As a graduate, managing multiple student loans can be overwhelming, with various interest rates, repayment terms, and due dates to keep track of. For instance, you may have a federal loan with a fixed interest rate and a private loan with a variable interest rate, making it difficult to prioritize your payments. This complexity can lead to missed payments, late fees, and a longer payoff period.

To avoid these pitfalls, it's essential to develop effective strategies for managing your student loans. By taking control of your debt, you can save money on interest, reduce your stress levels, and achieve financial stability sooner. For example, you can start by creating a list of all your loans, including the balance, interest rate, and minimum payment due each month.

Some key considerations when managing multiple student loans include:

- consolidating your loans to simplify your payments

- exploring income-driven repayment plans to lower your monthly payments

- paying more than the minimum payment each month to reduce your principal balance

By understanding these concepts and implementing a solid plan, you can overcome the challenges of managing multiple student loans and achieve your long-term financial goals.

Effective management of your student loans requires a thorough understanding of your financial situation, as well as the various options available to you. By taking the time to educate yourself and create a personalized plan, you can make significant progress in paying off your debt and building a brighter financial future. This may involve working with a financial advisor, using online resources to track your loans, or simply making a few adjustments to your budget each month.

Understanding Your Loans

When it comes to managing your loans, the first step is to identify the types of loans you have. This includes distinguishing between federal and private loans, as each has its own set of interest rates and repayment terms. For instance, federal loans like Stafford and Perkins loans often have fixed interest rates and more flexible repayment options.

To get a clear picture of your loan landscape, gather all your loan documents and create a spreadsheet to track your loans. This spreadsheet should include columns for loan balances, interest rates, and minimum payments. By having all this information in one place, you'll be able to see the full scope of your debt and make more informed decisions about how to tackle it.

Some key details to include in your spreadsheet are:

- Loan type (federal or private)

- Interest rate

- Current balance

- Minimum monthly payment

- Repayment term

Having this information organized will help you prioritize your loans and develop a repayment strategy that works for you.

Income-driven repayment plans can be a useful tool for managing multiple loans, especially if you have a large amount of debt relative to your income. These plans can help lower your monthly payments by capping them at a certain percentage of your income. However, it's essential to understand the pros and cons of these plans, such as potential increases in the total amount paid over the life of the loan due to extended repayment periods.

For example, if you have a mix of federal and private loans with high interest rates, an income-driven repayment plan might be a good option for your federal loans, while you focus on aggressively paying down your private loans. By weighing the benefits and drawbacks of these plans, you can make an informed decision about whether they're right for your financial situation.

Creating a personalized plan for managing your loans takes time and effort, but it's a crucial step in taking control of your finances. By understanding your loans and exploring your repayment options, you'll be well on your way to paying off your debt and achieving financial stability.

Prioritizing Your Loans

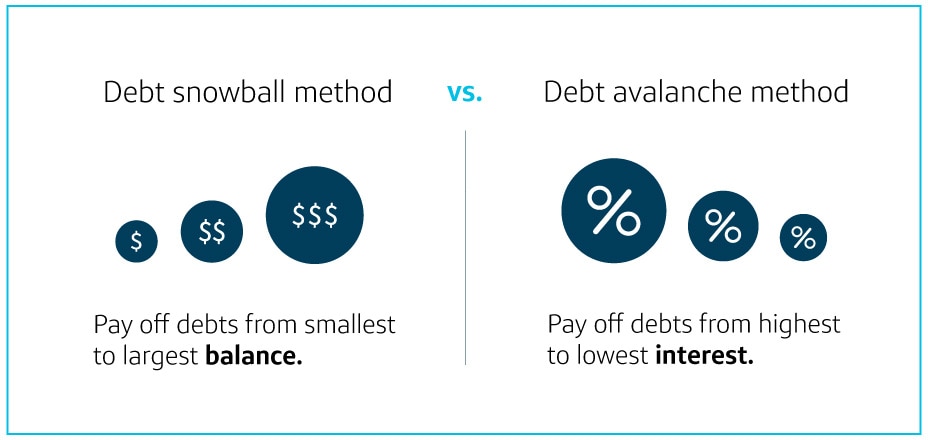

When it comes to managing your debt, prioritizing your loans is a crucial step. To start, determine which loans to prioritize based on interest rates, with high-interest loans typically being paid off first. For instance, if you have a credit card with an 18% interest rate and a student loan with a 6% interest rate, you would focus on paying off the credit card balance first.

Another approach is to consider the snowball method, where you prioritize loans with the smallest balances to build momentum and confidence. This method can be helpful for those who need a psychological boost from quickly paying off smaller loans. By paying off smaller loans, you'll gain a sense of accomplishment and be more motivated to tackle the larger loans.

Some benefits of the snowball method include:

- Quickly eliminating smaller loans to reduce overall debt

- Building momentum and confidence in your debt repayment journey

- Creating a sense of accomplishment as you pay off each loan

This approach may not always be the most cost-effective, but it can be a great way to stay motivated and engaged in the debt repayment process.

Exploring the benefits of consolidating loans can also be a viable option. Consolidating loans can simplify your payments and potentially lower your interest rates. For example, if you have multiple student loans with different interest rates and payment due dates, consolidating them into a single loan with a lower interest rate and one monthly payment can make it easier to manage your debt.

Some things to consider when consolidating loans include:

- Simplified payments and reduced likelihood of missed payments

- Potentially lower interest rates, depending on your credit score and loan terms

- The potential for longer repayment periods, which may increase the total amount paid over time

Ultimately, the key is to find a debt repayment strategy that works for you and your financial situation, and to stay committed to your goals.

Creating a Repayment Plan

When it comes to managing your debt, creating a repayment plan is essential. To start, you need to calculate your total monthly loan payments, including credit cards, student loans, and any other debts you may have. This will give you a clear picture of how much you owe each month and help you determine how much you can realistically afford to pay.

Developing a budget is the next step in creating a repayment plan. This involves allocating a fixed amount for loan payments, taking into account other financial obligations and goals, such as saving for a emergency fund or retirement. By prioritizing your expenses, you can ensure that you have enough money set aside for loan payments and avoid missing payments.

To make your repayment plan more manageable, consider the following tips:

- Track your income and expenses to see where you can cut back on unnecessary spending

- Use the 50/30/20 rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment

- Consider using a budgeting app to help you stay on track and make adjustments as needed

By following these tips and creating a budget that works for you, you can ensure that you have enough money set aside for loan payments and make progress towards becoming debt-free.

Automating your loan payments is another way to ensure timely payments and avoid late fees. You can set up automatic payments through your lender or bank, which will deduct the payment amount from your account on the due date. This way, you can avoid missing payments and make sure that your loans are paid on time, every time. For example, you can set up automatic payments for your student loans, credit cards, or personal loans, and even earn rewards or discounts for making timely payments.

Exploring Forgiveness and Assistance Options

When it comes to managing your student loans, it's essential to explore the various forgiveness and assistance options available. Researching federal loan forgiveness programs, such as Public Service Loan Forgiveness, can be a great place to start. For instance, if you work in a public service role, such as a teacher or nurse, you may qualify for this program, which can forgive a significant portion of your loan balance after a certain number of payments.

Looking into income-driven repayment plans is another way to potentially lower your monthly payments. These plans, such as Income-Based Repayment or Pay As You Earn, can help make your loans more manageable by capping your monthly payments at a certain percentage of your income. This can be especially helpful if you're experiencing financial difficulties or have a variable income.

Some key options to consider when exploring forgiveness and assistance include:

- Public Service Loan Forgiveness, which can forgive loans for borrowers working in public service roles

- Income-Driven Repayment plans, which can lower monthly payments based on income and family size

- Temporary forbearance or deferment, which can provide a temporary reprieve from making loan payments

Reaching out to your loan servicer can also provide valuable guidance on these options and help you determine the best course of action for your specific situation. By discussing your financial situation and loan details with your servicer, you can get a better understanding of the assistance options available to you. Additionally, your servicer may be able to offer additional guidance on how to navigate the forgiveness and repayment process.

Maintaining Financial Health

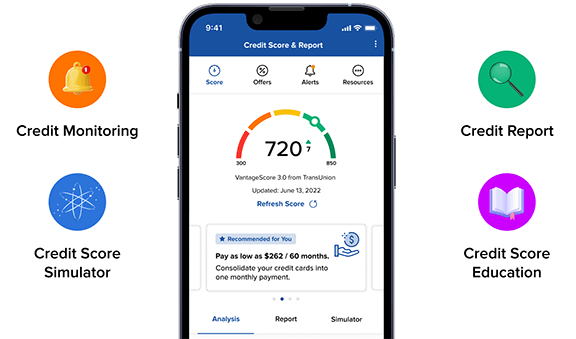

Maintaining financial health is crucial, especially when paying off student loans. To ensure your credit report and score are accurate, it's essential to monitor them regularly. You can request a free credit report from the three major credit bureaus - Equifax, Experian, and TransUnion - once a year, which will help you identify any errors or discrepancies.

One common mistake to avoid is taking on additional debt, such as credit card balances, while paying off your student loans. This can lead to a cycle of debt that's difficult to escape, making it harder to achieve financial stability. For example, if you have a credit card with a high interest rate, try to pay off the balance in full each month or consider consolidating your debt into a lower-interest loan.

Building an emergency fund is also vital to maintaining financial health. This fund will help you cover 3-6 months of living expenses in case of unexpected financial setbacks, such as losing your job or facing unexpected medical bills. Here are some tips to get you started:

- Set aside a fixed amount each month, even if it's just $100

- Avoid dipping into your emergency fund for non-essential expenses

- Consider opening a separate savings account specifically for your emergency fund

By following these tips, you'll be well on your way to maintaining financial health and achieving long-term stability. Remember, paying off student loans is just one aspect of financial health - it's also important to build a safety net and avoid taking on unnecessary debt. With time and discipline, you can achieve financial freedom and start building the life you want.

Frequently Asked Questions (FAQ)

How do I consolidate my student loans?

Consolidating your student loans can be a great way to simplify your finances and make your debt more manageable. Through consolidation, you can combine multiple loans into one loan with a single interest rate and monthly payment. This can be especially helpful if you have multiple loans with different interest rates and payment due dates.

You have two main options for consolidating your student loans: the federal government or a private lender. The federal government offers a Direct Consolidation Loan program, which allows you to consolidate your federal student loans into one loan with a fixed interest rate. For example, if you have multiple federal loans with interest rates ranging from 4% to 7%, you may be able to consolidate them into a single loan with a 5% interest rate.

To consolidate your student loans, you will need to meet certain eligibility requirements, such as having a minimum amount of debt and being current on your loan payments. Here are some steps to consider:

- Check your credit report to ensure it is accurate and up-to-date

- Research and compare consolidation options from different lenders

- Apply for a consolidation loan and provide required documentation, such as proof of income and identification

By following these steps, you can simplify your payments and potentially lower your interest rate, making it easier to manage your student loan debt.

It's also important to consider the potential benefits and drawbacks of consolidating your student loans. For instance, consolidating your loans may lower your monthly payments, but it may also increase the total amount you pay over the life of the loan. On the other hand, consolidating your loans can also help you qualify for income-driven repayment plans or loan forgiveness programs.

What is the difference between deferment and forbearance?

When dealing with financial hardship, it's essential to understand the options available for managing your loans. Deferment is a provision that temporarily suspends loan payments, offering a much-needed break for individuals facing difficulties. This can be particularly helpful for those experiencing unemployment, economic hardship, or other challenging circumstances.

Deferment is typically granted for a specific period, during which time the borrower is not required to make payments. However, it's crucial to note that interest may or may not accrue, depending on the type of loan. For example, subsidized federal student loans usually do not accrue interest during deferment, while unsubsidized loans may continue to accrue interest.

In contrast, forbearance is another option that temporarily reduces or suspends payments, but interest may still accrue, regardless of the loan type. Some common reasons for granting forbearance include illness, financial hardship, or serving in a medical or dental internship. It's essential to carefully review the terms and conditions of your loan to understand how interest accrual works during forbearance.

Here are some key differences between deferment and forbearance:

- Deferment is usually granted for more extended periods, while forbearance is typically shorter-term

- Deferment may not accrue interest, depending on the loan type, while forbearance often accrues interest

- Deferment is often more beneficial for borrowers, as it can provide a more comprehensive break from payments

To illustrate the difference, consider a borrower with a $30,000 unsubsidized student loan, who is granted a 12-month deferment. During this period, no payments are due, and interest may or may not accrue, depending on the loan terms. In contrast, if the borrower is granted a 12-month forbearance, they may not be required to make payments, but interest will likely continue to accrue, adding to the overall loan balance.

It's vital to carefully consider your options and review your loan terms before choosing between deferment and forbearance. By understanding the implications of each, you can make an informed decision that best suits your financial situation and helps you get back on track with your loan payments.

Can I refinance my student loans with a private lender?

Refinancing your student loans with a private lender can be a great way to save money on interest or simplify your monthly payments. This option allows you to replace your existing loans with a new loan that may offer a lower interest rate or more flexible repayment terms. For example, if you have a high-interest rate loan, refinancing with a private lender could help you reduce the amount of interest you pay over the life of the loan.

When considering refinancing with a private lender, it's essential to weigh the potential benefits against the potential drawbacks. One significant consideration is that refinancing federal student loans with a private lender means you will lose access to federal loan benefits, such as income-driven repayment plans and public service loan forgiveness. These benefits can be valuable, so it's crucial to think carefully before making a decision.

Some benefits of refinancing with a private lender include:

- Lower interest rates, which can save you money on interest over the life of the loan

- More flexible repayment terms, such as longer or shorter repayment periods

- Simplification of your monthly payments, as you'll only have one loan to keep track of

On the other hand, refinancing with a private lender may not be the best option for everyone, especially if you rely on federal loan benefits or have a low-income job. It's essential to do your research and consider your individual circumstances before making a decision.

To get started with refinancing your student loans, you'll need to shop around and compare rates from different private lenders. You can typically do this online, and many lenders offer pre-approval or pre-qualification options that allow you to see your potential interest rate without affecting your credit score. Be sure to read the fine print and understand the terms of any loan before signing on the dotted line.