As a recent graduate, you're likely no stranger to the financial burden of student loans. The weight of debt can be overwhelming, making it difficult to plan for the future or achieve financial stability. For many, the key to managing this debt lies in creating a solid repayment plan.

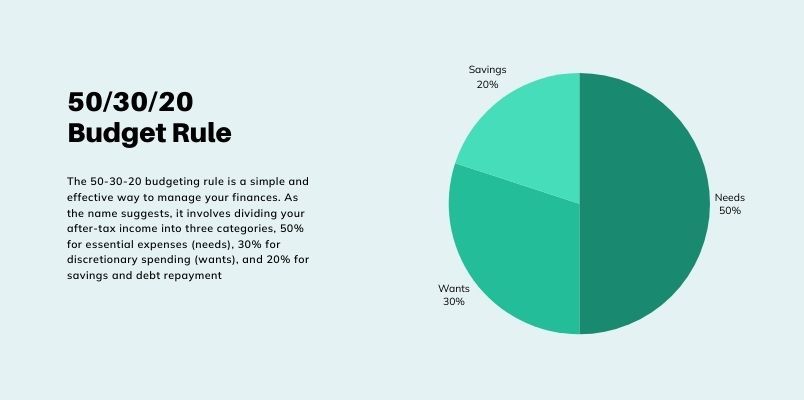

To understand the importance of a repayment plan, consider the long-term implications of student loan debt. Without a clear plan, borrowers may struggle to make timely payments, leading to accrued interest and a longer repayment period. This can result in paying significantly more than the initial loan amount.

Some benefits of having a repayment plan include:

- Reduced financial stress and anxiety

- Improved credit scores through timely payments

- Increased financial flexibility and freedom

By prioritizing debt repayment and making informed financial decisions, graduates can set themselves up for long-term success and stability.

When creating a repayment plan, it's essential to consider factors such as income, expenses, and interest rates. For example, borrowers with high-interest loans may want to focus on paying those off first, while others may prioritize loans with smaller balances. By tailoring a repayment plan to individual financial circumstances, graduates can make steady progress towards becoming debt-free.

Understanding Your Student Loans

When it comes to managing your student loans, the first step is to calculate the total amount owed, including principal and interest. This will give you a clear understanding of the scope of your debt and help you create a plan to tackle it. For instance, if you have a loan with a principal amount of $10,000 and an interest rate of 4%, you can expect to pay around $1,000 in interest over a 10-year repayment period.

To get started, you'll need to identify the types of loans you have, such as federal or private, and their respective interest rates. This information can usually be found on your loan documents or by logging into your loan servicer's website. Federal loans, like Stafford or Perkins loans, typically have lower interest rates compared to private loans from banks or credit unions.

Here are some key factors to consider when reviewing your loans:

- Federal loans: These loans are funded by the government and often have more flexible repayment terms and lower interest rates.

- Private loans: These loans are issued by banks, credit unions, or other private lenders and may have higher interest rates and less flexible repayment terms.

- Interest rates: These can range from around 3% to over 12%, depending on the type of loan and your credit score.

Determine the repayment terms and grace periods for each loan to understand when you need to start making payments and how much you'll need to pay each month. For example, federal loans often have a six-month grace period after graduation, while private loans may require payments to start immediately. By reviewing your loan documents and creating a repayment plan, you can stay on top of your debt and make progress towards becoming debt-free.

It's also essential to review your loan statements regularly to ensure you're on track with your payments and to identify any potential issues, such as late fees or changes to your interest rate. By staying informed and proactive, you can take control of your student loans and make the most of your financial situation.

Creating a Repayment Strategy

When it comes to managing your debt, having a solid repayment strategy in place is crucial. Consider income-driven repayment plans, which can help lower your monthly payments and make them more manageable. For instance, if you're a recent graduate with a limited income, an income-driven plan can cap your monthly payments at a percentage of your discretionary income.

To simplify your loan management, look into loan consolidation or refinancing options. These can combine multiple loans into one, potentially lowering your interest rates and reducing the number of payments you need to make each month. This can be especially helpful if you have multiple loans with different interest rates and payment due dates.

Some options to explore include:

- Income-driven repayment plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE)

- Loan consolidation, which can combine multiple federal loans into one

- Refinancing, which can help you secure a lower interest rate and lower monthly payments

It's essential to weigh the pros and cons of each option and consider factors like interest rates, fees, and repayment terms.

If you work in a public service field, such as teaching, nursing, or government, you may be eligible for forgiveness programs. Programs like Public Service Loan Forgiveness (PSLF) can forgive a portion of your loan balance after a certain number of qualifying payments. To qualify, you'll need to meet specific requirements, such as working full-time for a qualifying employer and making 120 qualifying payments.

Exploring forgiveness programs can be a great way to reduce your debt burden and free up more money in your budget for other expenses. Be sure to research the eligibility criteria and application process for programs like PSLF, and don't hesitate to reach out to your loan servicer or a financial advisor for guidance. By taking a proactive approach to managing your loans, you can create a repayment strategy that works for you and helps you achieve financial stability.

Boosting Income to Pay Off Loans Faster

To pay off loans faster, it's essential to focus on increasing your monthly income. Developing a side hustle can be a great way to do this, as it allows you to earn extra money on top of your regular salary. For example, you could try freelancing or taking on a part-time job to boost your earnings.

Some popular side hustles include writing, graphic design, and tutoring, which can be done remotely and on a flexible schedule. You can use platforms like Upwork or Fiverr to find freelance work, or reach out to friends and family to see if they know of any part-time job opportunities. By dedicating just a few hours a week to a side hustle, you can significantly increase your monthly income.

In addition to developing a side hustle, you may also be able to negotiate a salary increase at your current job. To do this, you'll need to highlight your value to the company and make a solid case for why you deserve a raise. Here are some tips to keep in mind:

- Make a list of your accomplishments and the ways in which you've contributed to the company's success

- Research the market rate for your position to determine a fair salary range

- Practice your negotiation skills so you feel confident and prepared

By negotiating a salary increase, you can earn more money each month and put it towards your loans.

Another option for paying off loans faster is to sell unwanted items or assets to make a lump sum payment. This could be anything from an old car or piece of furniture to a collection of unused electronics or jewelry. You can use online marketplaces like eBay or Craigslist to sell your items, or hold a yard sale to get rid of multiple things at once. By putting the proceeds from these sales towards your loans, you can make a significant dent in your debt and get back on track financially.

Maintaining Financial Health During Repayment

When it comes to maintaining financial health during repayment, having a safety net is crucial. This is where an emergency fund comes in - a cushion that helps you cover unexpected expenses without going further into debt. By saving 3-6 months' worth of living expenses, you can ensure that you can still meet your repayment obligations even if you encounter a financial setback.

To build a healthy emergency fund, consider setting aside a fixed amount each month, such as $500 or $1000, until you reach your target. You can also take advantage of high-yield savings accounts, which offer higher interest rates than traditional savings accounts, to grow your fund over time. For example, if you save $500 per month for 6 months, you'll have a total of $3000 in your emergency fund.

Monitoring your credit scores and reports is also essential during repayment. You can check your credit report for free from the three major credit bureaus - Equifax, Experian, and TransUnion - to ensure that all the information is accurate and up-to-date. Here are some tips to keep in mind:

- Check your credit report at least once a year to catch any errors or discrepancies

- Dispute any inaccuracies you find and work to resolve them as quickly as possible

- Keep an eye on your credit utilization ratio, which should be below 30% to maintain a good credit history

Avoiding new debt during the repayment period is also critical to maintaining financial health. This means being mindful of your spending habits and avoiding the temptation to take on new credit cards or personal loans. Instead, focus on paying off your existing debt as quickly as possible, and consider using the snowball method or avalanche method to pay off your debts one by one. By staying focused and disciplined, you can avoid accumulating more debt and make steady progress towards becoming debt-free.

Staying Motivated and Accountable

Staying on track with your financial goals can be challenging, but having a support system can make a big difference. Sharing your repayment goals with a friend or family member can provide an added motivation to stick to your plan, as you'll have someone to report back to and stay accountable. This can be as simple as sending a monthly update to a friend or family member, detailing your progress and any challenges you're facing.

Celebrating milestones is also crucial in maintaining momentum and motivation. This can be done by treating yourself to something special after paying off a certain amount or completing a year of payments. For example, you could plan a weekend getaway or a nice dinner to mark the occasion, giving you something to look forward to and reinforcing the idea that your hard work is paying off.

Using budgeting apps or spreadsheets to track progress and stay organized is another effective way to stay motivated. Some popular budgeting apps include Mint, You Need a Budget (YNAB), and Personal Capital, which offer features such as automated expense tracking and bill reminders. Here are some ways to use these tools to your advantage:

- Set up regular budget reviews to assess your spending and make adjustments as needed

- Use the apps' built-in goal-setting features to create a plan for paying off debt or building savings

- Take advantage of alerts and notifications to stay on top of upcoming payments and deadlines

By leveraging these tools and strategies, you can stay on top of your finances and make steady progress towards your goals.

Frequently Asked Questions (FAQ)

How do I know which repayment plan is best for me?

When it comes to choosing a repayment plan, it's essential to consider your individual financial situation. Consulting with a financial advisor can provide personalized guidance and help you make an informed decision. They can assess your income, expenses, and debt to recommend the most suitable plan for your needs.

Alternatively, you can use online tools to compare repayment plans and find the one that best fits your budget. These tools often provide calculators and quizzes to help you determine which plan is most suitable for you. For example, you can use a debt repayment calculator to see how different plans will impact your monthly payments.

To get started, consider the following steps:

- Make a list of your income and expenses to understand your financial situation

- Research different repayment plans, such as income-driven repayment or graduated repayment

- Use online tools or consult with a financial advisor to compare plans and choose the best one for you

By taking the time to evaluate your options and choose a plan that aligns with your financial goals, you can ensure a smoother and more manageable repayment process.

It's also important to consider your long-term financial goals and how your repayment plan will impact your ability to achieve them. For instance, if you're trying to save for a down payment on a house, you may want to choose a plan with lower monthly payments to free up more money in your budget. By prioritizing your goals and choosing a repayment plan that supports them, you can set yourself up for financial success.

Can I refinance my student loans with bad credit?

Refinancing student loans can be a great way to simplify your finances and potentially lower your monthly payments. However, if you have bad credit, refinancing might seem like a daunting task. Fortunately, some lenders offer options that can help you refinance your student loans even with a less-than-ideal credit score.

When refinancing with bad credit, having a co-signer with good credit can significantly improve your chances of approval. This is because the lender will consider the co-signer's credit history in addition to yours, which can help offset the risk. For example, a parent or spouse with good credit could co-sign your loan, making it more likely that you'll qualify for a refinancing option.

Some lenders also consider factors beyond your credit score when evaluating your refinancing application. These may include:

- Income and employment history

- Debt-to-income ratio

- Payment history on existing student loans

By taking a more holistic approach to evaluating borrowers, these lenders can offer refinancing options to individuals who might not qualify based on credit score alone.

To increase your chances of refinancing with bad credit, it's essential to shop around and compare rates from multiple lenders. You may also want to consider working on improving your credit score before applying, as this can help you qualify for better interest rates and terms. By doing your research and exploring your options, you can find a refinancing solution that works for you, even with bad credit.

Are there any tax benefits to paying off student loans?

When it comes to paying off student loans, many individuals are looking for ways to reduce their financial burden. One often overlooked benefit is the potential for tax deductions on the interest paid towards these loans. This can help decrease taxable income, resulting in a lower overall tax liability.

To qualify for this deduction, you will need to meet certain income and loan requirements, so it is essential to review the specifics with a tax professional or financial advisor. Generally, you can deduct the interest paid on qualified student loans, which includes federal and private loans used for education expenses. For example, if you paid $1,000 in interest on your student loan last year, you may be able to deduct this amount from your taxable income.

Here are some key points to consider when claiming a tax deduction on student loan interest:

- The loan must be used solely for education expenses, such as tuition, fees, and room and board.

- The deduction is subject to income limits, which may reduce or eliminate the deduction for higher-income individuals.

- You can claim the deduction even if you do not itemize your deductions on your tax return.

It is also worth noting that you will need to receive a Form 1098-E from your loan servicer to claim the deduction, which will show the amount of interest paid on your loan during the tax year. By taking advantage of this tax benefit, you can make paying off your student loans more manageable and potentially reduce your tax liability.