As a young adult, navigating the world of student loans can be overwhelming, but understanding your options is crucial for making informed decisions. Sallie Mae student loans are one of the most popular choices among students, offering a range of borrowing options to help fund higher education. With a long history of providing financial assistance, Sallie Mae has become a trusted name in the student loan industry.

For many students, Sallie Mae student loans provide a vital source of funding, helping to bridge the gap between available savings and the total cost of attending college. These loans can be used to cover a variety of expenses, including tuition, room and board, and other education-related costs. By exploring Sallie Mae's loan options, students can create a personalized plan to achieve their academic goals.

Some key benefits of Sallie Mae student loans include:

- Competitive interest rates and flexible repayment terms

- No origination fees or prepayment penalties

- Multiple repayment options to suit different financial situations

These features can help students manage their debt effectively and make timely payments, which is essential for maintaining a healthy credit score.

When considering Sallie Mae student loans, it's essential to evaluate your individual financial circumstances and academic goals. By doing so, you can determine which loan options are best suited to your needs and create a plan to achieve financial stability after graduation. For example, students can take advantage of Sallie Mae's online resources and tools to estimate their loan payments and explore different repayment scenarios.

Overview of Sallie Mae Student Loans

As a leading provider of student loans, Sallie Mae offers a range of options to help students finance their education. Undergraduate and graduate loans are available, allowing students to borrow money to cover tuition, fees, and other expenses. For example, undergraduate students can use Sallie Mae loans to pay for textbooks, room, and board.

To be eligible for a Sallie Mae student loan, applicants must meet certain criteria, including being a U.S. citizen or permanent resident, being enrolled in a degree-granting program, and having a good credit history. The application process typically involves filling out an online application, providing personal and financial information, and agreeing to the loan terms. It's essential to review and understand the terms before applying.

The loan terms offered by Sallie Mae vary depending on the type of loan and the borrower's creditworthiness. Interest rates can range from around 2% to over 12%, and repayment options include fixed and variable rates, as well as deferred payment plans. Some key features of Sallie Mae loans include:

- Competitive interest rates and no origination fees

- Flexible repayment terms, including income-driven repayment plans

- Multiple repayment options, such as fixed and variable rates

Sallie Mae also offers a range of repayment options, including the option to defer payments while in school or during economic hardship. Borrowers can choose from various repayment plans, such as the standard repayment plan or the graduated repayment plan, which allows for lower payments in the early years of repayment. It's crucial to carefully review the repayment options and choose the one that best fits your financial situation.

In addition to the loan terms, Sallie Mae provides resources and tools to help borrowers manage their debt and make informed financial decisions. For instance, borrowers can use the Sallie Mae website to track their loan balances, make payments, and access financial education materials. By understanding the loan terms and using these resources, borrowers can make the most of their Sallie Mae student loan and achieve their financial goals.

Benefits and Drawbacks of Sallie Mae Student Loans

When considering Sallie Mae student loans, it's essential to weigh the advantages and disadvantages. One of the significant benefits is the competitive interest rates offered, which can help keep borrowing costs low. For instance, a lower interest rate can save you hundreds or even thousands of dollars over the life of the loan.

Flexible repayment plans are another advantage of Sallie Mae student loans, allowing you to choose from various options that fit your financial situation. This can include deferred payments, income-driven repayment, or fixed monthly payments. By selecting a repayment plan that aligns with your budget, you can avoid default and make timely payments.

Some of the benefits of Sallie Mae student loans include:

- Competitive interest rates that can help reduce borrowing costs

- Flexible repayment plans to accommodate different financial situations

- No origination fees for most loan products

These benefits can make Sallie Mae a attractive option for students and families seeking financial assistance.

However, there are also some drawbacks to consider when evaluating Sallie Mae student loans. One of the notable disadvantages is the potential fees associated with late payments or returned checks. Additionally, Sallie Mae's forbearance options may be limited, which can make it challenging to temporarily suspend payments during financial hardship.

In comparison to other lenders, Sallie Mae student loans offer some unique features, but may not always be the best option. For example, some lenders may offer more generous forbearance policies or lower interest rates for borrowers with excellent credit. It's crucial to research and compare the offerings of different lenders, including:

- Discover Student Loans

- Wells Fargo Student Loans

- College Ave Student Loans

By evaluating the pros and cons of each lender, you can make an informed decision that suits your financial needs and goals.

To get the most out of a Sallie Mae student loan, it's essential to carefully review the terms and conditions before signing the agreement. This includes understanding the interest rate, repayment terms, and any potential fees associated with the loan. By doing your research and choosing the right loan product, you can minimize borrowing costs and set yourself up for long-term financial success.

Managing Sallie Mae Student Loan Debt

Creating a budget is a crucial step in managing Sallie Mae student loan debt. Start by tracking your income and expenses to understand where your money is going, and then allocate a specific amount for loan payments. This will help you stay on top of your payments and avoid missing any.

To prioritize payments, consider the snowball method, where you pay off loans with the smallest balances first, or the avalanche method, where you focus on loans with the highest interest rates. Both approaches can be effective, so choose the one that works best for your financial situation. For example, if you have a loan with a 6% interest rate and another with a 4% interest rate, you may want to prioritize the loan with the 6% interest rate.

Making timely payments is essential to avoid late fees and negative credit reporting. Late fees can add up quickly, so it's vital to set up automatic payments or reminders to ensure you never miss a payment. By making timely payments, you can also build a positive credit history, which can help you qualify for better loan terms in the future.

Here are some additional tips for managing Sallie Mae student loan debt:

- Consider enrolling in an income-driven repayment plan, which can lower your monthly payments based on your income and family size.

- Look into forgiveness programs, such as Public Service Loan Forgiveness, which can forgive part or all of your loan balance after a certain number of payments.

- Keep track of your loan statements and correspondence from Sallie Mae to stay informed about your loan status and any changes to your repayment terms.

Refinancing or consolidating Sallie Mae student loans can be a good option for some borrowers. Refinancing involves taking out a new loan with a lower interest rate to pay off your existing loans, while consolidation involves combining multiple loans into a single loan with a single interest rate and payment. For example, if you have multiple loans with high interest rates, refinancing or consolidating them into a single loan with a lower interest rate can save you money on interest and simplify your payments. Be sure to carefully review the terms and conditions of any refinancing or consolidation option before making a decision.

Alternatives to Sallie Mae Student Loans

When it comes to funding your education, Sallie Mae is not the only option available. Students can explore alternative options such as scholarships, grants, and federal student loans, which can provide more favorable terms and lower interest rates. For instance, the Federal Pell Grant is a need-based grant that can help undergraduate students cover their tuition fees.

Scholarships are another excellent way to fund your education, and they can be merit-based or need-based. Students can search for scholarships on websites such as Fastweb or Scholarships.com, which offer a wide range of scholarship opportunities. By applying for multiple scholarships, students can increase their chances of receiving funding for their education.

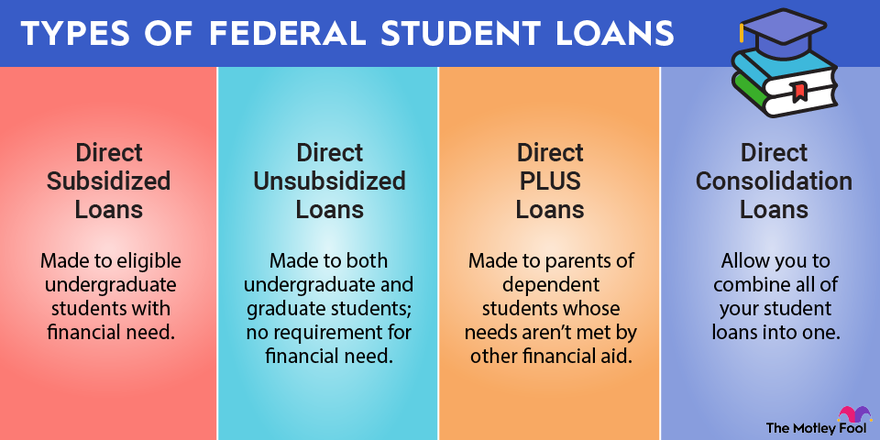

In addition to scholarships and grants, federal student loans are a popular alternative to Sallie Mae loans. Federal student loans offer benefits such as lower interest rates, income-driven repayment plans, and forgiveness options. Some examples of federal student loans include:

- Direct Subsidized Loans

- Direct Unsubsidized Loans

- Perkins Loans

These loans can help students cover their education expenses without having to rely on private lenders like Sallie Mae.

Using alternative lenders or credit cards to fund education expenses can be tempting, but it's essential to weigh the benefits and drawbacks. Alternative lenders may offer more flexible repayment terms, but they often come with higher interest rates and fees. Credit cards, on the other hand, can provide quick access to cash, but they can lead to debt traps and negative credit scores if not managed properly.

To explore and compare alternative funding options, students can start by researching online and reaching out to their school's financial aid office. They can also use online tools such as the College Board's Net Price Calculator to estimate their education costs and explore funding options. By taking the time to compare and contrast different funding options, students can make informed decisions about how to fund their education and avoid costly mistakes.

Frequently Asked Questions (FAQ)

What are the interest rates for Sallie Mae student loans?

When it comes to Sallie Mae student loans, interest rates play a crucial role in determining the overall cost of borrowing. Sallie Mae student loan interest rates vary depending on the type of loan and the borrower's creditworthiness. This means that students with a good credit score can qualify for lower interest rates, while those with a poor credit score may face higher rates.

The type of loan also affects the interest rate, with options like variable and fixed rates available. For instance, variable rates may start lower but can increase over time, while fixed rates remain the same throughout the loan term. It's essential to understand the differences between these rates to make an informed decision.

Some of the key factors that influence Sallie Mae student loan interest rates include:

- Credit score: A good credit score can lead to lower interest rates

- Loan type: Variable or fixed rates, and the specific loan product chosen

- Repayment term: Longer repayment terms may result in higher interest rates

By considering these factors, borrowers can better navigate the interest rate landscape and choose the best loan option for their needs.

To give you a better idea, Sallie Mae offers a range of interest rates, from around 2.50% to over 12.00%, depending on the loan and borrower. It's crucial to review the terms and conditions of each loan carefully and consider factors like origination fees and repayment options. By doing your research and comparing rates, you can find the most affordable Sallie Mae student loan for your educational expenses.

Can I refinance my Sallie Mae student loans?

Refinancing your student loans can be a great way to save money and simplify your finances. If you have Sallie Mae student loans, you may be wondering if you can refinance them. The good news is that Sallie Mae does offer refinancing options for existing student loans, which can help lower interest rates or monthly payments.

To refinance your Sallie Mae student loans, you'll typically need to meet certain eligibility requirements, such as having a good credit score and a steady income. You can check your eligibility on the Sallie Mae website or by contacting their customer service team. They will guide you through the process and help you determine if refinancing is right for you.

Some benefits of refinancing your Sallie Mae student loans include:

- Lower interest rates, which can save you money over the life of the loan

- Lower monthly payments, which can help you free up more money in your budget

- A single, simplified loan payment, which can make it easier to manage your finances

For example, let's say you have a $30,000 Sallie Mae student loan with an interest rate of 6% and a monthly payment of $333. If you refinance the loan to a 4% interest rate, your monthly payment could drop to $299, saving you $34 per month.

Before refinancing your Sallie Mae student loans, it's essential to consider your individual financial situation and goals. You may want to weigh the pros and cons of refinancing, such as potentially losing certain benefits like income-driven repayment plans. By doing your research and carefully evaluating your options, you can make an informed decision that's right for you.

It's also important to note that Sallie Mae offers various refinancing options, so it's crucial to compare rates and terms before making a decision. You can visit the Sallie Mae website or consult with a financial advisor to determine the best course of action for your specific situation.

How do I apply for a Sallie Mae student loan?

To get started with the application process, visit the Sallie Mae website and click on the "Apply Now" button. This will direct you to an online application form where you'll be asked to provide some basic information, such as your name, address, and date of birth. Make sure you have all the necessary documents ready, including your social security number and driver's license.

The online application process typically takes around 15-30 minutes to complete, depending on the type of loan you're applying for and the amount of information you need to provide. You'll be asked to provide details about your financial situation, including your income, expenses, and any existing debts. It's a good idea to have your financial documents, such as pay stubs and bank statements, readily available to make the process smoother.

Here are some key steps to follow during the application process:

- Provide accurate and complete personal and financial information to avoid any delays or complications

- Choose the correct loan option that suits your needs, such as an undergraduate or graduate loan

- Review and agree to the terms and conditions of the loan, including the interest rate and repayment terms

By following these steps and providing the required information, you can complete the application process and receive a decision on your loan eligibility. If you have any questions or need help during the application process, you can contact Sallie Mae's customer support team for assistance.