and taking proactive steps to manage debt, students can protect their financial health and achieve their goals. This may involve making lifestyle adjustments, such as reducing expenses or taking on a side job, to free up more money for debt repayment and savings.

Next Steps for Concerned Students

As the spending bill continues to evolve, it's essential for students to stay up-to-date on the latest developments and their potential impact on financial aid and student loans. Students can check the official government website or reputable news sources for updates on the bill's implementation. By staying informed, students can better understand how the changes may affect their financial situation and make necessary adjustments.

For personalized guidance, students can seek advice from financial advisors or student loan experts who can help navigate the changing landscape. These professionals can provide tailored advice on managing debt, creating a budget, and exploring available financial aid options. For example, students can ask about income-driven repayment plans or loan forgiveness programs that may be available to them.

To get involved in advocacy efforts, students can:

- contact their representatives to express concerns about the spending bill and its impact on higher education

- join student organizations or advocacy groups that focus on education policy and financial aid

- participate in online campaigns or petitions that aim to raise awareness about the issue

By taking an active role in advocacy efforts, students can make their voices heard and contribute to shaping the future of higher education funding.

Students can also utilize online resources, such as the National Association of Student Financial Aid Administrators (NASFAA) or the Consumer Financial Protection Bureau (CFPB), to stay informed about financial aid and student loan policies. These organizations often provide updates, guides, and tools to help students navigate the complex world of financial aid and make informed decisions about their financial futures. By leveraging these resources, students can take control of their financial situation and make progress towards achieving their goals.

Frequently Asked Questions (FAQ)

How will the loan change affect my current student loans?

If you're currently repaying student loans, you might be wondering how the loan change will impact your existing debt. The good news is that existing loans may be grandfathered in, meaning the new rules won't apply to you. This means you can continue making payments under the same terms you agreed to when you took out the loan.

The loan change is likely to affect new borrowers, who may face higher interest rates or less favorable repayment terms. For example, if the interest rate on new loans increases, new borrowers may end up paying more over the life of the loan. However, if you already have a loan, your interest rate will likely remain the same.

To understand how the loan change might affect you, consider the following:

- Check your loan documents to see what interest rate and repayment terms you agreed to

- Look for any notices from your lender about changes to your loan terms

- Reach out to your lender or a financial advisor if you have questions about how the loan change will impact your specific situation

By taking these steps, you can get a clear understanding of how the loan change will affect your current student loans and make informed decisions about your finances.

It's also important to note that even if your existing loans are grandfathered in, you may still be able to take advantage of other benefits or programs that can help you manage your debt. For instance, you might be able to consolidate your loans or enroll in an income-driven repayment plan. Be sure to explore your options and ask questions if you're unsure about what's available to you.

Can I still afford to become a doctor or lawyer with the new loan terms?

Pursuing a career in medicine or law can be a costly endeavor, and the new loan terms may seem daunting. However, with careful planning and exploration of alternative funding options, it's still possible to make these careers a reality. By considering factors such as scholarship opportunities, grants, and assistantships, aspiring doctors and lawyers can reduce their reliance on loans.

One key aspect to consider is budgeting strategies that can help manage the financial burden of these careers. Creating a personalized budget that accounts for living expenses, tuition, and other costs can help individuals make informed decisions about their financial situation. For example, cutting back on discretionary spending and allocating funds towards loan repayment or savings can make a significant difference in the long run.

Exploring alternative funding options is also crucial in making these careers more accessible. Some alternatives include:

- Merit-based scholarships, which can provide a significant source of funding for students who excel academically

- Federal and private grants, which can help cover living expenses and other costs associated with pursuing a medical or law degree

- Part-time jobs or internships, which can provide valuable work experience and a steady income while studying

These options can help reduce the financial burden of pursuing a career in medicine or law, making it more feasible for individuals to achieve their goals.

Financial planning is also essential in navigating the new loan terms and making these careers more accessible. By understanding the terms of their loans, including interest rates and repayment schedules, individuals can make informed decisions about their financial situation. For instance, considering income-driven repayment plans or loan forgiveness programs can help alleviate the financial burden of pursuing a medical or law degree.

What can I do to voice my concerns about the loan change?

If you're concerned about the recent loan change, there are several steps you can take to make your voice heard. Contacting your local representatives is a great place to start, as they can provide valuable insight into the decision-making process and potentially advocate on your behalf. You can find your representative's contact information on their official website or through a quick online search.

Participating in advocacy efforts is another effective way to express your concerns and push for change. Many organizations, such as the National Consumer Law Center, offer resources and support for students affected by loan changes. By getting involved with these organizations, you can join a community of like-minded individuals working towards a common goal.

To connect with others who share your concerns, consider joining online forums or social media groups focused on student loan issues. These platforms provide a space to discuss your concerns, ask questions, and learn from others who may be experiencing similar challenges. Some popular online forums include:

- Reddit's r/StudentLoans, where you can engage with a community of students and experts

- Facebook groups dedicated to student loan advocacy and support

- Online forums hosted by organizations specializing in student loan policy and reform

By taking these steps, you can contribute to a larger conversation about student loan policy and potentially influence positive change. Remember to stay informed about the latest developments and updates, and don't be afraid to reach out to others for support and guidance along the way. With persistence and collective action, you can help create a more equitable and sustainable student loan system.