As a young adult, building wealth may seem like a daunting task, especially without a side hustle. However, there are ways to create a silent wealth-building formula that can help you achieve financial stability and security. By making a few simple changes to your daily habits and financial decisions, you can set yourself up for long-term success.

One of the key components of this formula is to start small and be consistent. This can involve setting aside a fixed amount each month, such as $100, and putting it towards a savings or investment account. Over time, this can add up and provide a significant boost to your finances.

Some examples of silent wealth-building strategies include:

- Automating your savings to ensure that you save a fixed amount regularly

- Taking advantage of compound interest by starting to save early

- Investing in a diversified portfolio to minimize risk and maximize returns

By implementing these strategies, you can create a wealth-building formula that works for you, even without a side hustle.

It's also important to note that building wealth is a marathon, not a sprint. It requires patience, discipline, and a long-term perspective. By focusing on making progress, rather than trying to get rich quickly, you can create a sustainable and reliable path to financial success.

To get started, begin by tracking your expenses and creating a budget that accounts for your income and spending. This will help you identify areas where you can cut back and allocate more funds towards savings and investments. From there, you can start to build a silent wealth-building formula that works for you and helps you achieve your financial goals.

Understanding the Wealth Formula

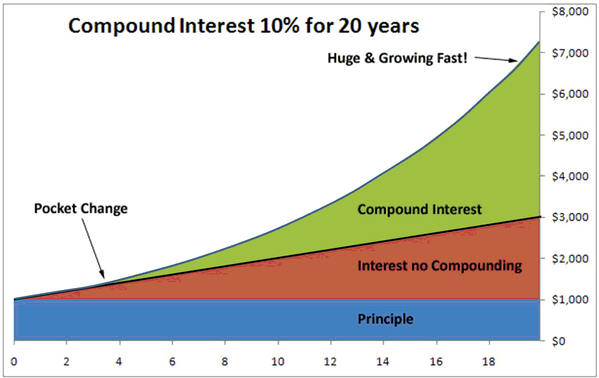

The concept of compound interest is a powerful force in wealth creation, allowing your investments to grow exponentially over time. As your money earns interest, that interest is then added to your principal, creating a snowball effect that can lead to significant wealth. By harnessing the power of compound interest, you can turn small, regular investments into a substantial nest egg.

To maximize the benefits of compound interest, it's essential to start early and be consistent in your investments. The sooner you begin, the more time your money has to grow, and even small, regular investments can add up to significant wealth. For example, investing just $100 per month from age 25 to 65 can result in a substantial sum, thanks to the power of compound interest.

Some key principles to keep in mind when it comes to building wealth over time include:

- Starting early, to give your investments time to grow

- Being consistent, to take advantage of dollar-cost averaging and reduce risk

- Being patient, to allow compound interest to work its magic

By following these principles and making small, regular investments, you can set yourself up for long-term financial success.

To illustrate the power of small, regular investments, consider the example of a college student who invests just $50 per month in a retirement account, starting at age 20. Over the course of 45 years, this small monthly investment can add up to a significant sum, potentially exceeding $100,000. This demonstrates the potential for small, consistent investments to lead to substantial wealth over time, making it an essential part of any long-term financial plan.

In terms of practical tips, it's essential to take advantage of tax-advantaged accounts, such as 401(k) or IRA, to maximize your investment returns. Additionally, consider setting up automatic transfers from your checking account to your investment account, to make investing a habit and ensure consistency. By following these tips and harnessing the power of compound interest, you can set yourself up for long-term financial success and achieve your wealth goals.

Budgeting for Wealth Creation

When it comes to building wealth, creating a budget is the first step towards achieving your financial goals. A well-crafted budget helps you understand where your money is going and makes it easier to allocate funds for investments. By prioritizing investments, you can set yourself up for long-term financial success.

The 50/30/20 rule is a popular guideline for allocating your income towards different expenses. This rule suggests that 50% of your income should go towards necessary expenses like rent, utilities, and groceries, 30% towards discretionary spending, and 20% towards saving and investing. By following this rule, you can ensure that you're setting aside a significant portion of your income for wealth creation.

To apply the 50/30/20 rule, start by tracking your income and expenses to see where your money is going. Then, make adjustments to allocate 20% of your income towards investments, such as:

- Retirement accounts, like 401(k) or IRA

- Stocks, bonds, or mutual funds

- Real estate investments, like rental properties or REITs

By investing in these assets, you can grow your wealth over time and achieve your long-term financial goals.

Reducing expenses is another key aspect of budgeting for wealth creation. By cutting back on unnecessary expenses, you can free up more money to invest in your future. Some practical tips for reducing expenses include:

- Cooking at home instead of eating out

- Cancelling subscription services you don't use

- Negotiating a lower rate with service providers, like your cable or phone company

By implementing these strategies, you can save money and allocate it towards investments, setting yourself up for long-term financial success.

As you create your budget, remember to review and adjust it regularly to ensure you're on track to meet your financial goals. With time and discipline, you can build wealth and achieve financial freedom. By prioritizing investments and reducing expenses, you can set yourself up for a brighter financial future.

Investing Without a Side Hustle

Investing in the stock market can seem daunting, especially for those without a side hustle to generate extra income. However, there are several low-maintenance investment options available that can help you get started, such as index funds or ETFs, which track a specific market index, like the S&P 500. These options require minimal effort and can provide broad diversification, making them an excellent choice for beginners.

To make the most of your investments, it's essential to utilize tax-advantaged accounts, such as a 401(k) or IRA, which offer tax benefits that can help your investments grow faster. For example, contributing to a 401(k) can reduce your taxable income, while an IRA provides tax-deferred growth, meaning you won't have to pay taxes on your investments until you withdraw the funds. This can be a significant advantage, especially for long-term investments.

Some key tax-advantaged accounts to consider include:

- 401(k) or 403(b) plans, which are often offered by employers

- Individual Retirement Accounts (IRAs), such as traditional or Roth IRAs

- Thrift Savings Plans, which are available to federal employees and members of the military

These accounts can help you save for retirement while reducing your tax liability, making it easier to invest for the future.

Dollar-cost averaging is another strategy that can help reduce investment risk by investing a fixed amount of money at regular intervals, regardless of the market's performance. This approach can help you smooth out market fluctuations and avoid trying to time the market, which can be a costly mistake. For instance, investing $100 per month in a diversified portfolio can help you take advantage of lower prices during market downturns, potentially leading to higher returns over the long term.

By combining tax-advantaged accounts with dollar-cost averaging and low-maintenance investment options, you can create a solid foundation for your investment portfolio, even without a side hustle. Remember to start small, be consistent, and patient, and you'll be on your way to building wealth over time. As with any investment strategy, it's essential to educate yourself and consider your individual financial goals and risk tolerance before making any investment decisions.

Avoiding Debt for Financial Health

Avoiding debt is crucial for achieving long-term financial health, as it can save you from paying excessive interest rates and free up more money in your budget for savings and investments. High-interest debt, in particular, can be a significant obstacle to financial stability, making it essential to prioritize debt repayment. For instance, credit card debt can have interest rates as high as 20%, which can quickly add up and make it challenging to pay off the principal amount.

To pay off existing debt, there are several strategies you can use, including the snowball and avalanche methods. The snowball method involves paying off debts with the smallest balances first, while the avalanche method focuses on paying off debts with the highest interest rates first. Both methods can be effective, and the key is to find the approach that works best for your financial situation and personality.

Some practical tips for paying off debt include:

- Creating a budget that accounts for all your income and expenses

- Cutting back on non-essential expenses to free up more money for debt repayment

- Considering a balance transfer or debt consolidation loan to simplify your payments and potentially lower your interest rate

By following these tips and staying committed to your debt repayment plan, you can make significant progress towards becoming debt-free and improving your overall financial health.

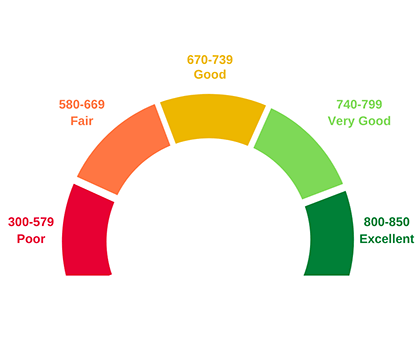

Maintaining a good credit score is also essential for better financial opportunities, such as qualifying for lower interest rates on loans and credit cards. To maintain a good credit score, it's essential to make on-time payments, keep your credit utilization ratio low, and avoid applying for too much credit at once. You can also monitor your credit report regularly to ensure it's accurate and up-to-date, which can help you identify any potential issues or errors that may be affecting your credit score.

In addition to paying off debt and maintaining a good credit score, it's also important to build an emergency fund to protect yourself from unexpected expenses and avoid going further into debt. Aim to save three to six months' worth of living expenses in a easily accessible savings account, which can provide a cushion in case of job loss, medical emergencies, or other financial setbacks. By taking these steps, you can improve your financial stability and set yourself up for long-term success.

Staying Disciplined and Patient

When it comes to managing your finances, staying disciplined is crucial for achieving your long-term goals. This involves setting clear objectives and avoiding impulsive decisions based on emotions. By creating a well-structured investment and budgeting plan, you can develop the discipline needed to stick to your goals.

Developing a disciplined mindset requires an understanding of the psychological aspects that drive financial decisions. For instance, the fear of missing out (FOMO) can lead to reckless investments in get-rich-quick schemes, which often end in financial losses. To avoid this, it's essential to educate yourself on the risks associated with such schemes and focus on tried-and-tested investment strategies.

Some common pitfalls to watch out for include:

- Investing in unverified investment opportunities

- Chasing high returns without considering the risks

- Overleveraging your finances to make quick gains

These mistakes can be avoided by adopting a patient and informed approach to investing, where you prioritize long-term growth over short-term gains.

Patience is a vital virtue in wealth creation, as it allows you to ride out market fluctuations and avoid making impulsive decisions. By taking a long-term perspective, you can focus on steady, consistent growth rather than trying to time the market or make quick profits. For example, investing in a diversified portfolio of stocks, bonds, and other assets can provide a stable foundation for long-term wealth creation.

To cultivate patience, it's essential to set realistic expectations and celebrate small milestones along the way. This can involve tracking your progress, learning from your mistakes, and adjusting your strategy as needed. By doing so, you can develop the discipline and patience required to achieve your financial goals and create lasting wealth.

Embracing a long-term perspective also involves avoiding the temptation to constantly monitor your investments and make emotional decisions based on short-term market movements. Instead, focus on the bigger picture and trust in your well-researched investment plan to deliver results over time. With patience and discipline, you can overcome the psychological hurdles that often stand in the way of financial success.

Frequently Asked Questions (FAQ)

Do I need a side hustle to build wealth?

Building wealth often seems like a daunting task, but it's achievable through consistent investing and smart financial planning. By setting clear financial goals and creating a tailored plan, you can silently build wealth over time without necessarily needing a side hustle. For instance, automating your investments can help you save and grow your money consistently, even with a modest income.

Many people believe that having a side hustle is the only way to build wealth quickly, but this isn't always the case. With a solid understanding of investing and financial planning, you can make the most of your money and create a stable financial foundation. A key aspect of this is understanding the power of compound interest, which can help your investments grow exponentially over time.

To get started, consider the following essential steps:

- Set clear financial goals, such as saving for a down payment on a house or retirement

- Create a budget that accounts for all your expenses and savings

- Automate your investments to ensure consistent saving and growth

By following these steps and staying committed to your financial plan, you can build wealth over time without relying on a side hustle. It's also important to stay informed about personal finance and investing, and to continually educate yourself on the best strategies for achieving your financial goals.

Practical tips, such as taking advantage of tax-advantaged retirement accounts and avoiding lifestyle inflation, can also help you build wealth silently. By living below your means and investing your savings wisely, you can create a stable financial foundation that will serve you well in the long term. Additionally, avoiding debt and building an emergency fund can help you stay on track and achieve your financial goals, even in the face of unexpected expenses or financial setbacks.

How do I start investing with little money?

When it comes to investing, many people think they need a lot of money to get started, but the truth is, you can begin with a small amount. Start by allocating a small percentage of your income into low-maintenance investment options, such as index funds or exchange-traded funds (ETFs). This approach allows you to dip your toes into the world of investing without breaking the bank.

To make the most of your limited funds, consider setting up a monthly automatic transfer from your checking account to your investment account. This way, you'll ensure that you're investing a fixed amount regularly, without having to think about it. For example, you could start by transferring $50 or $100 per month into a high-yield savings account or a micro-investing app.

Some popular low-maintenance investment options for beginners include:

- Index funds, which track a specific market index, such as the S&P 500

- ETFs, which are similar to index funds but trade on an exchange like stocks

- Micro-investing apps, which allow you to invest small amounts of money into a diversified portfolio

These options are great for beginners because they offer broad diversification and typically require minimal effort to manage.

As you get started, it's essential to keep in mind that investing is a long-term game, and it's essential to be patient and disciplined. Avoid putting all your eggs in one basket, and instead, focus on building a diversified portfolio over time. By starting small and being consistent, you can set yourself up for long-term financial success and make the most of your limited funds.

What is the most important factor in wealth creation?

When it comes to building wealth, many people think that making a lot of money is the most important factor. However, this is not entirely true. Starting early and being consistent are key factors in successful wealth creation, as they allow you to take advantage of compound interest and make the most of your money over time.

Consistency is crucial because it helps you develop a habit of saving and investing regularly. This can be as simple as setting aside a fixed amount each month, or taking advantage of automated investment plans that transfer a portion of your paycheck into a savings or investment account. By doing so, you can make steady progress towards your financial goals without having to think about it too much.

Some of the benefits of starting early and being consistent include:

- Compound interest: this allows your savings to grow exponentially over time, even with small monthly contributions

- Reduced financial stress: by saving and investing regularly, you can avoid worrying about money and feel more secure in your financial future

- Increased financial flexibility: having a cushion of savings and investments gives you the freedom to pursue opportunities and make choices that align with your values and goals

For example, if you start saving $100 per month at age 25, you could have over $100,000 by the time you're 50, assuming a 5% annual return. This may not seem like a lot, but it's a great starting point, and you can always increase your contributions over time as your income grows.

To get started with consistent wealth creation, consider setting clear financial goals and making a plan to achieve them. This could involve creating a budget, paying off high-interest debt, and opening a retirement or investment account. By taking these steps and sticking to your plan, you can set yourself up for long-term financial success and make the most of your money.