As a young adult, navigating the world of student loans can be overwhelming, especially when it comes to understanding interest rates. It's essential to grasp the concept of interest rates, as they can significantly impact your financial future. For instance, a small difference in interest rates can add up to thousands of dollars over the life of a loan.

When considering student loans, it's crucial to understand how interest rates work and how they can affect your monthly payments. Interest rates can be fixed or variable, and each type has its pros and cons. Fixed interest rates, for example, remain the same over the life of the loan, while variable interest rates may change periodically.

To make informed decisions about your student loans, it's helpful to know the key factors that affect interest rates, including:

- credit score

- loan term

- type of loan (federal or private)

- repayment plan

By understanding these factors, you can better navigate the process of applying for and managing your student loans. This knowledge will also help you create a personalized plan to minimize your debt and maximize your financial stability.

In the following sections, we'll delve deeper into the world of student loan interest rates, exploring topics such as how to compare rates, how to qualify for lower rates, and strategies for paying off high-interest loans. By the end of this guide, you'll be equipped with the knowledge and tools needed to make smart decisions about your student loans and secure a brighter financial future.

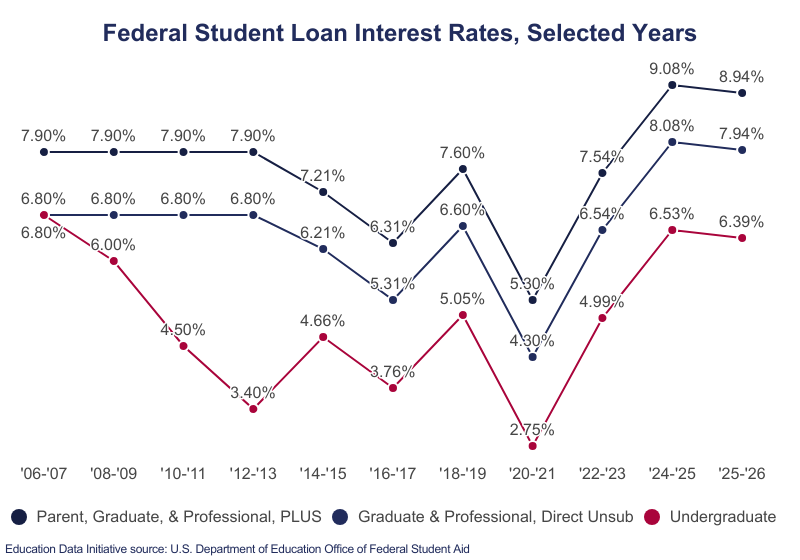

Federal Student Loan Interest Rates 2025

As a student, understanding federal student loan interest rates is crucial for managing your debt. For the 2025 academic year, undergraduate students can expect to pay an interest rate of 5.50% on their federal loans, while graduate students will face a rate of 7.05%. These rates apply to direct unsubsidized loans, which are the most common type of federal student loan.

The current interest rates are slightly higher compared to previous years, which means borrowing costs will increase for students. For instance, in 2022, the interest rate for undergraduate students was 4.99%, so the increase to 5.50% in 2025 will result in higher monthly payments. This rise in interest rates can have a significant impact on the total amount of debt students accumulate over time.

Here are some key factors to consider when it comes to federal student loan interest rates:

- Interest rates are fixed, meaning they remain the same for the life of the loan

- Interest rates can vary depending on the type of loan and the student's degree level

- Interest accrues from the date of disbursement, so it's essential to make timely payments to avoid accumulating too much interest

To illustrate the impact of interest rates on monthly payments, let's consider an example: a student borrowing $10,000 at an interest rate of 5.50% will pay approximately $106 per month for 10 years, while a student borrowing the same amount at 4.99% would pay around $99 per month. This difference may seem small, but it can add up over time, resulting in a higher total debt repayment.

In terms of total debt, the difference in interest rates can be significant. For example, a graduate student borrowing $20,000 at an interest rate of 7.05% will pay around $218 per month for 10 years, resulting in a total repayment of $26,160, while a student borrowing the same amount at 6.54% would pay around $203 per month, resulting in a total repayment of $24,360. By understanding how federal loan interest rates affect monthly payments and total debt, students can make informed decisions about their borrowing and repayment strategies.

Private Student Loan Interest Rates 2025

Private student loan interest rates can vary significantly, typically ranging from around 3.5% to over 12%, depending on the lender and the borrower's creditworthiness. Factors such as credit score, income, and debt-to-income ratio can influence the interest rate offered by a lender. For instance, a borrower with an excellent credit score may qualify for a lower interest rate, such as 4.5%, while a borrower with a poor credit score may be offered a higher rate, such as 10%.

When comparing private loan options, it's essential to consider the rates, terms, and benefits offered by major lenders. Some lenders, like Sallie Mae and Discover, offer competitive interest rates and flexible repayment terms. For example, Sallie Mae's variable interest rate can be as low as 2.50%, while Discover's fixed interest rate can be as low as 4.49%.

Here are some key factors to consider when evaluating private loan options:

- Interest rate type: fixed or variable

- Repayment term: 5, 10, or 15 years

- Fees: origination, late payment, or interest-only repayment fees

- Benefits: cosigner release, forbearance, or death and disability discharge

Lenders like College Ave and SoFi offer unique benefits, such as cosigner release and unemployment protection, which can provide added peace of mind for borrowers.

Private loans might be preferable to federal loans in certain situations, such as when the borrower has already reached the federal loan limit or needs to cover additional education expenses. Additionally, private loans can offer more flexible repayment terms and lower interest rates for borrowers with excellent credit. However, it's crucial to carefully weigh the pros and cons of private loans and consider factors like lack of federal loan forgiveness options and potential higher interest rates over the life of the loan.

To make an informed decision, borrowers should research and compare private loan options from multiple lenders, considering their individual financial situation and needs. By doing so, they can find the most suitable private loan to help fund their education expenses. It's also essential to review and understand the loan agreement terms before signing, as this can help avoid potential pitfalls and ensure a smooth repayment process.

)

Strategies to Manage Student Loan Debt

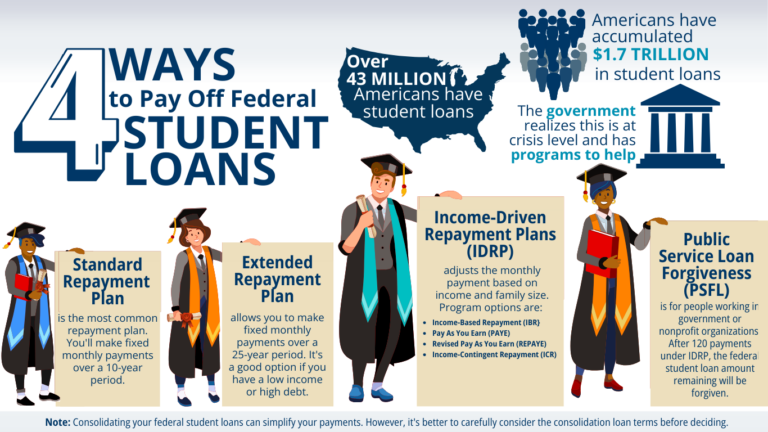

When it comes to managing student loan debt, one effective approach is to explore income-driven repayment plans. These plans can significantly lower your monthly payments by capping them at a percentage of your discretionary income. For instance, the Income-Based Repayment (IBR) plan and the Pay As You Earn (PAYE) plan are popular options that can help make your debt more manageable.

To qualify for these plans, you'll typically need to provide documentation of your income and family size, and your loan servicer will calculate your new monthly payment amount. It's essential to review the terms and conditions of each plan to determine which one best suits your financial situation. You can visit the Federal Student Aid website to learn more about the eligibility criteria and application process.

Another option to consider is the Public Service Loan Forgiveness (PSLF) program, which offers loan forgiveness to borrowers who work in public service jobs. The benefits of PSLF include tax-free loan forgiveness and the potential to have a significant portion of your debt wiped out after 10 years of qualifying payments. To be eligible for PSLF, you must:

- Work full-time for a qualifying employer, such as a government agency or non-profit organization

- Have a Direct Loan or consolidate your loans into a Direct Consolidation Loan

- Be enrolled in a qualifying repayment plan, such as an income-driven plan

By meeting these criteria, you can potentially have your remaining loan balance forgiven after 10 years of qualifying payments.

In addition to exploring income-driven repayment plans and PSLF, you can also accelerate your debt repayment by taking on a side hustle or implementing budgeting strategies. Some ideas for side hustles include freelancing, tutoring, or selling products online. By putting extra money towards your loans each month, you can pay off your debt faster and save on interest. For example, you could try:

- Cutting back on discretionary spending and allocating that money towards your loans

- Using the 50/30/20 rule to allocate 50% of your income towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment

- Considering a bi-weekly payment plan, where you make half payments every two weeks to reduce the principal balance of your loans

By combining these strategies, you can take control of your student loan debt and make progress towards becoming debt-free.

Investing and Building Credit While Repaying Loans

Repaying loans can have a significant impact on your credit score, as it demonstrates your ability to manage debt responsibly. Making timely payments can help improve your credit score over time, while late or missed payments can have a negative effect. For example, setting up automatic payments can help ensure you never miss a payment.

To maintain good credit, it's essential to understand the factors that affect your credit score, such as payment history, credit utilization, and credit age. By keeping credit utilization below 30% and making on-time payments, you can help maintain a healthy credit score. You can also monitor your credit report regularly to catch any errors or discrepancies.

When it comes to investing, starting early is key, especially when it comes to retirement funds. Contributing to a 401(k) or IRA can help you build a safety net for the future, and many employers offer matching contributions to help your savings grow. Even small, regular contributions can add up over time, so it's essential to start as soon as possible.

Some basic investing concepts to consider include:

- Diversifying your portfolio to minimize risk

- Starting with low-cost index funds or ETFs

- Setting clear financial goals, such as saving for a down payment on a house

By understanding these concepts, you can make informed decisions about your investments and create a strategy that works for you.

Balancing loan repayments with saving and investing goals requires careful budgeting and prioritization. Consider using the 50/30/20 rule, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment. You can also explore income-driven repayment plans or loan forgiveness options to help manage your debt burden.

Ultimately, finding a balance between loan repayments, saving, and investing requires patience, discipline, and a long-term perspective. By making smart financial decisions and staying committed to your goals, you can build a strong financial foundation and set yourself up for success in the years to come.

Conclusion and Next Steps

As you navigate the complex world of student loans, it's essential to remember that understanding interest rates and debt management is crucial for making informed decisions. By grasping the basics of interest rates, you can save thousands of dollars over the life of your loan. For instance, a 1% difference in interest rate can result in significant savings, so it's worth exploring your options carefully.

When it comes to managing your debt, it's vital to have a clear plan in place. This includes considering both federal and private loan options, as well as looking into income-driven repayment plans and loan forgiveness programs. By weighing the pros and cons of each option, you can create a personalized plan that works for your unique financial situation.

Some key considerations to keep in mind when exploring loan options include:

- Interest rates and fees associated with each loan

- Repayment terms and flexibility

- Eligibility requirements and application processes

By carefully evaluating these factors, you can make an informed decision that sets you up for long-term financial success.

For personalized financial planning and loan counseling, there are many resources available to help you get started. You can visit the official websites of federal loan programs, such as the Department of Education, or consult with a financial advisor who specializes in student loan planning. Additionally, many non-profit organizations offer free or low-cost counseling services to help you navigate the loan process.

Ultimately, taking control of your student loan debt requires patience, persistence, and a willingness to learn. By staying informed, exploring your options carefully, and seeking out personalized guidance, you can create a debt management plan that works for you and sets you up for long-term financial stability. With the right tools and resources, you can achieve financial freedom and make the most of your investment in higher education.

Frequently Asked Questions (FAQ)

How do federal student loan interest rates impact my monthly payments?

When it comes to managing your student loan debt, understanding how federal student loan interest rates work is crucial. Federal student loan interest rates directly affect your monthly payments, with higher rates resulting in more interest paid over the life of the loan. This means that even a small increase in interest rates can add up to a significant amount over time.

To put this into perspective, consider a student loan of $30,000 with a 10-year repayment period. If the interest rate is 4%, your monthly payment would be around $304. However, if the interest rate increases to 6%, your monthly payment would jump to $333. This increase may not seem like a lot, but it can make a big difference in your budget.

Here are some key things to keep in mind when it comes to federal student loan interest rates and monthly payments:

- Higher interest rates mean more of your monthly payment goes towards interest, rather than the principal amount

- Lower interest rates can save you money over the life of the loan

- Interest rates can vary depending on the type of loan and the borrower's credit score

It's essential to review your loan terms and understand how interest rates will impact your monthly payments. By doing so, you can make informed decisions about your loan and create a budget that works for you.

One practical tip is to consider consolidating your loans or refinancing to a lower interest rate, if possible. This can help reduce your monthly payments and save you money in the long run. Additionally, making extra payments or paying more than the minimum each month can also help you pay off your loan faster and reduce the amount of interest you pay.

Can I refinance my student loans to get a better interest rate?

Refinancing your student loans can be a great way to lower your interest rate and potentially save thousands of dollars over the life of your loan. This process involves working with a private lender to replace your existing loan with a new one that has a lower interest rate and more favorable terms. For example, if you have a federal loan with an interest rate of 6% and you refinance to a private loan with an interest rate of 4%, you could save a significant amount of money in interest payments.

When considering refinancing your student loans, it's essential to weigh the potential benefits against the potential drawbacks. One of the main things to consider is that refinancing federal loans will cause you to lose access to federal loan benefits, such as income-driven repayment plans and forgiveness options. This can be a significant consideration, especially if you're currently using one of these programs to manage your loan payments.

Some of the federal loan benefits you may lose access to if you refinance include:

- Income-driven repayment plans, which can lower your monthly payment amount based on your income and family size

- Public Service Loan Forgiveness, which can forgive your remaining loan balance after you've made a certain number of qualifying payments while working in a public service job

- Deferment and forbearance options, which can temporarily suspend or reduce your loan payments if you're experiencing financial hardship

If you're considering refinancing your student loans, it's crucial to carefully review your options and consider whether the potential savings are worth giving up these benefits. You may also want to speak with a financial advisor or student loan expert to get personalized advice on the best course of action for your situation.

How can I pay off my student loans quickly and efficiently?

To tackle your student loans effectively, it's essential to start by creating a budget that accounts for all your income and expenses. This will help you understand how much you can realistically allocate towards your loan payments each month. By making a budget, you can identify areas where you can cut back on unnecessary spending and direct that money towards your loans.

Considering side hustles is another great way to pay off your student loans quickly, as it can provide a significant boost to your income. For example, you could take up freelancing, part-time jobs, or even sell items you no longer need online. These extra earnings can be directly applied to your loan payments, helping you pay off your debt faster.

When it comes to managing your student loans, there are several strategies you can explore to reduce your interest rate and pay off your debt more efficiently. Some options to consider include:

- Consolidating your loans to combine multiple payments into one

- Refinancing your loans to a lower interest rate, which can save you money over time

- Looking into income-driven repayment plans, which can lower your monthly payments based on your income

By exploring these options and finding the one that works best for you, you can simplify your loan payments and make progress towards becoming debt-free.

In addition to these strategies, it's also important to stay organized and keep track of your loan payments and progress. You can use a spreadsheet or a budgeting app to monitor your payments and make adjustments as needed. By staying on top of your loans and making consistent payments, you can pay off your debt quickly and efficiently, and start building a more secure financial future.