As a young adult, managing student loan debt can be overwhelming, especially with the numerous options available. This article aims to simplify the process by providing a comprehensive guide to the best student loan refinance lenders of 2025. By understanding the various options and their benefits, you can make informed decisions about your financial future.

Refinancing your student loans can help you save money, reduce your monthly payments, and pay off your debt faster. For instance, if you have a high-interest rate loan, refinancing it with a lower interest rate can significantly reduce the amount you pay over the life of the loan. This can be a game-changer for recent graduates who are just starting to build their careers.

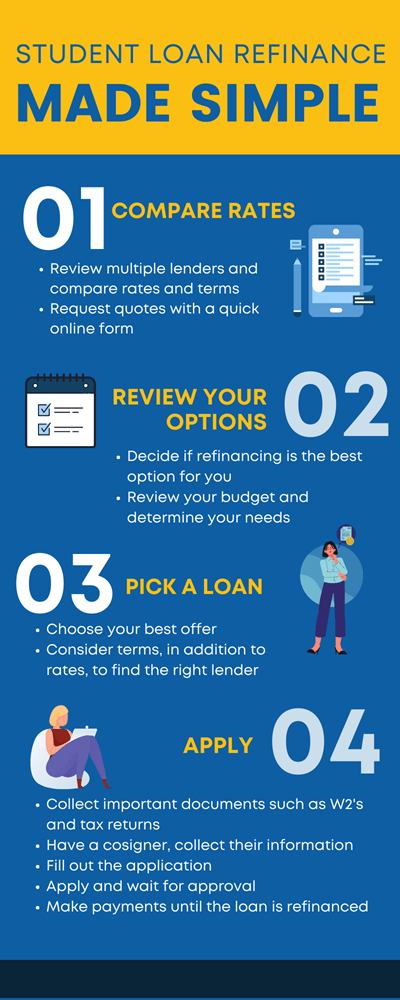

To get started, it's essential to research and compare different lenders to find the one that best suits your needs. Here are some key factors to consider when evaluating student loan refinance lenders:

- Interest rates and fees

- Repayment terms and flexibility

- Customer service and support

- Eligibility requirements and credit score requirements

By considering these factors, you can find a lender that offers the best combination of rates, terms, and benefits for your situation.

Understanding Student Loan Refinance

When it comes to managing student loan debt, one option to consider is refinancing. This process involves replacing your existing loan with a new one, typically with a lower interest rate and more favorable terms. By refinancing, you can potentially save money on interest and simplify your payments.

Refinancing can be a bit complex, especially when it comes to the differences between federal and private student loans. Federal loans, such as those offered through the Department of Education, often have more flexible repayment terms and forgiveness options. Private loans, on the other hand, are offered by banks and other lenders, and their refinance options may vary.

The benefits of refinancing are numerous, including:

- Lower interest rates, which can save you money on interest over the life of the loan

- Simplified payments, as you'll only have to make one payment per month instead of multiple payments to different lenders

- Flexibility, as some refinance lenders offer more flexible repayment terms, such as income-driven repayment plans

For example, if you have a stable income and a good credit score, you may be able to refinance your high-interest private loans to a lower-interest loan with a single lender.

Having a stable income and good credit score can make you a more attractive candidate to lenders, which can lead to better refinance options. If you've recently graduated and landed a well-paying job, or if you've made consistent payments on your loans, you may be able to refinance to a lower interest rate. Additionally, if you have multiple loans with high interest rates, refinancing can help you consolidate them into a single loan with a lower rate.

It's essential to carefully consider your situation and weigh the pros and cons before refinancing. You should also research and compare different refinance lenders to find the best option for your needs. By doing so, you can make an informed decision and potentially save money on your student loans.

Top Student Loan Refinance Lenders of 2025

When it comes to refinancing student loans, choosing the right lender can be overwhelming. To help you make an informed decision, we've compiled a list of top student loan refinance lenders for 2025. These lenders offer competitive interest rates and flexible terms, making it easier to manage your debt.

The top student loan refinance lenders include:

- SoFi, known for its low interest rates and career support services

- CommonBond, which offers a range of repayment terms and forbearance options

- Laurel Road, providing unique benefits like a 0.25% interest rate reduction for automatic payments

Each lender has its own set of eligibility requirements, such as credit score and income thresholds, so it's essential to review these before applying.

Some lenders also offer unique features, such as forbearance options or career coaching, which can be a major advantage for borrowers. For example, SoFi's career support services can help you find a job or transition to a new career, while CommonBond's forbearance options can provide temporary relief if you're struggling to make payments.

To get the best deal, it's crucial to compare interest rates and terms from multiple lenders. You can use online tools to calculate your potential savings and find the lender that best fits your needs. Reading reviews from other borrowers can also give you valuable insights into a lender's customer service and overall experience.

Before choosing a lender, make sure to review the fine print and ask questions about any fees or penalties. You should also consider factors like customer support and online resources, as these can make a big difference in your refinancing experience. By doing your research and comparing lenders, you can find the best refinancing option for your situation and start saving money on your student loans.

It's also important to note that eligibility requirements may vary depending on the lender and the type of loan you're refinancing. Be sure to check the lender's website or contact their customer support team to confirm their requirements and get a clear understanding of the refinancing process.

How to Choose the Best Refinance Option

When considering refinancing, it's essential to evaluate key factors that impact your financial situation. Interest rates, fees, and repayment terms are crucial elements to consider when selecting a refinance lender. For instance, a lower interest rate can save you thousands of dollars over the life of the loan, while excessive fees can negate any potential savings.

To compare and contrast different refinance options, you can use online tools or spreadsheets to organize and analyze the data. Some online tools allow you to input your loan details and receive personalized recommendations, while spreadsheets can help you create a side-by-side comparison of various lenders. This will enable you to make an informed decision based on your individual needs.

Some key factors to consider when evaluating refinance options include:

- Interest rates: fixed or variable, and how they may impact your monthly payments

- Fees: origination fees, closing costs, and any other charges associated with the loan

- Repayment terms: the length of the loan, monthly payment amounts, and any prepayment penalties

By carefully considering these factors, you can choose a refinance option that aligns with your financial goals and helps you achieve long-term stability.

Your individual financial situation and goals should also play a significant role in your decision-making process. For example, if you're looking to pay off your loan quickly, you may prioritize a shorter repayment term, even if it means higher monthly payments. On the other hand, if you're on a tight budget, you may opt for a longer repayment term with lower monthly payments.

Ultimately, choosing the best refinance option requires careful consideration and research. By taking the time to evaluate your options, compare rates and terms, and prioritize your financial goals, you can make an informed decision that sets you up for success. Remember to always review the fine print and ask questions before committing to a refinance lender, and don't hesitate to seek guidance from a financial advisor if needed.

Applying for Student Loan Refinance

When considering student loan refinance, the application process can seem daunting, but it's actually quite straightforward. To get started, you'll typically need to provide personal and financial information, such as your income, employment history, and debt obligations. This information will help lenders assess your creditworthiness and determine the terms of your refinance loan.

The required documents for a student loan refinance application often include identification, pay stubs, and tax returns, as well as information about your existing loans. You may also need to provide documentation of your income and employment, such as a W-2 form or a letter from your employer. Having these documents ready can help speed up the application process and reduce the risk of delays.

As part of the application process, lenders will typically perform a credit check to assess your credit history and score. This can have a temporary impact on your credit score, but it's a necessary step in determining your eligibility for a refinance loan. To improve your chances of approval, consider the following tips:

- Having a co-signer with good credit can help you qualify for a lower interest rate

- Improving your credit score by paying off debt and making on-time payments can also increase your chances of approval

- Shopping around and comparing rates from different lenders can help you find the best deal

After applying for a student loan refinance, the processing time can vary depending on the lender and the complexity of your application. In general, you can expect to wait anywhere from a few days to a few weeks for a decision. Once your application is approved, you can expect to receive a new loan with a lower interest rate and a single monthly payment, which can help simplify your finances and save you money over time.

In terms of potential outcomes, it's possible that your application may be denied if you don't meet the lender's credit or income requirements. However, many lenders offer options for appealing a denial or reapplying with a co-signer. It's also worth noting that some lenders may offer pre-approval or pre-qualification, which can give you an idea of your chances of approval before you submit a full application. By understanding the application process and taking steps to improve your credit and financial profile, you can increase your chances of success and find a refinance loan that works for you.

Managing Refinanced Student Loans

When it comes to managing refinanced student loans, creating a budget is essential. Start by tracking your income and expenses to understand where your money is going, and then allocate a specific amount for your loan payments. This will help you stay on top of your payments and avoid falling behind.

Setting up automatic payments is another crucial step in managing your refinanced student loans. By doing so, you can ensure that your payments are made on time, every time, and you'll also avoid the risk of missing a payment due to forgetfulness. For example, you can set up automatic payments through your bank or loan provider's online portal.

Monitoring your credit reports and scores is also vital when managing refinanced student loans. You can request a free credit report from the three major credit bureaus (Experian, TransUnion, and Equifax) once a year, and review it for any errors or inaccuracies. This will help you stay on top of your credit health and avoid any negative marks on your report.

Some common pitfalls to avoid when managing refinanced student loans include:

- Missing payments, which can negatively impact your credit score

- Not communicating with your loan provider if you're experiencing financial difficulties

- Not taking advantage of tax deductions and other benefits associated with student loan refinance

By being aware of these potential pitfalls, you can take steps to avoid them and successfully manage your refinanced student loans.

Taking advantage of tax deductions and other benefits associated with student loan refinance can also help you save money and reduce your debt burden. For example, you may be eligible to deduct the interest you pay on your refinanced student loans from your taxable income, which can result in significant savings. Be sure to consult with a tax professional or financial advisor to understand the specific benefits and deductions available to you.

In addition to tax deductions, you may also be eligible for other benefits, such as income-driven repayment plans or loan forgiveness programs. These programs can help you manage your loan payments and reduce your debt burden, so it's worth exploring your options and understanding the eligibility criteria. By taking a proactive and informed approach to managing your refinanced student loans, you can achieve financial stability and make progress towards paying off your debt.

Frequently Asked Questions (FAQ)

What are the benefits of refinancing student loans?

Refinancing student loans can be a game-changer for graduates looking to manage their debt more effectively. By refinancing, you can potentially lower your interest rates, which can save you thousands of dollars in interest payments over the life of the loan. For example, if you have a $30,000 loan with an interest rate of 6%, refinancing to a 4% interest rate could save you around $3,000 in interest payments.

One of the main advantages of refinancing student loans is the opportunity to simplify your payments. When you refinance, you can consolidate multiple loans into one loan with a single interest rate and monthly payment. This can make it easier to keep track of your payments and avoid missing deadlines.

Some of the key benefits of refinancing student loans include:

- Lower interest rates, which can lead to significant savings over time

- Simplified payments, which can reduce stress and make it easier to manage your finances

- Improved financial flexibility, which can give you more freedom to pursue other financial goals

Refinancing can also provide improved financial flexibility, allowing you to choose a repayment term that works best for your situation. This can be especially helpful if you're experiencing financial difficulties or if you're trying to pay off your loans quickly. By choosing a shorter repayment term, you can pay off your loans faster and save even more money in interest payments.

Can I refinance both federal and private student loans?

When considering refinancing your student loans, it's crucial to understand the differences between federal and private loans. Federal loans, such as Direct Subsidized and Unsubsidized Loans, can be refinanced, but borrowers should be aware of the potential consequences. This includes the loss of federal benefits, such as income-driven repayment plans and forgiveness options.

Refinancing federal loans means replacing them with a private loan, which may offer a lower interest rate or more favorable repayment terms. However, this also means giving up federal protections, like deferment and forbearance options, which can be beneficial during financial hardship. For instance, if you're experiencing a temporary reduction in income, federal loans may offer more flexible repayment options.

To make an informed decision, consider the following factors:

- Interest rates: Compare the interest rates of your current federal loans with the refinanced private loan offer.

- Repayment terms: Evaluate the repayment period and monthly payments of the refinanced loan.

- Federal benefits: Assess the importance of federal benefits, such as Public Service Loan Forgiveness, to your individual situation.

Private student loans, on the other hand, can also be refinanced, and this may be a more straightforward process since they don't offer the same federal benefits and protections. By refinancing private loans, borrowers may be able to secure a lower interest rate, reduce their monthly payments, or simplify their finances by consolidating multiple loans into one.

It's essential to carefully weigh the pros and cons of refinancing both federal and private student loans, taking into account your individual financial situation and goals. Borrowers should consider their income, expenses, and career plans when deciding whether refinancing is the right choice for them. By doing so, they can make an informed decision that aligns with their financial priorities and objectives.

How do I know if I qualify for student loan refinance?

When considering student loan refinance, it's essential to assess your eligibility. Typically, lenders require a good credit score, stable income, and a history of on-time payments to qualify for refinance options. This is because they want to ensure you can manage your debt obligations and make timely payments.

To determine if you qualify, start by checking your credit score, which can be obtained for free from the three major credit reporting agencies. A good credit score can significantly improve your chances of qualifying for a refinance. For example, a credit score of 700 or higher is often considered good and may help you qualify for better interest rates.

In addition to a good credit score, lenders also look for a stable income, which demonstrates your ability to repay the loan. This can include a steady paycheck, a stable job, or a consistent income from self-employment. Some lenders may also consider other factors, such as:

- Debt-to-income ratio, which should be relatively low

- Employment history, which shows stability and growth

- Loan repayment history, which demonstrates responsible borrowing habits

To improve your chances of qualifying for a refinance, make sure to review your credit report and dispute any errors, make all loan payments on time, and keep your debt-to-income ratio in check. By taking these steps, you can demonstrate to lenders that you're a responsible borrower and increase your chances of qualifying for a refinance. It's also a good idea to shop around and compare rates from different lenders to find the best option for your situation.