As a recent graduate, managing finances can be overwhelming, especially when it seems like everyone is talking about starting a side hustle to build wealth. However, there are alternative strategies that can help you achieve financial stability without taking on a part-time job. By focusing on smart financial decisions, you can set yourself up for long-term success.

One of the most effective ways to build wealth is by making the most of your existing income and expenses. This can involve creating a budget, cutting back on unnecessary expenses, and allocating your money into investments that will grow over time. For example, you can start by tracking your expenses to see where your money is going and identifying areas where you can cut back.

Some key areas to focus on when building wealth without a side hustle include:

- Investing in a retirement account, such as a 401(k) or IRA, to take advantage of compound interest

- Paying off high-interest debt, such as credit card balances, to free up more money in your budget

- Building an emergency fund to cover unexpected expenses and avoid going into debt

By implementing these strategies, you can start building wealth without having to take on a side hustle, and set yourself up for long-term financial success.

It's also important to note that building wealth is a long-term process, and it's not about getting rich quickly. It's about making smart financial decisions and being patient, as your wealth grows over time. By following these strategies and staying committed to your financial goals, you can achieve financial stability and build a secure future for yourself.

Understanding the Wealth Formula

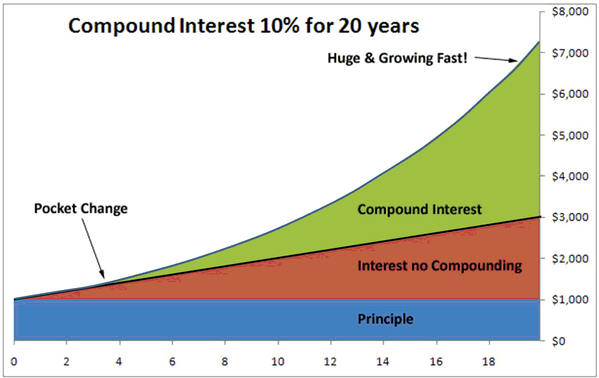

The wealth formula is a simple yet powerful concept that can help individuals create long-term wealth. At its core, it involves understanding the concept of compound interest, which is the idea that your investments can earn interest on both the initial amount and any accrued interest over time. This means that even small, regular investments can add up to significant sums over the years.

Compound interest plays a crucial role in long-term wealth creation, as it allows your money to grow exponentially over time. For example, if you invest $1,000 at an annual interest rate of 5%, you'll earn $50 in interest in the first year, bringing your total to $1,050. In the second year, you'll earn 5% interest on the new total of $1,050, resulting in $52.50 in interest, and so on.

Starting early and being consistent in savings and investments is essential to making the most of compound interest. By beginning to save and invest early, you give your money more time to grow, which can result in significant differences in your long-term wealth. For instance, if you start saving $100 per month at age 25, you'll have more time for your money to compound than if you start saving the same amount at age 35.

Some of the key benefits of starting early and being consistent include:

- More time for your money to compound and grow

- A lower risk of not meeting your long-term financial goals

- A greater sense of financial security and peace of mind

To illustrate the power of small, regular investments, consider the example of a college student who starts investing $50 per month in a retirement account. Over the course of 40 years, this small monthly investment can add up to over $100,000, assuming an average annual return of 7%.

Consistency is also key when it comes to savings and investments. By setting up automatic transfers from your checking account to your savings or investment account, you can make saving and investing a habitual part of your financial routine. This can help you avoid the temptation to spend money impulsively and ensure that you're making progress towards your long-term financial goals.

In terms of practical tips, it's a good idea to take advantage of tax-advantaged accounts such as 401(k) or IRA accounts, which can help your money grow even faster over time. You can also consider working with a financial advisor or using online investment platforms to make investing easier and more accessible. By following these tips and starting early, you can set yourself up for long-term financial success and make the most of the wealth formula.

Setting Financial Foundations

Creating a budget is the first step towards achieving financial stability. To prioritize savings and debt repayment, start by tracking your income and expenses to understand where your money is going. This will help you identify areas where you can cut back and allocate funds more effectively.

Minimizing unnecessary expenses is crucial to making the most of your budget. Consider ways to reduce your daily spending, such as cooking at home instead of eating out or canceling subscription services you don't use. By making a few small changes, you can free up more money in your budget for savings and debt repayment.

To allocate funds effectively, consider using the 50/30/20 rule, where 50% of your income goes towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment. This rule can serve as a guideline to help you prioritize your financial goals. For example, if you earn $4,000 per month, you would allocate $2,000 towards necessary expenses, $1,200 towards discretionary spending, and $800 towards saving and debt repayment.

Here are some tips to help you minimize unnecessary expenses:

- Use the envelope system to categorize and limit your spending

- Avoid impulse purchases by making a shopping list and sticking to it

- Take advantage of sales and discounts on essential items

By following these tips, you can reduce unnecessary expenses and free up more money in your budget for important financial goals.

Having an emergency fund in place is essential for financial stability. This fund will provide a cushion in case of unexpected expenses, such as car repairs or medical bills, and help you avoid going into debt. Aim to save 3-6 months' worth of living expenses in your emergency fund, and keep it separate from your everyday spending money. For example, if your monthly living expenses are $3,000, you would aim to save $9,000 to $18,000 in your emergency fund.

By prioritizing savings and debt repayment, minimizing unnecessary expenses, and building an emergency fund, you can set yourself up for long-term financial success. Remember to review and adjust your budget regularly to ensure you're on track to meet your financial goals. With time and discipline, you can achieve financial stability and secure a brighter financial future.

Investing for the Future

As a beginner, investing for the future can seem overwhelming, but it doesn't have to be. Start by exploring basic investment options such as index funds, which track a specific market index, like the S&P 500, to provide broad diversification. Index funds are often a good starting point due to their low fees and simplicity.

Exchange-traded funds (ETFs) are another popular option, offering flexibility and diversification by allowing you to buy and sell throughout the day. ETFs can track various assets, such as stocks, bonds, or commodities, making them a versatile choice for investors. For example, you can invest in a total stock market ETF to gain exposure to the entire US stock market.

Retirement accounts, like 401(k) or IRA, are also essential investment options, providing tax benefits and a dedicated space to save for your future. These accounts often offer a range of investment choices, from conservative to aggressive, allowing you to tailor your portfolio to your needs. By contributing to a retirement account, you can build a safety net and work towards long-term financial security.

Understanding your risk tolerance is crucial when making investment decisions, as it affects the types of investments you should consider. Your risk tolerance is essentially your ability to withstand market fluctuations and potential losses. To determine your risk tolerance, consider factors such as your age, financial goals, and comfort level with volatility.

Here are some key factors to consider when assessing your risk tolerance:

- Time horizon: When do you need the money, and how long can you keep it invested?

- Financial goals: Are you saving for a specific goal, like a down payment on a house, or long-term retirement?

- Comfort with volatility: Can you stomach market ups and downs, or do you prefer more stable investments?

For further learning on investing and financial literacy, there are many resources available. You can start with online courses, such as those offered by Coursera or edX, which cover topics from basic investing to advanced financial planning. Additionally, websites like Investopedia and The Balance provide a wealth of information on investing, personal finance, and money management, helping you make informed decisions about your financial future.

Maintaining Discipline and Patience

When it comes to saving and investing, it's essential to understand the psychological aspects that can impact our financial decisions. Avoiding get-rich-quick schemes is crucial, as they often promise unrealistic returns and can lead to significant financial losses. For instance, investing in a pyramid scheme may seem lucrative at first, but it can ultimately result in financial ruin.

Developing a long-term mindset is vital for achieving financial success. This involves setting realistic goals and creating a plan to achieve them, rather than seeking quick fixes. By doing so, you can focus on steady progress and avoid the temptation of risky investments.

To stay motivated and committed to your financial goals, it's helpful to break them down into smaller, manageable tasks. This can include creating a budget, automating your savings, and regularly reviewing your investment portfolio. Additionally, consider the following strategies:

- Set specific, achievable goals, such as saving for a down payment on a house or retirement

- Track your progress and celebrate small victories along the way

- Find a financial accountability partner or join a support group to stay motivated

Regularly reviewing and adjusting your financial plan is also crucial for long-term success. This involves assessing your income, expenses, and investments to ensure they align with your goals. By doing so, you can make informed decisions and avoid costly mistakes, such as overspending or underinvesting.

Staying patient and disciplined is key to overcoming financial setbacks and achieving your goals. This involves avoiding impulse purchases and staying focused on your long-term objectives. For example, consider implementing a 30-day waiting period before making non-essential purchases to help you avoid making impulsive decisions.

By adopting a disciplined and patient approach to saving and investing, you can set yourself up for long-term financial success. This involves creating a solid financial foundation, avoiding risky investments, and staying committed to your goals. With time and perseverance, you can achieve financial stability and security, and enjoy the benefits of a well-planned financial future.

Conclusion and Next Steps

As we wrap up our discussion on the wealth formula, it's essential to remember that this approach focuses on silent, long-term growth, rather than get-rich-quick schemes. By investing in a diversified portfolio and consistently saving, you can set yourself up for financial success. For example, starting to save just $100 per month in your early twenties can lead to a substantial nest egg by the time you reach retirement age.

The key elements of the wealth formula include living below your means, investing wisely, and avoiding debt. By following these principles, you can create a solid foundation for building wealth over time. Consider using the 50/30/20 rule as a guideline, where 50% of your income goes towards necessities, 30% towards discretionary spending, and 20% towards saving and debt repayment.

To get started, take a close look at your budget and identify areas where you can cut back on unnecessary expenses. You can then redirect that money towards saving and investing. Some popular options for beginners include:

- Opening a high-yield savings account to earn interest on your savings

- Starting a retirement account, such as a Roth IRA or 401(k)

- Investing in a diversified portfolio of stocks, bonds, or ETFs

For those interested in further learning, there are many resources available to help you on your financial journey. You can check out online courses or workshops that teach investing and personal finance, or read books on the subject, such as "The Total Money Makeover" or "A Random Walk Down Wall Street". Additionally, consider consulting with a financial advisor or joining a community of like-minded individuals to stay motivated and accountable.

Remember, building wealth takes time and discipline, but it's achievable with the right mindset and strategies. By starting small and being consistent, you can make progress towards your financial goals and set yourself up for long-term success. Take the first step today, and watch your wealth grow over time.

Frequently Asked Questions (FAQ)

Do I really need to start saving and investing as early as possible?

When it comes to saving and investing, time is on your side, and the sooner you start, the better. Starting early allows for the power of compound interest to work in your favor over time, helping your money grow exponentially. This means that even small, consistent investments can add up to a significant amount over the years.

The concept of compound interest can be a game-changer for your finances, and it's essential to understand how it works. Essentially, compound interest is the interest earned on both the principal amount and any accrued interest, allowing your savings to grow at an accelerating rate. For example, if you invest $1,000 with a 5% annual interest rate, you'll earn $50 in interest in the first year, and then 5% of $1,050 in the second year, and so on.

To make the most of compound interest, consider the following tips:

- Set up a monthly investment plan, where you invest a fixed amount regularly

- Take advantage of tax-advantaged accounts, such as 401(k) or IRA, to maximize your savings

- Avoid dipping into your investments, and let the power of compound interest work its magic over time

By following these tips and starting to save and invest early, you'll be well on your way to building a secure financial future. Remember, it's not about investing a lot at once, but about being consistent and patient, allowing your money to grow over time.

In practice, this means that even small, regular investments, such as $50 or $100 per month, can add up to a significant amount over the years. For instance, if you invest $100 per month with a 7% annual return, you'll have over $10,000 in 10 years, and over $50,000 in 25 years. This highlights the importance of starting early and being consistent with your investments.

How do I know which investments are right for me?

To determine the right investments for you, it's essential to understand your risk tolerance, which refers to your ability to withstand market fluctuations and potential losses. Consider how you would react if your investments declined in value - would you be able to ride out the downturn or would you need to access your money quickly? This self-reflection will help you make informed decisions about your investment portfolio.

Your financial goals also play a significant role in guiding your investment choices. Are you saving for a short-term goal, such as a down payment on a house, or a long-term goal, like retirement? Different goals require different investment strategies, so it's crucial to identify what you want to achieve. For example, if you're saving for a short-term goal, you may want to consider more conservative investments that prioritize capital preservation.

When evaluating investment options, consider the following factors:

- Return on investment: What kind of returns can you expect from a particular investment, and are they aligned with your financial goals?

- Fees and expenses: What are the costs associated with an investment, and how will they impact your returns?

- Diversification: How will an investment contribute to the overall diversification of your portfolio, and help you manage risk?

By carefully considering these factors and understanding your risk tolerance and financial goals, you can make informed decisions about which investments are right for you.

It's also important to assess your time horizon, or the amount of time you have to invest, as this will impact your investment choices. If you have a longer time horizon, you may be able to take on more risk and invest in assets with higher potential returns, such as stocks. On the other hand, if you have a shorter time horizon, you may want to focus on more conservative investments, such as bonds or money market funds.

Can I still build wealth without a side hustle if I have significant debt?

Having significant debt can feel overwhelming, but it's essential to know that you can still work towards building wealth. Focusing on debt repayment and building an emergency fund are crucial first steps towards financial health and eventual wealth building. By prioritizing these goals, you'll set yourself up for long-term success.

To start, it's vital to understand the importance of debt repayment. This involves creating a budget and debt repayment plan that works for you, and sticking to it. For example, you can use the snowball method, where you pay off debts with the smallest balances first, or the avalanche method, where you focus on debts with the highest interest rates.

Some practical tips for debt repayment include:

- Consolidating debts into a lower-interest loan or credit card

- Cutting back on unnecessary expenses to free up more money for debt repayment

- Using the 50/30/20 rule to allocate your income towards necessities, discretionary spending, and debt repayment

By following these tips, you can make significant progress on your debt and start building momentum towards financial health.

Building an emergency fund is also critical, as it provides a safety net in case of unexpected expenses or job loss. Aim to save 3-6 months' worth of living expenses in a easily accessible savings account. This will help you avoid going further into debt when unexpected expenses arise, and give you peace of mind as you work towards debt repayment.

As you make progress on your debt and emergency fund, you can start to think about longer-term wealth building strategies, such as investing in a retirement account or starting a savings plan for specific goals. Remember, building wealth takes time and patience, but by focusing on debt repayment and building a solid financial foundation, you can set yourself up for success.